Private credit has become one of the fastest-growing areas in modern finance, yet for many investors it remains opaque and misunderstood. Often referred to as “direct lending” or “private debt,” this asset class sits at the intersection of traditional lending and private markets. For decades, banks dominated corporate lending, but tighter regulations, shifting risk appetites, and investor demand for yield have fueled the rapid rise of private credit funds.

For institutional allocators and wealthy individuals alike, private credit offers compelling opportunities: higher yields than public bonds, diversification from traditional equities, and access to specialized strategies not available through public markets. But these benefits come with risks—illiquidity, manager selection challenges, and exposure to cycles in ways that differ from public markets.

This guide will walk investors through the foundations of private credit. We’ll cover what it is, how it works, its history, strategies, investor requirements, risks, and where the market is heading. By the end, you’ll have a comprehensive framework to evaluate whether private credit belongs in your portfolio.

Defining Private Credit

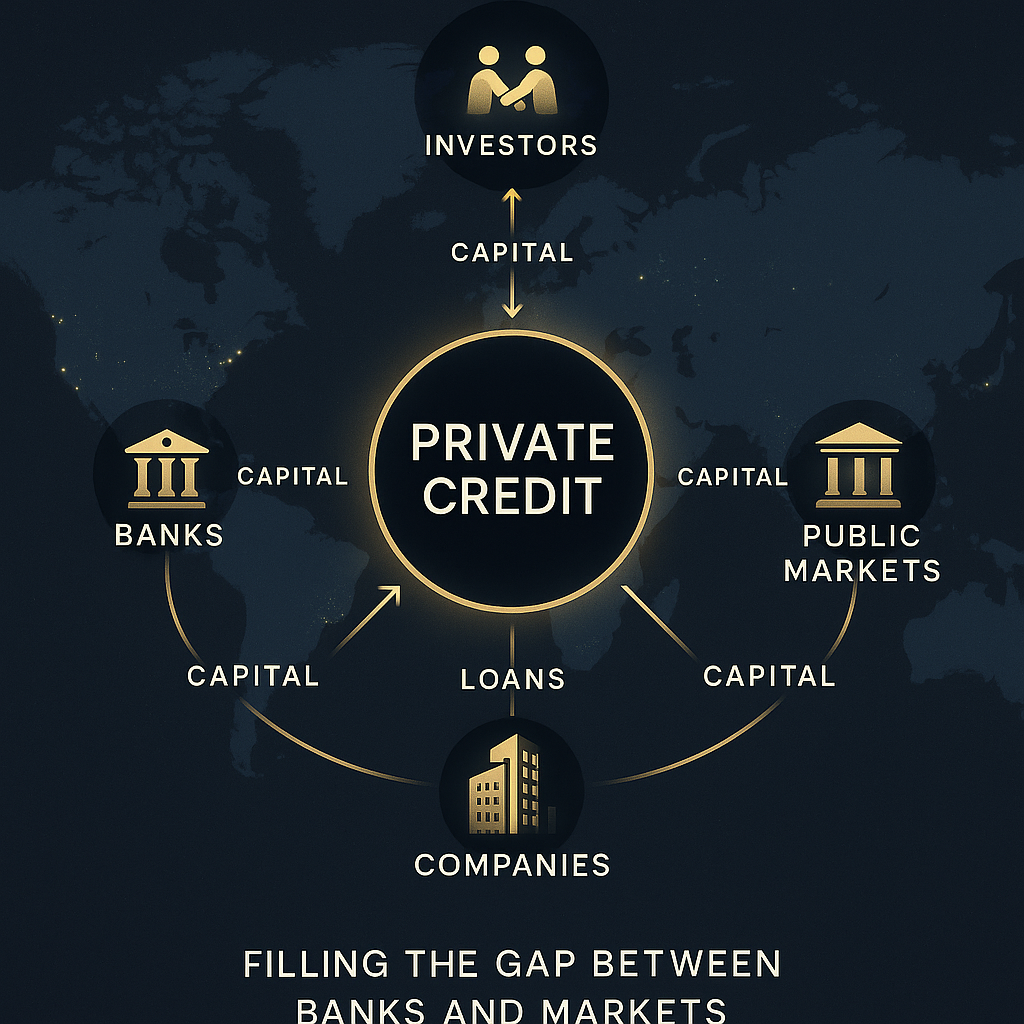

At its simplest, private credit refers to non-bank lending to companies or projects, typically arranged through private funds rather than public bond markets. Unlike traditional bank loans or corporate bonds, private credit deals are not traded on public exchanges. Instead, they are privately negotiated, tailored, and held to maturity.

The hallmark features include:

- Direct lending: Investors provide capital directly to companies, often mid-sized firms that can’t easily access public bond markets.

