This Content Is Only For Subscribers

When you lend money in private credit, you’re not just betting on a borrower’s promise—you’re securing a claim on something tangible if things go wrong. That “something” is collateral, and it’s the backbone of downside protection. For new investors, here’s a clear, no-jargon tour of what collateral is, how it’s valued and monitored, and the practical questions that separate strong structures from wishful thinking.

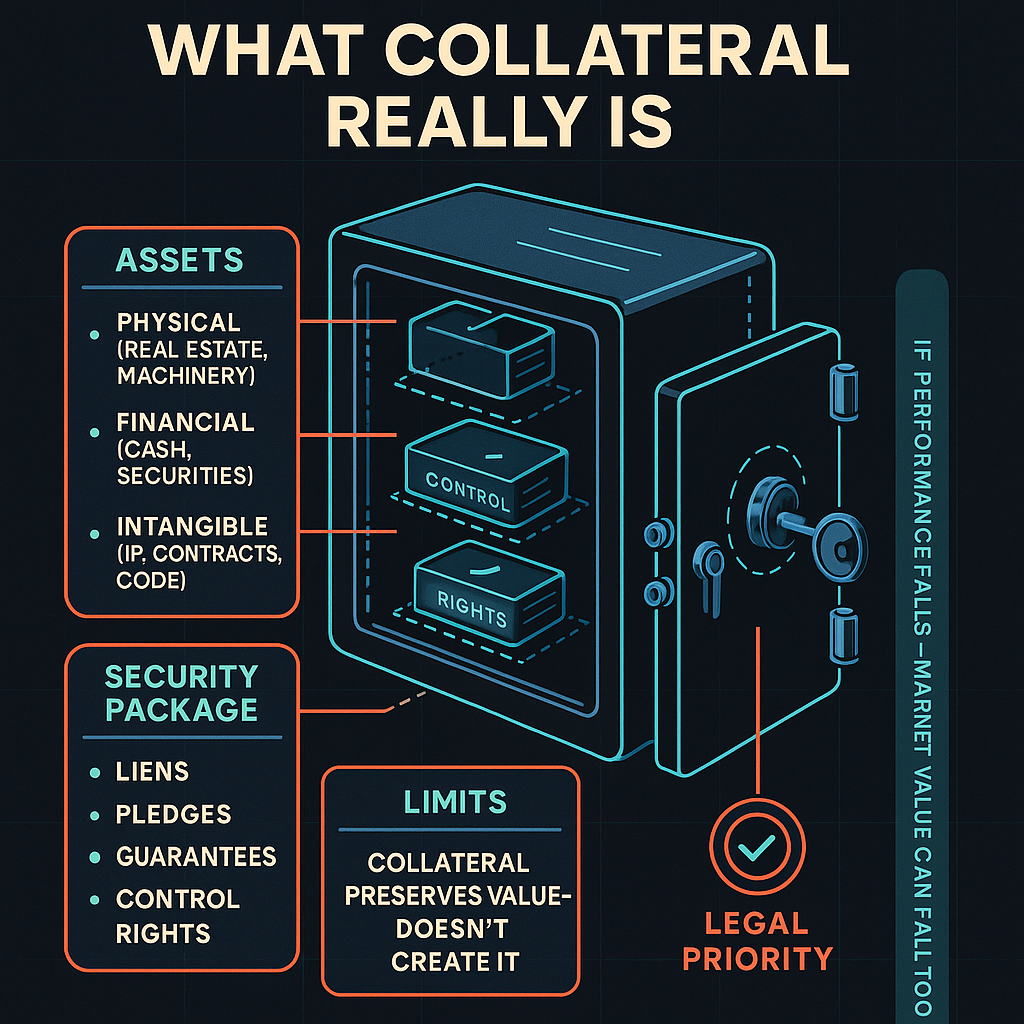

What collateral really is (and isn’t)

Collateral is an asset—or a pool of assets—that the lender can take or control if the borrower defaults. It can be physical (real estate, machinery), financial (cash, securities), or intangible (intellectual property, contracts, software code). In private credit, collateral lives inside a security package: liens, pledges, guarantees, and rights spelled out in the loan agreement.

Important nuance: collateral doesn’t create value; it preserves it. If business performance collapses, the collateral’s market value may fall too. The lender’s advantage is legal priority and a plan to convert assets into repayment faster than other creditors can.

Seniority and lien priority: who gets paid first?

