In our feature What Is a Hedge Fund? Breaking Down the Basics for Investors, we explained what hedge funds are and how they work. But here’s the catch: not everyone can invest in them.

Unlike mutual funds or ETFs, hedge funds live behind a gate. Their doors are open only to certain investors who meet strict financial qualifications. If you’ve ever wondered why—or whether you might qualify—here’s what you need to know.

Why the Barriers Exist

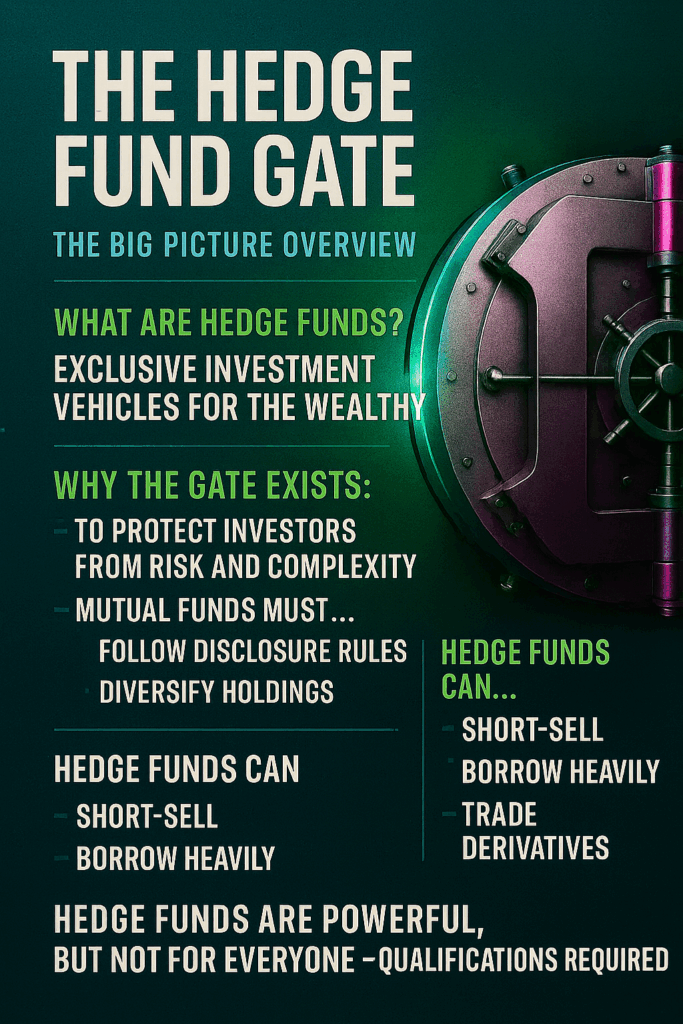

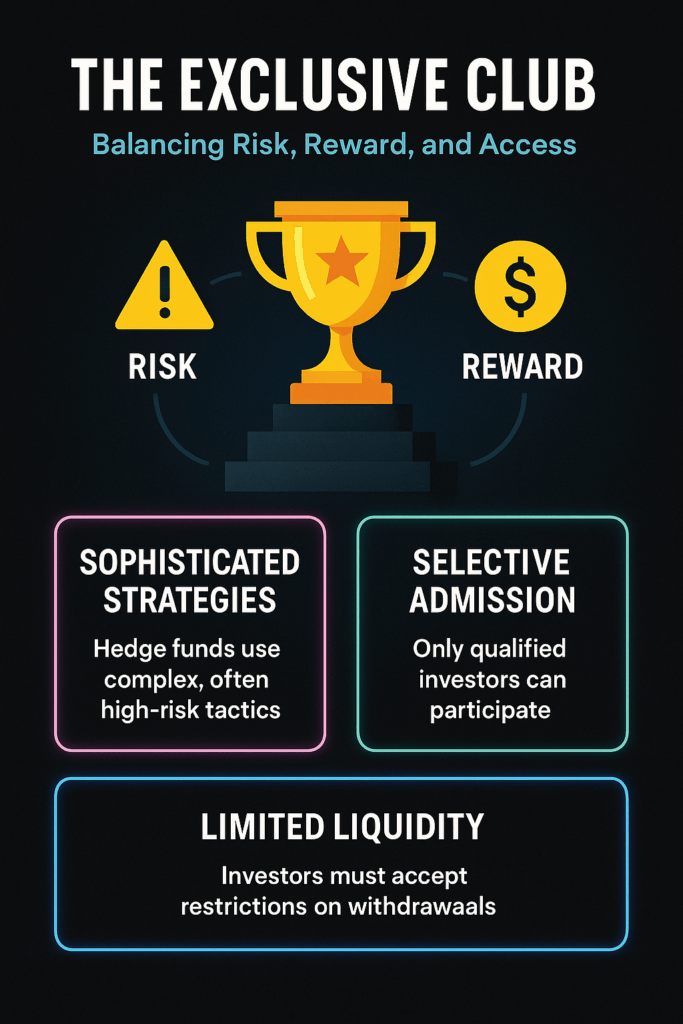

Hedge funds are intentionally exclusive. Regulators like the U.S. Securities and Exchange Commission (SEC) don’t want everyday savers risking retirement money on complex strategies.

Mutual funds must follow disclosure and diversification rules. Hedge funds can short-sell, borrow heavily, and trade derivatives. That freedom raises the risk, and the accredited-investor rules exist to ensure only those with financial cushion—or sophistication—enter the space.

This doesn’t mean hedge funds are “bad” for the public; it just means they’re considered too complex and risky to be offered broadly without limits.

The Accredited Investor Standard

The baseline qualification in the U.S. is being an accredited investor. You qualify by meeting at least one standard:

- Income: $200,000 annually as an individual (or $300,000 with a spouse/partner) for the past two years, with expectations to continue.

- Net Worth: Over $1 million, excluding your primary residence.

- Professional Licenses: Holders of certain credentials (like Series 7, 65, or 82).

- Institutions: Banks, pension funds, and trusts may qualify based on size.

If you don’t meet these, hedge funds can’t legally accept your money.

Qualified Purchasers: A Higher Bar

Some hedge funds require investors to be qualified purchasers. That means at least $5 million in investments for individuals or $25 million for institutions.

Funds with this structure often operate with fewer restrictions, giving managers more latitude in strategy. For investors, it means access to funds that take on riskier or less liquid opportunities—but it also means the wealth bar climbs from “well-off” to “truly wealthy.”

The Institutional Crowd

Most hedge-fund capital actually comes from institutions: pension funds, endowments, and insurance companies. These players value hedge funds for diversification and long horizons.

