This Content Is Only For Subscribers

The SEC doesn’t regulate private equity (PE) funds the way it regulates mutual funds. Instead, it regulates the advisers who run them—the management companies behind the general partner (GP). That distinction matters. It means SEC oversight focuses on how managers behave, what they disclose, and how they handle investors’ money, rather than prescribing what a fund can or can’t buy. If you’re a newer investor considering PE, here’s a clear, plain-English map of what the SEC looks for and what you should ask.

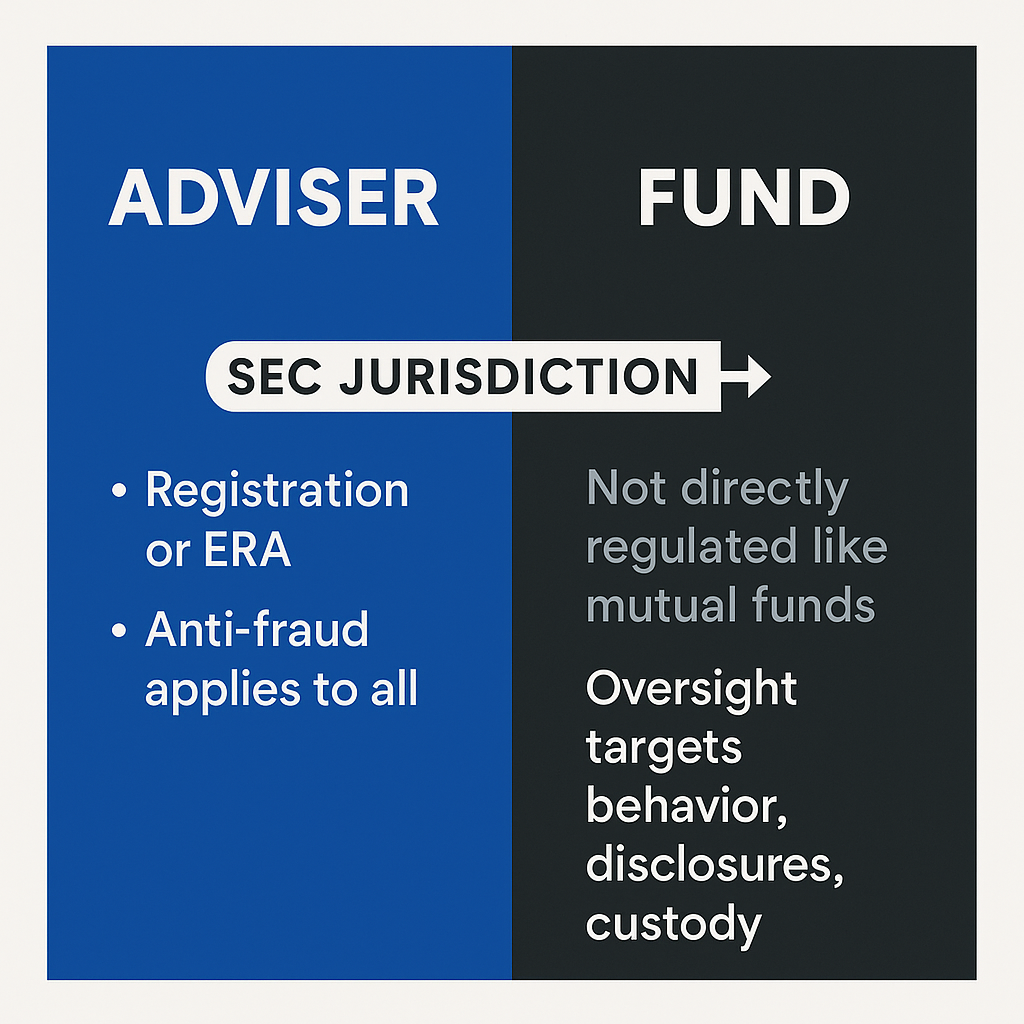

Who the SEC Oversees (and how)

Investment adviser vs. fund.

Legally, the SEC’s jurisdiction lives with the adviser (the management company), not the limited partnership itself. Most sizable PE advisers register as investment advisers with the SEC; some smaller or specialized firms qualify as Exempt Reporting Advisers (ERAs) and file lighter reports. Either way, anti-fraud rules apply to everyone.

Fiduciary duty: the headline concept.

Registered advisers owe a fiduciary duty of care and loyalty. Boiled down: act in investors’ best interests, disclose conflicts plainly, and don’t mislead. This duty informs everything—valuation policy, fee practices, co-investment allocations, even the tone of marketing materials.

Policies, a real CCO, and exams.

SEC-registered advisers must maintain written policies and procedures, appoint a Chief Compliance Officer (CCO)with real authority, and expect examinations. Examiners don’t just read the manual; they test whether it works—sampling emails, marketing claims, expense allocations, and valuation decisions. Most exams end with a deficiency letter (a fix-it list) that the adviser must remediate.