Think of the capital structure as a line at the exit door during a fire drill:

- First-lien secured lenders are first in line, with a direct claim on pledged assets.

- Second-lien lenders stand behind first-lien lenders on the same collateral.

- Mezzanine/subordinated lenders may be secured by different assets, or unsecured but compensated with higher coupons or equity kickers.

The intercreditor agreement is the rulebook that decides who can act, when, and how sale proceeds are split. In a stress, these rules matter more than any marketing slide.

Investor takeaway: Ask which lien you hold, what assets it covers, and for a plain-English summary of the intercreditor terms.

Two big flavors: cash-flow lending vs. asset-based lending (ABL)

Cash-flow lending relies on the borrower’s earnings capacity (EBITDA) and overall enterprise value. Collateral here is often a broad “all-asset” lien: accounts, inventory, equipment, IP, and stock pledges. Protection comes from financial covenants (e.g., leverage, interest coverage), frequent reporting, and the ability to push for changes early if coverage weakens.

Asset-based lending (ABL) relies on assets that are regularly valued and liquid. Lenders set a borrowing base—a formula that advances, say, 85% of eligible receivables or 60% of eligible inventory—with eligibility rules (aging, concentration, dilution) and field exams to verify what’s really there. When assets convert to cash, the loan balance adjusts too.

Investor takeaway: ABL can produce lower losses because collateral is measured and tested constantly. Cash-flow deals can offer higher yields but depend more on covenants and sponsor support.

How lenders value collateral (and protect that value)

1) Advance rates and haircuts.

A lender rarely advances 100% against collateral. The advance rate leaves a cushion for price moves, selling costs, and errors. More volatile assets (fashion inventory) get lower advance rates than stable ones (prime receivables).

2) Perfection and control.

Lawyers “perfect” security interests (filings, control agreements, mortgages) so the lender’s claim is legally enforceable and senior to others. For cash and securities, account-control agreements can give the lender practical control if triggers are hit.

3) Appraisals and field exams.

For property and equipment, appraisals anchor value. For ABL, cycle counts, aging schedules, and site visits keep numbers honest. Expect periodic re-valuations—especially in fast-moving industries.

4) Covenants and reporting.

Maintenance tests (borrowing-base compliance, minimum liquidity) and reporting cadences (monthly or even weekly in ABL) provide early warning. When a company drifts, a lender can tighten terms, charge amendment fees, or ask for more collateral.

What strong collateral packages include

- Clear collateral description. Exactly what’s pledged (and what’s excluded).

- Priority on key assets. First claim on the things that matter: cash, receivables, IP, equipment, real estate.

- Guarantors where it counts. Parent or subsidiary guarantees that actually add value, not just paper comfort.

- Control over cash. Springing or full control of key bank accounts if covenants trip.

- Thoughtful covenants. Limits on additional debt, liens, asset sales, and dividends; information and inspection rights.

- Insurance and loss payee status. If something burns down, the lender is first in line for proceeds.

- Well-drafted intercreditor terms. Timelines and voting thresholds that allow action in a crisis.

Red flags to watch for

- Collateral you can’t sell fast. Obscure assets with thin markets and high legal friction.

- Over-broad carve-outs. “All-asset liens” that quietly exclude the crown jewels.

- Weak perfection. Missing filings, no account control, or liens that don’t attach in key jurisdictions.

- Covenant-lite creep. No maintenance tests, limited reporting—problems surface too late.

- Leaky baskets. Generous capacity for additional debt, liens, or asset transfers that dilute your claim.

- Wishful appraisals. Aggressive assumptions, stale reports, or no back-testing vs. sale values.