- Illiquidity: Positions are locked in for years, unlike bonds that trade daily.

- Customization: Terms are negotiated to suit borrower needs and lender protections.

- Higher yield: Investors expect compensation for illiquidity and risk.

Private credit has grown rapidly because it fills a void: businesses need capital, but post-2008 regulations have made banks less able or willing to lend. Investors, meanwhile, crave income and diversification in a world where government bonds have often yielded little.

A Brief History of Private Credit

Private credit isn’t entirely new. In fact, its roots go back centuries to merchant lenders, family financiers, and private banking networks that extended credit long before the modern bond market existed. But the contemporary rise of private credit as an institutional asset class began more recently.

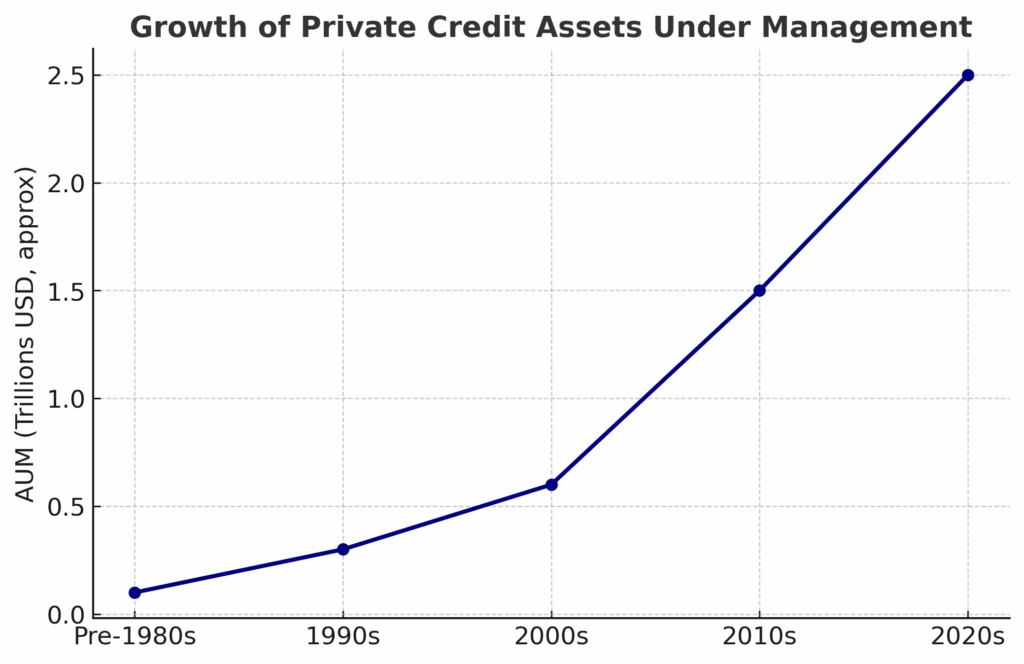

- Pre-1980s: Middle-market lending was almost entirely the domain of banks. Non-bank lending existed but was fragmented and small-scale.

- 1980s–1990s: Junk bonds, pioneered by firms like Drexel Burnham Lambert, opened new channels for financing riskier companies. Still, most loans flowed through banks.

- 2000s: Private credit began to emerge as institutional investors, especially in the U.S., sought higher-yield alternatives to bonds. Hedge funds and PE firms experimented with lending strategies.

- 2008 Financial Crisis: This was the turning point. Regulations such as Basel III and Dodd-Frank forced banks to hold more capital and de-risk their balance sheets. Lending to small and mid-sized companies became less attractive for banks. Private credit funds stepped in to fill the gap.

- 2010s–Present: Assets under management (AUM) in private credit exploded, surpassing $1.5 trillion globally by the early 2020s, with projections to exceed $2.5 trillion in coming years. Institutional investors such as pension funds, insurance companies, and sovereign wealth funds have become core allocators.

Today, private credit is a mainstream alternative asset class, sitting alongside private equity, real estate, and infrastructure in sophisticated portfolios.

How Private Credit Works

The mechanics of private credit revolve around fund structures and deal execution. Here’s a step-by-step look:

- Fundraising: Private credit managers—often specialist firms or private equity affiliates—raise capital from investors. Commitments are usually locked for 7–10 years.

- Sourcing Deals: Managers identify lending opportunities through networks, investment banks, and relationships with private equity sponsors.

- Due Diligence: They evaluate the borrower’s financials, collateral, management team, and industry dynamics.

- Structuring Loans: Deals can range from senior secured loans to subordinated mezzanine debt, often customized for borrower and investor needs.

- Ongoing Monitoring: Fund managers monitor performance, enforce covenants, and may restructure terms if challenges arise.

