If you’ve ever wondered whether hedge funds and mutual funds are basically the same thing with different names, you’re not alone. Both pool money from multiple investors, both are managed by professionals, and both aim to grow wealth. But once you start peeling back the layers, the differences are stark.

Hedge funds and mutual funds represent two very different corners of the investment universe—one geared toward accessibility and broad participation, the other toward exclusivity and specialized strategies. Knowing where they diverge can help investors understand not just their options, but also the forces shaping the financial markets they’re part of.

Who Can Invest

One of the biggest differences between hedge funds and mutual funds is who they’re designed for.

- Mutual funds are open to almost anyone. If you have a brokerage account or a retirement plan, you can usually buy into a mutual fund with a modest amount of money—sometimes as little as $1,000 or less. They are heavily regulated by the SEC to protect retail investors, and they must disclose holdings, strategies, and fees regularly.

- Hedge funds, on the other hand, are restricted to “accredited” investors. That means you must meet certain income or net-worth thresholds (currently $200,000 in annual income or $1 million in net worth, excluding your primary home). This barrier is intentional: hedge funds use complex strategies that regulators believe are too risky for the average saver.

In short, mutual funds are democratized investing vehicles. Hedge funds are private clubs.

Regulation and Transparency

Because they are marketed to the public, mutual funds are bound by strict disclosure and reporting rules. Managers must publish prospectuses, file with regulators, and provide ongoing information about their performance and holdings. If you buy into a mutual fund, you can see exactly what securities it owns and how much it costs to run.

Hedge funds, by contrast, operate in a much more opaque environment. They are private investment partnerships, not public funds, so their reporting requirements are limited. Investors often know the broad strategy but not every position or trade. That opacity allows for greater flexibility, but it also makes it harder to know what risks you’re truly exposed to.

Investment Strategies

The range of strategies is another defining difference.

- Mutual funds typically stick to traditional investments like stocks, bonds, or money-market instruments. Their goal is usually to track or beat a benchmark index—think the S&P 500 or the Bloomberg U.S. Aggregate Bond Index. Some funds are actively managed, while others are passive index funds.

- Hedge funds take a far wider approach. They can buy or short stocks, trade currencies and commodities, use derivatives, or invest in distressed debt. Some follow quantitative models, others bet on macroeconomic trends, and some combine multiple strategies under one roof. The common thread is flexibility: hedge fund managers can invest almost anywhere if they believe it will generate returns.

This freedom gives hedge funds a reputation for sophistication and innovation—but also for risk.

Use of Leverage

Leverage is another dividing line.

Mutual funds may use small amounts of borrowing, but they are generally limited by regulation. Their focus is on steady, long-term growth without exposing investors to excessive downside.

Hedge funds, however, frequently use leverage as a core tool. Borrowing amplifies returns, but it also magnifies losses. The collapses of Long-Term Capital Management in 1998 and Archegos Capital in 2021 are stark reminders of how leverage can turn a hedge fund’s downfall into a market-wide event.

For investors, this means hedge funds can deliver spectacular performance in good times but can unravel quickly when bets go wrong.

Liquidity and Access to Cash

Mutual funds are highly liquid. You can buy or sell shares at the fund’s net asset value at the end of each trading day. That liquidity is part of their appeal for everyday investors.

Hedge funds, by contrast, often impose lock-up periods during which you cannot withdraw your money—sometimes a year or more. Even after that, redemptions may only be allowed quarterly or annually, and usually require advance notice. These rules give managers stability to pursue longer-term or less liquid investments, but they reduce flexibility for investors.

