This Content Is Only For Subscribers

Venture capital (VC) can look mysterious from the outside: early bets on unproven teams, big swings at new markets, and a lot of alphabet soup (SAFE, QSBS, 83(b), 3(c)(1), 506(c)…). Underneath, though, VC runs on a fairly well-defined regulatory framework. If you’re a newer investor—maybe considering a fund commitment, an angel check, or a role at a startup—this guide walks the terrain in plain English: who the referees are, what rules shape behavior, where the tripwires live, and how to read documents with more confidence.

The one-minute map: who regulates what

- Securities laws govern how money is raised and who can invest. In the U.S., the Securities and Exchange Commission (SEC) sets the baseline; states add notice filings and certain local rules.

- Investment-adviser rules regulate the VC manager (the firm making the investments)—its fiduciary duties, marketing, recordkeeping, and conflicts controls.

- Company law and tax rules shape the startup side (cap tables, options, investor rights, Qualified Small Business Stock) and the fund side (partnership taxation, carried interest).

- Global regimes (EU/UK alternative-fund rules; Asia hubs; local foreign-investment screening) matter when capital or companies cross borders.

- Other overlays—privacy, data transfers, sanctions/export controls, labor, and antitrust—surface in diligence or exits.

Keep that scaffold in mind, and the acronyms start to make sense.

How VC funds are set up (and why it matters to investors)

Most VC funds are limited partnerships (LPs). Investors (limited partners, or LPs) commit capital to a general partner (GP) managed by an investment adviser (the management company). The fund draws capital over time, invests in startups, and returns cash (or stock) after exits. A separate parallel fund or feeder may exist for certain investor types or jurisdictions.

Two important consequences:

- Pass-through taxation. Funds are typically taxed as partnerships. Income, losses, and gains “pass through” to investors, who report them on a Schedule K-1. That means you can be taxed on allocations even before cash arrives (“phantom income”), and basis tracking matters.

- Private funds, not mutual funds. VC funds rely on exclusions from the Investment Company Act (most commonly 3(c)(1) or 3(c)(7)). In exchange, they limit who can invest and how marketing works. The tradeoff is more flexibility on strategy but tighter gates on access.

Adviser oversight: who polices the managers

VC regulation is adviser-centric: the rules focus on how managers behave more than what they buy.

- Registration status. Many pure VC firms rely on the venture capital adviser exemption and file as Exempt Reporting Advisers (ERAs)—a lighter regime with anti-fraud obligations and basic filings. Others register fully as investment advisers (for example, if they manage non-VC strategies or larger pools), which brings broader requirements.

- Fiduciary duty. Whether registered or exempt, advisers owe a core duty: act in clients’ best interests, disclose conflicts, and don’t mislead. That duty shows up in how fees are structured, how marks are set, how co-investments are allocated, and how performance is presented.

- Compliance program. Registered advisers must run written policies, appoint a Chief Compliance Officer, keep detailed records, and expect SEC examinations. ERAs face less formality but still live under anti-fraud rules and can be examined.

- Marketing discipline. Modern advertising standards allow testimonials and third-party ratings with conditions, and require that performance be fair, balanced, and substantiated. If you see “top-quartile” claims, the manager should have the calculations and datasets to back them up.

- Custody and audits. When an adviser can access client assets, custody safeguards apply. Many funds deliver annual audited financial statements to investors as a protection and to keep the “audit path” clean, even when not strictly required.

Investor takeaway: You don’t need to memorize the rulebook. You need to check for consistency (deck ↔ PPM ↔ LPA ↔ Form ADV), controls (valuation committee, audit, administrator), and evidence (workpapers behind performance and fees).

Fundraising rules: who can invest and how they’re verified

Venture funds raise capital through private placements, most often under two familiar routes:

- Quiet, relationship-based offerings (often using Rule 506(b)): No general solicitation. Managers rely on pre-existing relationships; investors typically self-certify eligibility in subscription documents.

- Public-facing private offerings (Rule 506(c)): General solicitation is permitted (websites, conferences, podcasts), but the fund must take reasonable steps to verify that each investor is eligible—typically through document review (income, net worth, or professional certifications) or a third-party verification letter. A checkbox alone isn’t enough.

Eligibility gates. You’ll encounter accredited investor tests (income/net worth or certain licenses) and, in some funds, qualified purchaser thresholds. Which gate applies depends on how the fund is structured (e.g., 3(c)(1) vs. 3(c)(7)).

State “blue sky.” While federal law preempts much state review for common private-offering routes, funds usually file notices and pay fees in states where interests are sold.

