This Content Is Only For Subscribers

Hedge funds often make headlines for spectacular wins or stunning blow-ups. But what happens when you look at the average hedge fund? How does it compare with a simple benchmark like the S&P 500?

The answer surprises many beginners: over long periods, the S&P 500 has usually outperformed the average hedge fund on raw returns. That doesn’t mean hedge funds are “bad”—it just means they’re built for a different purpose. Understanding that distinction is key for any investor.

Apples and oranges

- S&P 500: A broad basket of U.S. large-cap stocks. It’s long-only, fully invested, and easy to track with index funds. Returns move with the market.

- Hedge funds: Not a single strategy, but a category. They may trade stocks, bonds, currencies, or derivatives, use short selling, and carry leverage. They aim to limit downside risk and diversify, but typically charge high fees.

So the comparison isn’t apples to apples. It’s more like a sports car versus a rally car: one tuned for speed on a straight road, the other for handling bumps and curves.

Why the S&P often wins on returns

- Equity power – U.S. stocks have been strong over time. Staying fully invested captures that.

- Fees – Hedge funds’ higher fees (“2 and 20,” though often lower now) eat into returns.

- Diversification trade-off – Balancing risk across assets dilutes gains in long bull markets.

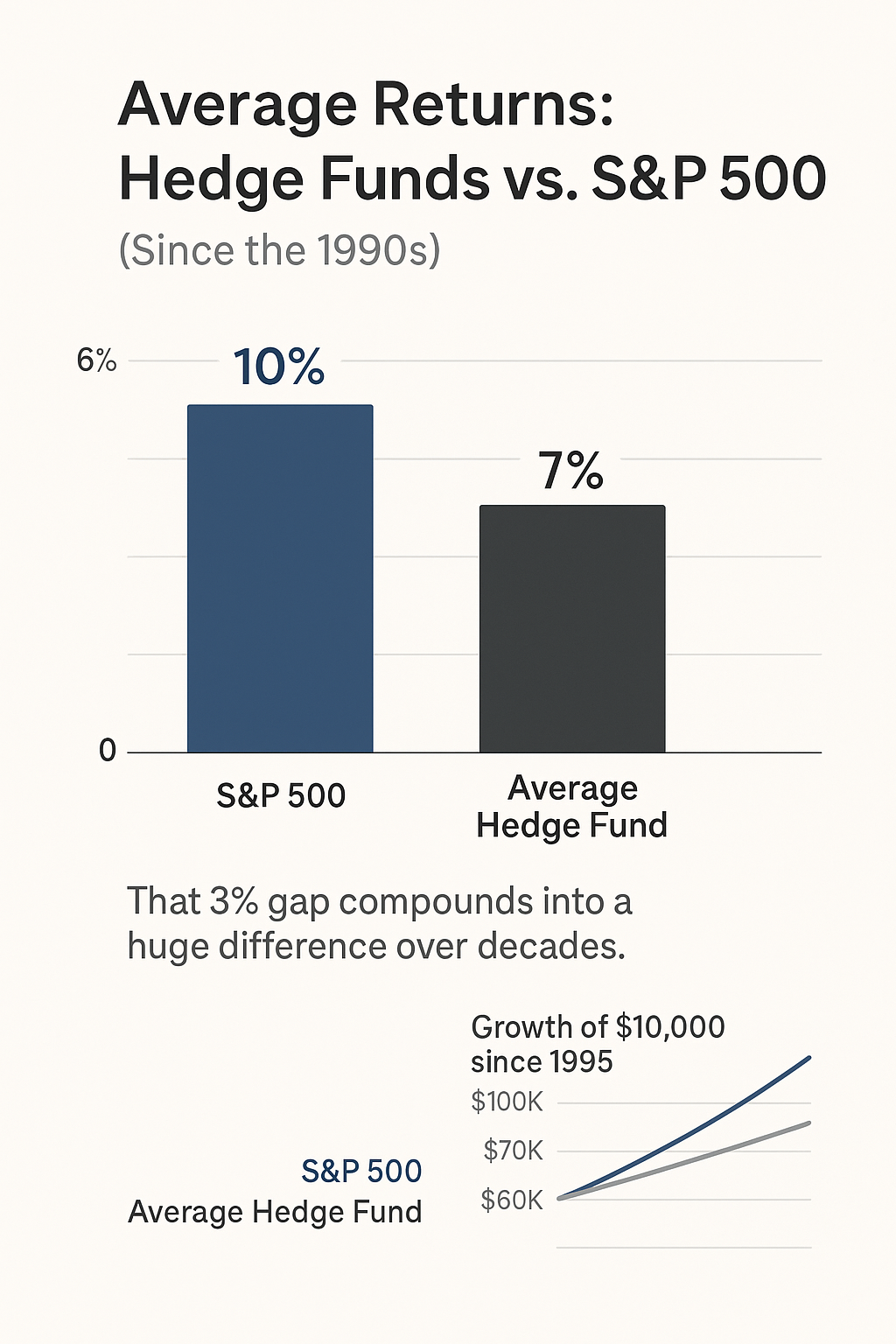

Since the mid-1990s, hedge fund indexes have returned around 7% annually, versus nearly 10% for the S&P 500. That small difference compounds enormously: over 25 years, $10,000 in the S&P would grow to more than $100,000, while the hedge fund index would be closer to $60,000.

Why hedge funds exist anyway

Institutions don’t just chase the highest return—they care about the path. Hedge funds aim to:

- Reduce volatility,

- Limit drawdowns,

- Diversify away from stock-heavy risk.

That can look disappointing in bull markets, but valuable in turbulence.

For example, in the 2000s “lost decade”, the S&P 500 delivered a negative return overall, weighed down by the dot-com bust and the 2008 crisis. Many hedge funds, while far from perfect, posted mid-single-digit annual gains, making them look attractive. In the 2010s, however, the S&P roared ahead at more than 13% annually, easily outpacing hedge funds’ ~5%.

Buffett’s famous bet

This contrast was highlighted by Warren Buffett’s 2008–2017 wager against hedge funds. Buffett bet $1 million that an S&P 500 index fund would outperform a basket of hedge funds over ten years. When the decade ended, the index fund had gained about 7% a year, while the hedge funds managed only ~2%.

For Buffett, the point wasn’t that hedge funds were “bad,” but that for most investors, low-cost index funds are a better default choice.

Risk-adjusted returns