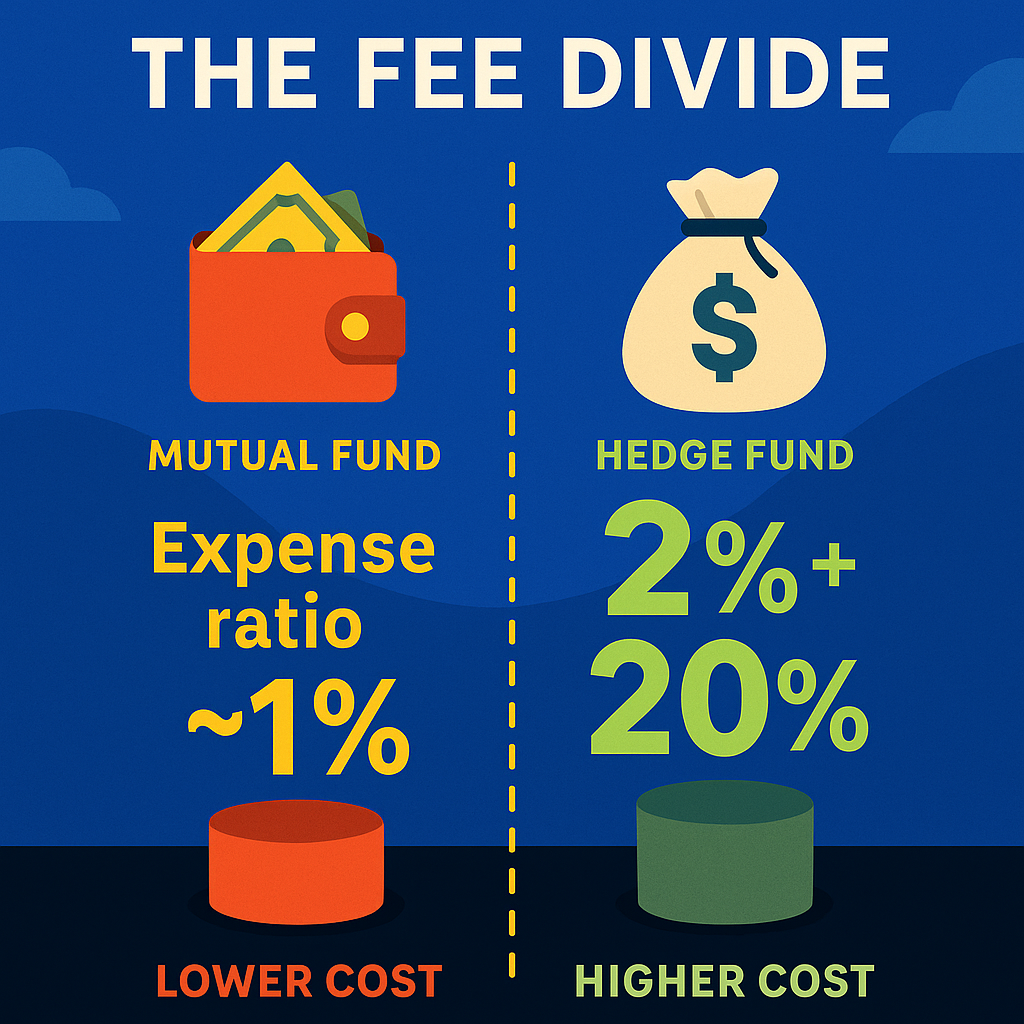

Fees

If you want a clear example of the cultural gap between mutual funds and hedge funds, look no further than fees.

- Mutual funds typically charge an annual expense ratio, often under 1% and increasingly much lower thanks to the rise of low-cost index funds.

- Hedge funds are famous for the “2 and 20” model: a 2% management fee plus 20% of any profits earned.

In practice, competition and investor pressure have pushed many hedge funds to reduce fees, but they still tend to be far more expensive than mutual funds. High costs are one reason critics argue hedge funds often underperform once fees are factored in.

Risk and Reward

Ultimately, the decision to invest in a hedge fund or mutual fund comes down to the balance of risk and reward.

Mutual funds offer accessibility, transparency, and relatively low cost. They’re designed for broad participation and long-term portfolio building. For most investors—especially those saving for retirement—they remain the go-to choice.

Hedge funds, on the other hand, promise the potential for outsized returns and strategies that can perform even in down markets. But they come with high fees, limited liquidity, and substantial risk. They are best suited for institutions or ultra-wealthy individuals who can absorb those trade-offs and want exposure to alternative approaches.

The Bottom Line

Hedge funds and mutual funds may both pool investor capital, but they operate in completely different ecosystems. One is public, transparent, and accessible; the other is private, opaque, and exclusive. One is built for the many; the other, for the few.

Neither is inherently “better.” Instead, each serves a purpose. For most people, mutual funds will remain the practical backbone of investing. For those with the means, appetite for risk, and patience, hedge funds can be a way to diversify into strategies beyond the reach of traditional portfolios.

As always, the right choice depends on your goals, your resources, and your tolerance for risk. But understanding the differences is the first step—and now you have a clear map of the terrain.

{kind=link}