Secondaries and transfers. Interests in VC funds are typically restricted. Transfers often require GP consent and compliance checks (no blowing the eligibility limits).

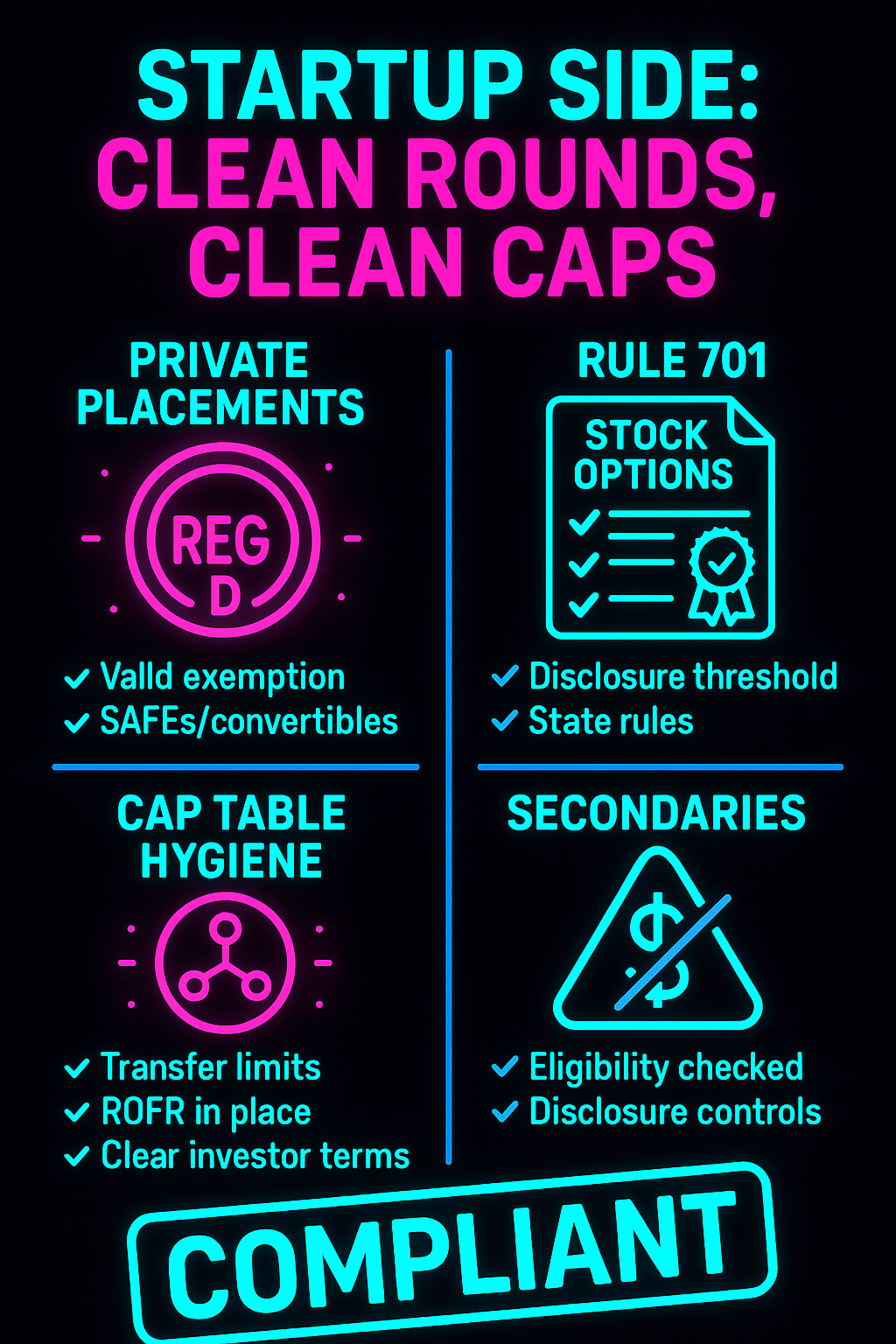

How startups raise money (and why those rules matter to VC)

Venture investors live on the other side of the trade too: the company’s fundraising. Understanding the company’s compliance makes you a better evaluator of risk.

- Private placements. Startups rely on private-offering exemptions (often Reg D) for priced rounds (preferred stock) and for SAFEs/convertible notes. Clean exemption use reduces rescission risk and regulatory headaches later.

- Employee equity. Compensatory grants are typically made under Rule 701 or equivalent state exemptions. As companies scale, 701 requires better disclosures; sloppy compliance can become a problem in diligence before a big round or IPO.