Professionals rarely ask, “Who had the highest return?” They ask, “Who took the least risk to earn a return?” Hedge funds usually post lower volatility and smaller drawdowns than the S&P. On a risk-adjusted basis, their records can look stronger—even if headline returns are weaker.

Take 2008: the S&P 500 plunged about 37%. Many hedge fund indexes fell too, but by less—around 20%. That’s still painful, but losing 20% instead of 37% can mean staying invested rather than panicking out of the market.

This “smoother ride” is one reason pension funds and endowments commit money to hedge funds. They can’t afford the same drawdowns that an individual with a 30-year horizon might tolerate.

Beyond U.S. stocks: why institutions care

It’s also worth remembering that the S&P 500 is just U.S. large-cap equities. Hedge funds often invest globally and across asset classes—emerging market currencies, distressed debt, commodities, or merger-arbitrage deals.

For a U.S. retiree, the S&P 500 may be the best starting point. But for a sovereign wealth fund in Asia or a European pension, hedge funds provide access to opportunities and risk exposures that aren’t captured by American stocks.

So while hedge funds as a group may lag the S&P 500, they can still add value to a diversified global portfolio.

Averages can mislead

When you hear “hedge funds underperform,” remember:

- Indexes blend very different strategies.

- Survivorship and reporting bias can skew results.

- The best funds are often closed to outsiders.

So “average hedge fund” numbers hide both stars and strugglers. Some funds have built extraordinary long-term records, but they are exceptions rather than the rule.

What it means for novices

Here are some practical ways beginners can apply these lessons:

- Use the right yardstick. If your goal is growth, and you can handle volatility, a low-cost S&P 500 index fund is a strong foundation.

- Mind fees. Paying 1–2% more in annual costs may not sound like much, but over 30 years it can mean tens of thousands of dollars less in your account.

- Diversify smartly. If you want smoother performance, add bonds, international stocks, or even cash reserves. These can blunt volatility without needing hedge fund access.

- Learn from risk-adjusted thinking. Don’t just chase the stock with the biggest upside. Ask yourself: “What happens if I’m wrong?”

- Stay disciplined. The best strategy is one you can stick with in both booms and busts.

Example: If you invested in the S&P 500 in January 2008 and sold in panic by March 2009, you would have locked in heavy losses. But if you stuck to your plan, you would have recovered and then some. The lesson: discipline beats timing.

Bottom line

The S&P 500 often outpaces the average hedge fund in raw returns. But hedge funds aren’t just about speed; they’re about shaping the ride. For institutions with billions to protect, that tradeoff makes sense. For most beginners, the practical takeaway is simpler: build around low-cost index funds, add sensible diversifiers, and remember that consistency and patience matter more than chasing miracles.

{kind=link}