What the SEC Looks At (day to day)

1) Fees, expenses, and offsets

Private equity has more moving parts than a simple “2 and 20.” There can be transaction fees, monitoring fees at portfolio companies, broken-deal costs, compliance and data expenses, and co-investment vehicle costs. The SEC’s question is simple: Did investors get what they were promised? Common focus areas:

- Are portfolio-company fees offset appropriately against management fees (as disclosed)?

- Are broken-deal costs allocated fairly among funds and co-investors?

- Are accelerated monitoring fees or termination fees at exit clearly disclosed and consistent with governing documents?

- Do expense caps or “ordinary course” definitions match practice?

2) Valuation and performance

PE funds report fair value each quarter, and that number flows into performance and sometimes fees. The SEC expects a documented process: methodologies, calibration to transaction prices, third-party data where relevant, a valuation committee, and back-testing (comparing realized exits against prior marks). If performance is marketed, the adviser must be able to substantiate it and present it fairly.

3) Conflicts of interest

Conflicts are normal in PE: multiple funds chasing similar deals, cross-fund transactions, stapled secondaries, use of affiliated service providers, fee breaks in side letters, and allocation of scarce co-investment capacity. The SEC standard isn’t “no conflicts”; it’s identify, disclose, monitor, and mitigate. The firm should keep conflict logs, committee minutes, and allocation policies that show how decisions were made.

4) Marketing and the “show your work” rule

Under the modern marketing rule, testimonials and third-party ratings can appear—with conditions—and hypothetical or model performance requires extra controls and audience limits. Any material claim (alpha, win rate, “top quartile”) needs backup. Books-and-records rules mean the firm must retain that backup.

5) Custody and audits

Because advisers typically control fund assets, custody safeguards apply. Many PE funds follow the “audit path”: annual financial statements audited by an independent public accountant and delivered to investors on time. Others may undergo surprise examinations. Either way, the objective is the same—protect investors’ money and verify what’s reported.

6) Form ADV and Form PF

- Form ADV (public) is the adviser’s “brochure”—strategies, fees, conflicts, disciplinary history, and key people, written in plain English. It’s the first thing you should read.

- Form PF (non-public) reports fund-level risk data (leverage, liquidity, exposures) so regulators can monitor systemic risk. You won’t see it, but it shapes the SEC’s risk priorities.

What “Good” Looks Like

You can recognize a healthy compliance culture without being a lawyer:

- Clear, consistent documents. The private placement memorandum (PPM), limited partnership agreement (LPA), and side letters all tell the same story as the pitch deck and website. No surprises.

- Independent checks. A credible auditor signs the annuals; a reputable administrator handles capital accounts and cash controls; valuation committees meet and keep minutes.

- Evidence on request. Ask for a sample valuation memo, a fee-offset calculation, or the backup behind a performance graphic. Good managers hand it over calmly.

- Exam maturity. If the firm was examined recently, they can summarize findings and what changed. Defensive or vague answers are a yellow flag.

Common Trouble Spots (and how to spot them)

- Invisible fees/expenses. If netting and offsets are explained in prose but never shown in numbers, push for an illustration.

- Valuation drift. Marks that never move until an exit—then surprise—are a sign to ask about methodology and calibration.

- Side-letter fairness. Side letters for big investors are normal; MFN processes that let similarly situated LPs elect comparable terms are a good sign of fairness.

- Co-investment allocation. Ask for the policy and a real example. “Case-by-case” is fine if there’s a paper trail.

- Recordkeeping gaps. If the firm can’t produce the documentation behind claims or allocations, the SEC won’t be amused—and you shouldn’t be either.

A 10-Question Diligence Script

Use this to turn SEC oversight into practical questions:

- Registration & exams: Are you SEC-registered or an ERA? When was your last exam, and what did you change afterward?

- CCO authority: Who is your CCO, and do they have direct access to leadership and the investment committee?

- Fees & offsets: Walk me through how transaction/monitoring fees flow back to the fund and show me one offset calculation.

- Broken-deal costs: How are they allocated across funds and co-investors?

- Valuation: Who sits on the valuation committee? Show me a memo and any back-testing from last year’s exits.

- Conflicts log: What are the most common conflicts here? How do you document and resolve them?

- Co-investments: What’s your allocation policy? Please share one anonymized example.

- Marketing backup: For this performance chart, can I see the support and the net-of-fee calculation?

- Custody path: Audit or surprise exam? Have audited financials been delivered on time each year?

- Service providers: Who are your auditor and administrator? How long have they served, and how do you evaluate them?

You’re listening for fluency, specifics, and documents that match the story.

Bottom Line

SEC oversight of private equity isn’t about dictating strategy. It’s about guardrails: fiduciary duty, truthful marketing, fair fees and expenses, disciplined valuation, custody safeguards, and good recordkeeping—tested through examinations and supported by public (Form ADV) and confidential (Form PF) reporting. As an investor, you don’t have to memorize the rules. You just need to use them as a lens: ask targeted questions, request evidence, and look for consistency between disclosure and behavior. The best managers welcome that scrutiny—because strong process is part of their edge.

{kind=link}