- Exits: Since most loans are not tradable, the exit comes when the borrower refinances, is acquired, or pays down the debt.

Types of Private Credit Strategies

Not all private credit is the same. Strategies vary by borrower size, risk tolerance, and structure:

- Direct Lending: The largest category, providing loans (often senior secured) to mid-market companies. Typically used for buyouts, expansions, or refinancing.

- Mezzanine Debt: Subordinated debt that sits below senior loans but above equity. Higher yield, often with equity “kickers” such as warrants.

- Distressed Debt: Investing in troubled companies, aiming to restructure or take control. High risk, high reward.

- Special Situations: Flexible capital for unique cases—turnarounds, rescue financing, or litigation-backed lending.

- Asset-Backed Lending (ABL): Loans secured by receivables, equipment, or real estate. Often safer due to collateral.

- Venture Debt: Loans to venture-backed startups, providing capital between equity rounds. Usually paired with equity warrants.

- Infrastructure Debt: Financing energy, transportation, or digital infrastructure projects with stable, long-term cash flows.

Each strategy offers a different balance of yield, risk, and correlation to broader markets.

Why Companies Borrow from Private Credit

If traditional bank loans are cheaper, why do companies borrow from private funds? The answer lies in flexibility and access.

- Speed: Private credit deals can be arranged faster than bank loans.

- Customization: Terms can be tailored, with fewer rigid requirements.

- Availability: Mid-sized or leveraged companies may not qualify for bank lending.

- Partnership: Private lenders often work closely with private equity sponsors to fund acquisitions or growth.

For borrowers, paying a premium in interest may be worth it if it secures needed capital without the restrictions of traditional lenders.

Private Credit vs. Bonds

It’s easy to confuse private credit with high-yield bonds. Both involve lending to companies outside the investment-grade universe. The differences are important:

- Liquidity: Bonds trade publicly; private credit loans do not.

- Customization: Bonds are standardized; private credit is bespoke.

- Investors: Bonds are broadly available; private credit requires accredited or institutional investors.

- Yields: Private credit typically offers higher yields to compensate for illiquidity and complexity.

Investor Requirements

Private credit is not open to everyone. Investors generally must be:

- Accredited Investors (income > $200,000 or net worth > $1M, excluding primary residence).

- Qualified Purchasers (>$5M in investable assets).

- Institutions such as pension funds, insurance companies, family offices, and endowments.

Minimum commitments often range from $5–10 million for large funds, though some feeder funds and interval funds now lower the threshold.

Returns in Private Credit

One of the main attractions of private credit is yield. Historically, annual returns for direct lending funds have ranged between 8–12% net of fees, significantly higher than public corporate bonds.

- Senior loans: Lower yield, lower risk (6–9%).

- Mezzanine debt: Higher yield, higher risk (10–15%).

- Distressed/special situations: Can exceed 15–20%, but with volatility.

Importantly, returns are less tied to public equity markets, making them valuable diversifiers in multi-asset portfolios.

Risks in Private Credit

Higher yields don’t come free. Key risks include:

- Illiquidity: Capital is locked for years, limiting flexibility.

- Credit Risk: Borrowers may default, especially in downturns.

- Manager Risk: Outcomes depend heavily on the manager’s skill in sourcing, structuring, and monitoring.

- Cyclical Exposure: A recession can trigger widespread defaults, especially in cyclical industries.

- Regulatory/Legal Risks: Bankruptcy laws, lender protections, and jurisdictional rules vary.

How Private Credit Creates Value for Investors

Private credit managers add value in multiple ways:

- Risk Selection: Identifying borrowers with strong cash flows and growth prospects.

- Structuring: Using covenants, collateral, and tailored terms to protect downside.

- Active Monitoring: Engaging with borrowers to avoid defaults.

- Specialization: Leveraging industry expertise (e.g., healthcare lending, energy project finance).

Global Growth of Private Credit

The U.S. has been the epicenter of private credit, but growth is now global.

- Europe: Post-2008 bank retrenchment created a massive opportunity. Direct lending funds are now entrenched in mid-market financing.

- Asia: Still developing but growing fast, especially in private lending to family-owned conglomerates and real estate.

- Emerging Markets: Higher yields available, but with political and legal risks.

Global investors often use private credit to diversify geographically while accessing attractive spreads.

Private Credit vs. Private Equity

Private credit and private equity often overlap but differ in key ways:

- Equity vs. Debt: PE owns companies; private credit lends to them.

- Risk/Return: PE has higher upside and downside; private credit is more income-oriented.

- Time Horizon: PE exits through IPOs or sales; private credit exits when loans are repaid.

- Correlation: Both can suffer in downturns, but credit often provides steadier cash flows.