Institutions can also negotiate better terms—such as reduced fees or greater transparency—because they invest hundreds of millions at a time. When you hear hedge funds manage more than $4 trillion globally, much of that comes from them.

Minimum Investments

Even accredited investors face steep buy-ins. Many hedge funds require minimum investments from $250,000 to several million.

Funds-of-funds sometimes lower the threshold, but still usually start in the six figures. These layered funds offer diversification across multiple hedge funds, though they often come with extra fees.

Lock-Ups and Liquidity

Qualifications aren’t just financial—you need patience too. Hedge funds often impose lock-up periods during which you can’t withdraw money. Even after that, withdrawals may only be quarterly or annually with advance notice.

This structure ensures managers aren’t forced to sell positions prematurely just because investors want out. For you, that means hedge funds require both capital and time.

Why Exclusivity Matters

Exclusivity protects both sides. It shields everyday investors from complex risks and gives managers freedom to pursue long-term or illiquid strategies without worrying about sudden cash demands.

It also adds to the “private club” aura that attracts some wealthy investors. But make no mistake—the rules aren’t about glamour. They’re about reducing risk in a part of the market where strategies can swing quickly.

What If You Don’t Qualify?

Most households won’t qualify, but alternatives exist. Liquid alternatives—mutual funds and ETFs that mimic hedge-fund tactics—are now available to the public.

They don’t match hedge funds’ full flexibility but can provide exposure to strategies like long/short equity or market-neutral investing in a more accessible format. For many, these funds offer a practical middle ground between plain-vanilla mutual funds and the exclusive hedge-fund universe.

The Bottom Line

Hedge funds are not designed for everyone. To invest, you need to meet financial thresholds, commit large sums, and accept limits on liquidity. Institutions dominate, while accredited and qualified investors fill out the rest.

For those who qualify, hedge funds offer diversification and the potential for higher returns—alongside higher risk and cost. For those who don’t, understanding the rules still matters, since hedge funds shape markets that affect us all.

{kind=link}