- Cap table hygiene. Transfer restrictions, right-of-first-refusal (ROFR), and information rights live in company documents. Early mistakes (uncapped notes, ambiguous SAFEs) can snarl later financings.

- Secondary sales. As companies mature, employees and early investors may sell shares in secondary transactions. These are still securities sales, and they raise questions about information rights, legends, and buyer eligibility.

What’s inside the fund documents (and how to read them)

The private placement memorandum (PPM) and limited partnership agreement (LPA) are the rulebook. A straightforward way to read them:

- Economics. Management fee schedule (rate, step-downs), carried interest (carry %, preferred return if any, clawback mechanics), and the order of cash distributions (the “waterfall”).

- Investment program. Stage, sector, check size, geography, and follow-on policy. Pay attention to concentrationlimits and whether there’s flexibility to hold public shares post-listing.

- Conflicts and allocations. Co-investment policy, cross-fund transactions, partner personal investing rules, and affiliated service providers. You’re looking for identify → disclose → monitor → mitigate.

- Valuation. Methodology under fair-value accounting (e.g., ASC 820), calibration to recent rounds, and who sits on the valuation committee. Back-testing (comparing realized exits to prior marks) is a good sign.

- Fees and expenses beyond “2 and 20.” Organizational expenses, transaction and monitoring fees (rare in classic VC but common in growth equity), broken-deal costs, and who pays for data, travel, and compliance. Look for offsets and caps.

- Reporting cadence. Quarterly letters, capital account statements, annual audits, and whether the fund provides an investor portal with historical data.

- Liquidity and transfers. Lockups, in-kind distributions, and GP consent standards for transfers. VC funds are long-dated and illiquid by design.

- Side letters and MFN. Large investors often negotiate side letters (fee breaks, reporting, ESG reporting, or capacity). An MFN (most-favored-nation) process lets similarly situated LPs elect comparable terms.

Simple test: Ask the manager to walk you through a numerical example—one investment that failed and one that succeeded—and show how fees, carry, and expenses flowed through to LPs.

Tax concepts that matter (without the jargon)

- Qualified Small Business Stock (QSBS / Section 1202). Stock of certain C-corps held for five years can be eligible for partial or full exclusion of gains, subject to strict requirements (business type, asset thresholds, original issuance, and more). This is a powerful driver of after-tax returns in early-stage investing.

- 83(b) elections. Founders and early employees receiving restricted stock often file an 83(b) election to start the capital-gains clock and tax the current (often low) value now. Missing the 30-day window can be expensive later.

- Carried interest. Gains allocated to the GP are generally capital gains if the underlying gains are capital, but a three-year holding period rule can recharacterize some carry to short-term. It affects waterfalls and how managers plan exits.

- State taxes and withholding. Multi-state operations can create a thicket of state filings for funds and LPs. Some funds handle composite returns or make withholding payments; others push filings to investors.

No one expects LPs to be tax wizards, but you should understand the direction of these items and how the fund handles them in practice.

Risk areas where regulation and reality often clash

Fees and expenses that don’t match disclosures.

The most common exam findings involve expenses charged to funds that should have been borne by the manager, or fee offsets that weren’t applied as promised. Ask for a sample fee-offset calculation.

Valuation drift.

Private markets require judgment. A disciplined process—methodology, committee minutes, calibration, and back-testing—reduces disputes and surprises.

Co-investment fairness.

Co-investments help with concentration and support big rounds, but they also introduce allocation choices. Good policies explain who gets invited, when, and why, with a clear record.

Use of testimonials and performance stats.

If a pitch uses testimonials or “top-quartile” claims, the manager should have supporting records and present context (net vs. gross, vintage and benchmark definitions, and what’s included/excluded).

Cybersecurity and vendor risk.

VC firms are small but handle sensitive data. Expect multi-factor authentication, access reviews, incident-response testing, and vendor diligence (including administrators, custodians, cloud providers, and data rooms).

Sanctions/export controls and sensitive tech.

Investing in frontier tech can raise export-control and sanctions diligence questions (who are the end users, where is the tech going). These issues surface in round documentation and later exits.

The global picture (quick, practical version)

Venture capital is global, but fundraising and manager oversight are local:

- Europe/UK. Alternative investment manager rules set authorization, disclosure, and reporting expectations. Non-local managers often use private placement regimes to market to professional investors country by country. Some countries run foreign-investment screening for sensitive sectors alongside merger control.

- Asia hubs. Jurisdictions such as Singapore and Hong Kong operate modern fund vehicles and licensing regimes aimed at professional investors. Marketing is typically restricted to qualified/professional classes, with local notices and documentation.

