Private equity (PE) is a powerful investment vehicle, but understanding how PE funds are structured is critical for any investor considering participation. While the concept of private equity often evokes images of large buyouts, venture investments, and operational turnarounds—as explored in What Is Private Equity? Understanding the Foundations of PE Investing—the mechanics of the funds themselves are equally important. Knowing how limited partners (LPs), general partners (GPs), and carried interest interact can help investors evaluate opportunities, assess risk, and understand potential returns.

Understanding the Fund Structure

Private equity funds typically follow a limited partnership model, the most common legal structure for pooled investments. In this setup, the fund has two main types of participants:

- General Partners (GPs): The GP is the private equity firm itself, responsible for sourcing deals, managing investments, implementing value creation strategies, and ultimately exiting investments. GPs make the day-to-day decisions regarding portfolio companies and oversee all operational, financial, and strategic activities. They also typically contribute a small percentage of the fund’s capital—often 1–5%—to align interests with investors.

- Limited Partners (LPs): LPs are the investors who provide the bulk of the capital. These can include institutional investors such as pension funds, endowments, insurance companies, sovereign wealth funds, and high-net-worth individuals. LPs enjoy limited liability, meaning they are not responsible for the fund’s debts beyond their committed capital, and they do not participate in day-to-day management.

This partnership structure is essential because it clearly separates management responsibilities and risk while aligning incentives between the fund managers and the investors.

Capital Commitment and Drawdowns

Investors don’t transfer the full amount of their commitment to the fund upfront. Instead, PE funds operate on a capital call or drawdown system. The GP will “call” portions of the committed capital over time as investment opportunities arise. This approach allows LPs to manage liquidity efficiently, keeping capital invested elsewhere until needed.

For example, if an investor commits $1 million to a fund, the GP may draw $200,000 initially to acquire a company. Subsequent calls would occur as additional acquisitions or operational improvements require capital. This phased approach is standard in PE investing and reflects the long-term, illiquid nature of the asset class.

Management Fees

Private equity funds charge management fees to cover operational costs, including salaries, research, due diligence, and administrative expenses. These fees typically range from 1.5% to 2% annually of committed or invested capital.

While fees are lower than hedge fund structures in some cases, they can add up over a 10-year fund life. Management fees provide a predictable revenue stream for the GP, regardless of fund performance, but they are distinct from profit-sharing arrangements.

Carried Interest: Aligning Incentives

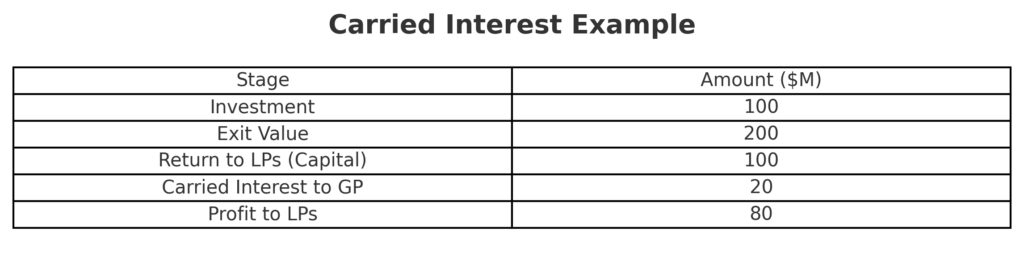

Carried interest is arguably the most distinctive feature of private equity fund economics. It represents the GP’s performance-based share of profits, typically 20% of the fund’s gains after returning the original capital to LPs.

For example, if a PE fund invests $100 million in a portfolio of companies and ultimately exits for $200 million, the LPs would first receive their $100 million back. The GP then earns 20% of the $100 million profit, or $20 million, as carried interest. This model incentivizes GPs to maximize returns because their compensation is directly tied to fund performance.

Some funds use hurdle rates, a minimum return threshold LPs must receive before the GP can collect carried interest. This ensures that LPs achieve a baseline return before the GP participates in profits, further aligning incentives.

Fund Lifecycle

The structure of a PE fund is also reflected in its lifecycle:

- Fundraising Period: Typically 12–24 months, during which the GP secures commitments from LPs.

- Investment Period: Usually 3–5 years, when the GP identifies and acquires portfolio companies.

