In recent years, private credit has shifted from being a niche alternative investment to one of the fastest-growing asset classes in the world. Once dominated by banks and a handful of institutional lenders, the private credit market is now a $1.5 trillion industry, projected to more than double by the end of the decade. For investors, the question isn’t whether private credit is here to stay—it’s why the demand for this asset class has exploded and what makes it so compelling in today’s financial environment.

This article builds on the insights shared in our pillar piece, What Is Private Credit? An Investor’s Guide, by examining the underlying forces driving growth and why investors are increasingly allocating to private credit strategies.

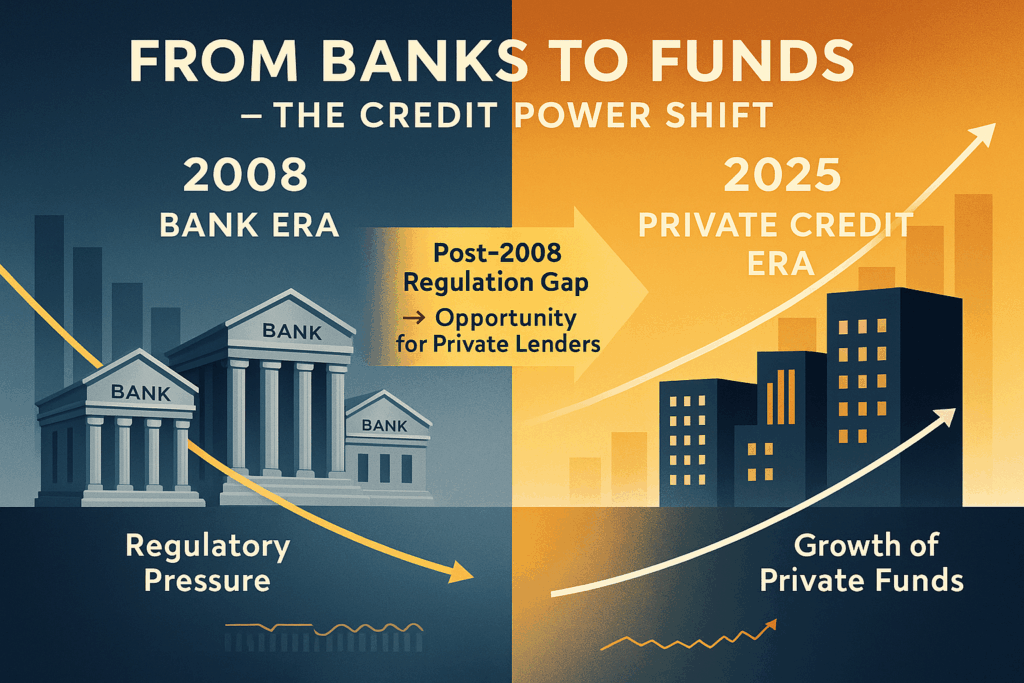

1. Retreat of Traditional Banks

One of the clearest drivers of private credit’s rise is the pullback of traditional banks from middle-market lending. After the 2008 global financial crisis, regulators imposed stricter capital and lending requirements on banks, limiting their ability to provide loans to riskier borrowers.

This created a financing gap for small and mid-sized businesses—companies too large for community banks but too small to tap public debt markets. Private credit funds stepped in, filling the void with flexible capital and faster execution. Over time, borrowers came to prefer the tailored structures private lenders could offer, and banks never regained their dominance in this corner of lending.

2. Investor Demand for Yield

Bond yields have struggled for much of the past 15 years. Even with the Federal Reserve raising interest rates in recent cycles, returns on traditional fixed-income investments often lag inflation.

Private credit, by contrast, consistently offers yields in the 8–12% range for direct lending and even higher for mezzanine or distressed strategies. For pension funds, insurers, endowments, and wealthy individuals seeking dependable income, private credit represents a rare combination of high yield and relatively stable performance.

The floating-rate structures common in private credit also help shield investors from interest-rate risk, making it attractive in both low- and high-rate environments.

3. Portfolio Diversification

Investors have learned that private credit behaves differently from public markets. Unlike bonds or stocks that trade daily and respond to headlines, private loans are illiquid and valued less frequently.

This reduced mark-to-market volatility helps smooth portfolio performance. Even during market turbulence, private credit returns tend to remain more stable, provided the underlying borrowers remain sound. As a result, institutions often allocate 5–15% of their portfolios to private credit as a diversifier alongside equities, real estate, and public fixed income.

4. Tailored Lending Solutions for Borrowers

From the borrower’s perspective, private credit is appealing because it’s faster, more flexible, and more customized than public debt. Private lenders can structure loans around the borrower’s needs—whether that’s delayed amortization, covenant-light terms, or financing tied to specific growth milestones.

This flexibility allows businesses to access capital when they might not qualify for traditional bank loans or public bond issuance. For investors, the benefit is twofold: not only are they meeting real demand, but the bespoke structures often come with higher yields and stronger covenant protections.

5. A Shift Toward Alternatives

Private credit’s rise is also part of a broader shift toward alternative assets. With public equity markets increasingly volatile and government bonds offering limited returns, institutions are seeking new sources of uncorrelated performance.

Private equity, infrastructure, hedge funds, and real estate have all benefited, but private credit stands out because it offers contractual cash flows, downside protections, and attractive yields. In many ways, it combines the income characteristics of bonds with the higher-return potential of private equity—without the same level of volatility.

6. Global Expansion

While private credit initially grew in North America, it has rapidly expanded into Europe and Asia. In Europe, bank retrenchment has been even more pronounced, creating fertile ground for direct lenders. In Asia, the rise of family-owned conglomerates and emerging-market growth stories is fueling demand for alternative financing.

For investors, this globalization means more opportunities, greater diversification, and exposure to different credit cycles. It also signals that private credit is not just a U.S. phenomenon but a permanent fixture of the global capital markets.

7. Technology and Transparency

Historically, private markets were criticized for being opaque. But advances in fintech, reporting platforms, and third-party data providers have improved transparency and accessibility. Investors can now track portfolio performance, benchmark against peers, and receive more frequent reporting.

This technological shift has made institutional investors more comfortable allocating significant capital, accelerating growth further.

8. Risks Remain

Despite its popularity, private credit isn’t without risks. Illiquidity is the most obvious—capital is often locked up for 5–10 years, with limited opportunities for redemption. Borrower defaults can also spike during recessions, and recovery processes in private deals are slower than in public bond markets.

Additionally, as more capital flows into the space, there’s concern that underwriting standards could loosen, leading to weaker protections and lower risk-adjusted returns. Investors must be selective, focusing on experienced managers with disciplined credit processes.

The Bottom Line

Private credit has grown because it solves problems for both sides of the table. Borrowers get access to flexible, tailored capital, while investors gain higher yields, diversification, and insulation from daily market swings.

As highlighted in What Is Private Credit? An Investor’s Guide, the industry has matured into a mainstream allocation for institutions and high-net-worth investors alike. While risks remain—particularly illiquidity and credit-cycle exposure—the growth of private credit reflects deeper structural changes in the financial system.

For investors, understanding these drivers is key. Private credit isn’t just a passing trend; it’s a reshaping of how capital flows in the modern economy, offering opportunities for those willing to commit capital long-term.

{kind=link}