- North America beyond the U.S. Canada blends merger control with national-interest reviews; fundraising follows provincial and federal securities rules. As in the U.S., funds generally target accredited/professional investors.

- Sanctions, data, and privacy. Cross-border rounds bring data-transfer rules (e.g., GDPR/UK GDPR concepts), and screening for prohibited parties becomes a standard onboarding step.

Investor takeaway: When a fund markets globally, ask for the jurisdiction matrix—where they can solicit, what filings are done, and how verification works in each place.

The startup compliance stack (investors should check this too)

- Company formation and equity plan. Clean charter documents, a board-approved option plan, and consistent grant practices (pricing, vesting, approvals).

- Information rights and financials. If you’re investing, what reporting will you receive and when? Early-stage reporting may be light; growth rounds usually expect quarterly financials and key metrics.

- IP ownership and assignments. Founders, employees, and contractors should have signed IP assignmentagreements. Open-source use policies matter, especially for developer-heavy teams.

- Employment and contractor rules. Classification (employee vs. contractor), offer letter practices, and any works-council or local notice obligations in other countries.

- Data and security. If the product handles personal or health data, expect privacy policies, vendor contracts, and basic security controls. Investors should sniff-test the posture, even at seed.

A surprising amount of later legal pain comes from early sloppiness. Fixing it is always cheaper before the next round, not during it.

How to diligence a VC manager in 60 minutes

- Strategy and edge (10 min). Stage, sector, check size, sourcing, decision process, and what they do post-investment.

- Team and incentives (10 min). Who owns carry, vesting/clawback, and how the team shares economics across funds.

- Track record (10 min). Realized vs. unrealized, loss ratio, DPI/TVPI multiples, how marks are set, and what changed after misses.

- Operations (10 min). Auditor, administrator, valuation committee, cyber posture, and exam history/remediation.

- Fees and expenses (10 min). Rate and step-downs, org-expense cap, offset mechanics, and one worked example with numbers.

- Legal and reporting (10 min). PPM/LPA consistency, side-letter/MFN approach, reporting templates, audit timing, and portal access.

You’re listening for fluency, consistency, and documents that match the story.

A quick glossary for the most common acronyms

- 3(c)(1) / 3(c)(7): Exclusions from the Investment Company Act used by private funds to avoid mutual-fund-style regulation.

- 506(b) / 506(c): Private-offering routes under Regulation D (no solicitation vs. solicitation with verification).

- Accredited Investor / Qualified Purchaser: Eligibility thresholds used for private offerings and certain fund structures.

- ERA / RIA: Exempt Reporting Adviser vs. Registered Investment Adviser (two different compliance footprints).

- LPA / PPM: Limited Partnership Agreement and Private Placement Memorandum (the governing documents).

- SAFE / Note: Common early-stage financing instruments that convert into equity later.

- ASC 820: U.S. fair-value accounting standard used for marking private assets.

- QSBS / 1202: Potential gain exclusion for qualifying stock of certain small C-corps held for five years.

- 83(b): Election to tax restricted stock at grant, starting the capital-gains clock.

Practical red flags (and green lights)

Red flags

- Fees/expenses described one way but charged another.

- Vague co-investment policy or inconsistent invitations.

- Performance presented only as “gross,” no backup, or cherry-picked subsets.

- Valuation marks that never move, then jump at exit.

- No auditor or repeated auditor changes without a clear reason.

- Defensive answers to routine diligence questions (“we don’t share that”).

Green lights

- Calm, specific walk-throughs of fees, offsets, and a realized case study.

- Valuation committee minutes, back-testing examples, and clear methodology.

- Document set is consistent; changes after exams are explained plainly.

- Cyber and vendor due diligence with recent tabletop exercises.

- Investor portal with historical letters, audits, and capital statements.

Bottom line

Venture capital isn’t lawless—it’s principles-based. Regulators set the guardrails: who can invest, how managers market, how conflicts and fees are handled, and how performance is presented. Startups rely on private-offering rules and employee-equity exemptions; funds operate under adviser duties and fair-value accounting; cross-border capital follows local distribution and investment-screening regimes.

For investors, the winning approach is simple:

- Read for consistency across the deck, PPM, LPA, and public filings.

- Ask for evidence behind performance and fees (and expect real numbers).

- Check controls: audits, valuation process, administrator, cyber posture.

- Understand your eligibility and how verification works.

- Know the tax basics (QSBS, 83(b), carry horizon) that drive after-tax returns.

Do that, and you’ll replace jargon with judgment—and turn a complicated landscape into a clear set of questions that smart managers are happy to answer.

{kind=link}