- Holding Period: Around 4–7 years, during which the GP actively manages and grows companies.

- Exit Period: The final stage, when portfolio companies are sold, and returns are distributed to LPs according to the partnership agreement.

The overall fund life often spans 10–12 years, providing enough time to source, develop, and exit investments while distributing returns systematically.

Understanding Risk and Return Distribution

The LP-GP structure balances risk and reward. LPs are exposed to market, operational, and liquidity risk but benefit from limited liability and professional management. GPs take on operational responsibility and reputational risk but stand to earn substantial profits through carried interest.

Returns are generally private equity-specific metrics rather than daily market movements. The internal rate of return (IRR) and multiple on invested capital (MOIC) are the primary measures. Because of the long-term, illiquid nature of investments, investors should understand that distributions may not occur until years after the initial commitment.

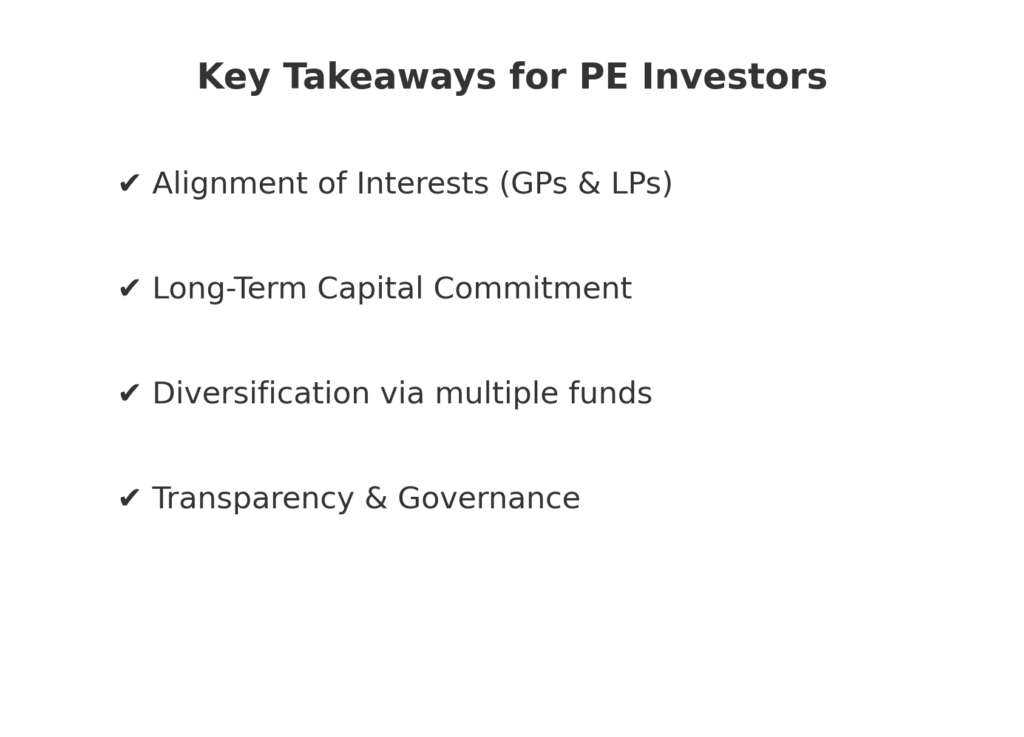

Key Takeaways for Investors

- Alignment of Interests: The combination of management fees and carried interest ensures that GPs are motivated to maximize value for LPs.

- Long-Term Commitment: Investors must be prepared for capital to be locked for the fund’s life.

- Diversification: Investing in multiple funds or funds-of-funds can reduce exposure to a single GP, sector, or geography.

- Transparency and Governance: LPs rely on quarterly reporting, advisory boards, and fund agreements to monitor performance and maintain accountability.

Understanding the structure of private equity funds is essential for evaluating opportunities, assessing risk, and optimizing portfolio allocation. LPs and GPs work together under a carefully designed framework that balances active management, investor protection, and financial incentives.

For investors seeking exposure to private companies, grasping how funds operate—from commitments and drawdowns to carried interest and exits—is just as important as understanding the underlying investments themselves. By mastering the mechanics of fund structure, investors can make informed decisions and maximize the potential benefits of private equity as a long-term, strategic component of their portfolios.

{kind=link}