Many large managers now run both PE and private credit arms, giving investors bundled options.

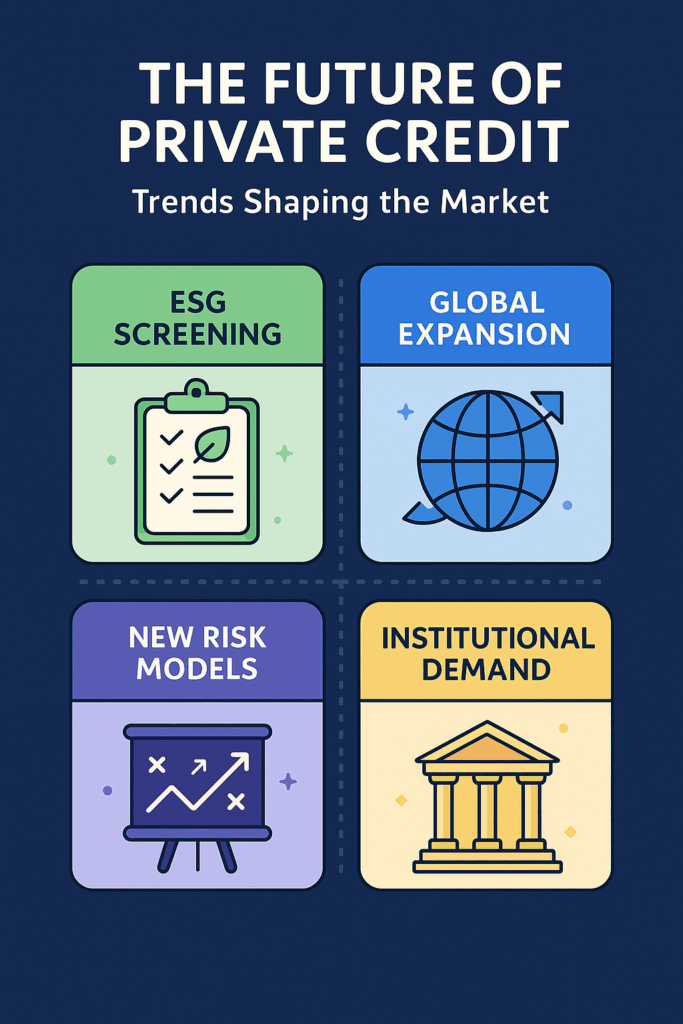

Emerging Trends in Private Credit

The private credit market is evolving rapidly. Key trends include:

- ESG Integration: More funds now screen loans for environmental, social, and governance (ESG) factors.

- Tokenization: Blockchain platforms are experimenting with tokenized loan participation, potentially improving liquidity.

- Retail Access: Interval funds and semi-liquid vehicles aim to bring private credit to affluent retail investors.

- Competition: As more capital flows in, yields may compress, requiring managers to differentiate through specialization.

Case Study: A Mid-Market Direct Loan

Imagine a private equity sponsor buying a regional healthcare provider. The acquisition requires $200 million in financing. A bank offers $100 million, but won’t provide the rest due to leverage limits.

A private credit fund steps in with $80 million in senior secured loans and $20 million in mezzanine debt. The deal closes quickly, tailored to the sponsor’s timeline. The fund earns 10% annually on the senior loan and 14% on the mezzanine tranche. Upon exit, investors receive steady income and potentially equity upside if warrants are exercised.

Private Credit in a Diversified Portfolio

For institutional allocators, private credit is increasingly viewed as a core allocation within alternatives. Typical allocations range from 5–15% of a portfolio. Benefits include:

- Income: Stable cash yield.

- Diversification: Low correlation to equities and bonds.

- Inflation Hedge: Many loans are floating-rate, protecting against rising interest rates.

The trade-off is illiquidity and the need for careful manager selection.

The Future of Private Credit

Looking forward, private credit is likely to continue expanding as a mainstream asset class. Key drivers:

- Bank Retreat: Regulations will keep banks cautious, leaving room for private lenders.

- Institutional Demand: Pension funds and insurers need yield in a low-rate world.

- Innovation: Tokenization, data-driven risk models, and ESG integration will reshape practices.

- Globalization: Growth in Asia and emerging markets will diversify opportunities.

The Bottom Line

Private credit is no longer a niche—it is a pillar of modern alternative investing. For investors, it represents a chance to capture yield, diversify portfolios, and access opportunities that were once confined to banks. But it also demands patience, due diligence, and tolerance for illiquidity.

As this guide has shown, private credit spans strategies from direct lending to distressed debt, across geographies and industries. It requires understanding structures, risks, and the manager’s skill. For sophisticated investors with a long horizon, it can play a powerful role in building durable, income-oriented portfolios.

{kind=link}