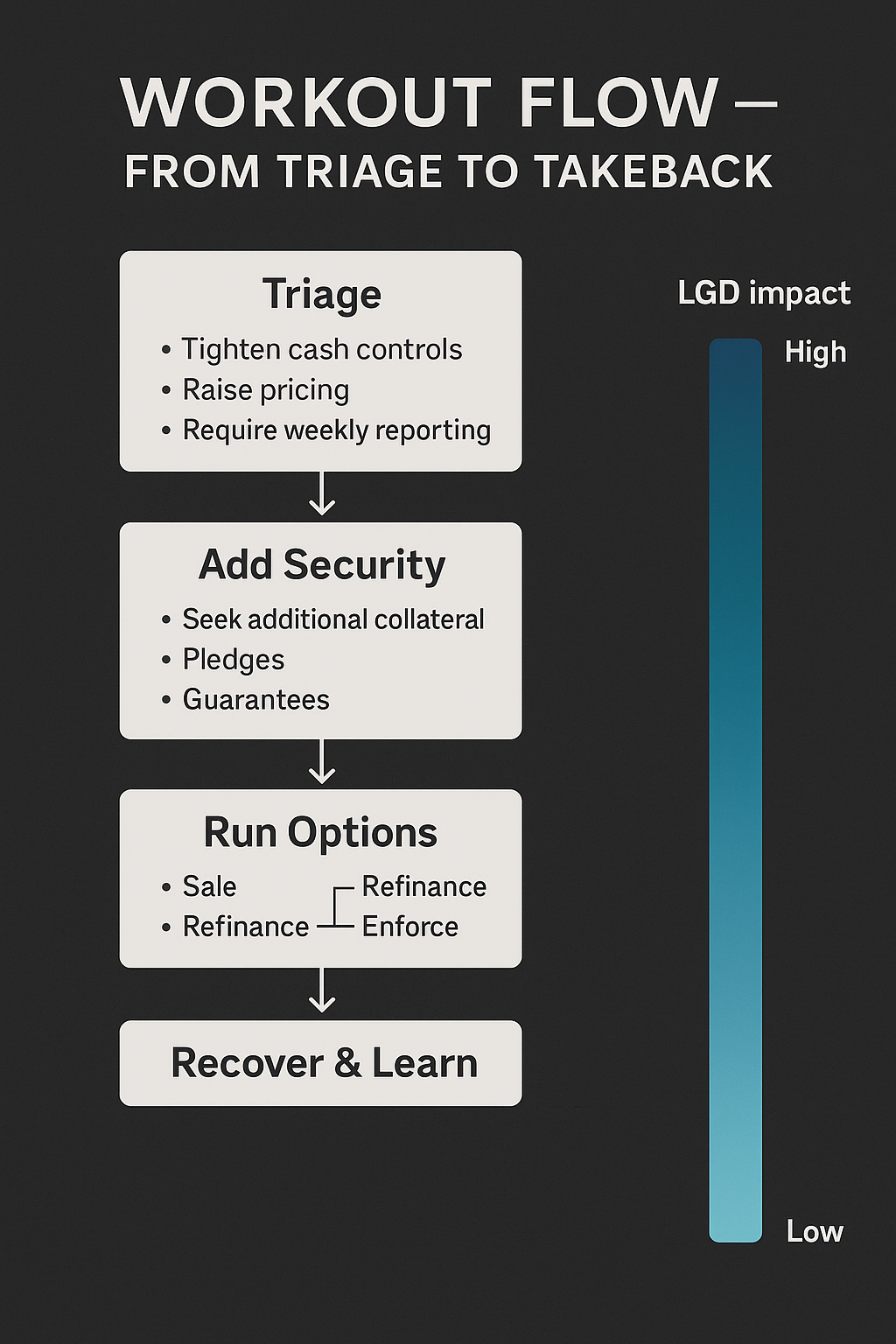

How collateral works in a workout

When performance slips, good lenders act early:

- Triage. Tighten cash controls, raise pricing, require weekly reporting.

- Add security. Seek additional collateral, pledges, or guarantees.

- Restructure terms. Extend maturities for a fee and a paydown; add covenants that bite.

- Run options. Prepare for a sale, refinance, or, if needed, enforce on collateral.

- Recover and learn. Compare realized proceeds to underwritten collateral values and update the playbook.

Well-documented collateral plus decisive action often reduces loss severity, even when default risk rises.

Diligence questions to copy/paste

- What assets secure the loan, exactly, and where are they?

- How are liens perfected and ranked across jurisdictions?

- What are the borrowing-base rules (advance rates, eligibility, reserves)?

- Who controls cash, and when do springing controls activate?

- What’s the appraisal/field-exam cadence, and who pays?

- Which covenants give early warning (and how often are they tested)?

- Show me the intercreditor summary: who can enforce, and on what timeline?

- Track record: realized recoveries vs. underwritten collateral values on past problem loans.

Bottom line

Collateral is the seatbelt of private credit. It won’t prevent a crash, but it can dramatically reduce the damage when things go wrong. The best protection isn’t just “being secured”—it’s being secured well: clear liens, enforceable priority, tested values, tight cash control, and covenants that surface trouble early. If a manager can explain these mechanics in plain English—and back them with real recoveries—you’re much closer to owning the downside, not just the pitch.