This Content Is Only For Subscribers

Crypto funds used to be a niche curiosity—small pools of capital buying and holding digital assets for a handful of believers. Today they look much more like mainstream investment vehicles: institutional custody, audited financials, risk committees, and increasingly sophisticated strategies. What hasn’t changed is the puzzle of regulation. Crypto sits at the crossroads of securities law, commodities rules, banking oversight, payments regulation, tax, and anti–money laundering requirements. If you’re new to this space as an investor, this guide walks the terrain in plain, practical language: who the referees are, what rules shape your experience, and how to separate signal from noise when you diligence a manager.

A two-minute map: where the rules come from

- Securities regulation: When a crypto asset or a fund’s interests are deemed securities, traditional securities laws apply: private-offering rules for fundraising, advertising/marketing limitations, and anti-fraud standards covering performance claims and disclosures. Investment advisers (the management company behind a fund) may be fully registered or rely on exemptions; either way, they live under fiduciary obligations.

- Commodities and derivatives: Certain crypto assets trade on futures markets and fall under derivatives rules. Funds using futures, options, swaps, or margin are subject to additional registration, reporting, and conduct requirements—even if the underlying spot asset is decentralized.

- Banking and payments: Stablecoins, fiat on-ramps/off-ramps, and some yield-bearing products implicate money transmission, e-money, or payments regulation. That mostly affects exchanges and service providers—indirectly shaping a fund’s operations.

- Anti–money laundering (AML) and sanctions: Know-your-customer (KYC) checks, transaction monitoring, and sanctions screening are table stakes for reputable funds and their service providers. Wallet screening and blockchain analytics are now routine.

- Tax: The tax code treats different crypto activities differently (trading vs. staking vs. derivatives vs. airdrops). Funds generally pass income and gains through to investors, so characterization and reporting quality matter.

- Global rules: Jurisdictions vary widely—from comprehensive licensing regimes to light-touch innovation zones. Cross-border investing adds layers for marketing, investor eligibility, data transfers, and sanctions.

You don’t need to memorize statutes. You do need to understand the themes that shape how good managers operate.

How crypto funds are structured (and why it matters)

Most crypto funds look like traditional private funds: limited partnerships or LLCs taxed as partnerships. Investors (limited partners, or LPs) commit capital to a fund managed by an adviser (the management company behind the general partner). Three structural choices shape your experience:

- Strategy:

- Directional/long-only: Buy and hold Bitcoin, Ether, or baskets (“index-style”).

- Quant/market-neutral: Arbitrage, basis trades, liquidity provision, high-frequency strategies.

- Venture/early-stage: Tokens or equity in builders, often under lockups or vesting schedules.

- Income/yield: Staking, lending, liquidity mining—areas that raise extra legal and operational questions.

- Offering route and investor gates:

Funds typically raise capital through private placements, often limited to accredited or professional investors. Some structures also require “qualified purchaser” status. The route a manager chooses affects whether they can publicly market (and what evidence you must provide to verify eligibility). - Domicile:

Onshore (e.g., U.S., EU, UK) vs. offshore (e.g., Cayman, BVI, Bermuda, Guernsey) affects regulation, service-provider choices, and tax reporting. Many managers run master-feeder structures (U.S. feeder, offshore feeder, master fund) to accommodate both taxable and tax-exempt or non-U.S. investors.

Investor takeaway: Ask for a one-page structure diagram and a plain-English explanation of where the fund is formed, who the service providers are, how assets are custodied, and what laws the adviser is subject to.

Adviser oversight: what “good” looks like

Even in crypto, the core of oversight is adviser-centric: regulators focus on how managers behave more than what they buy.

- Fiduciary duty: Registered advisers—and many exempt ones by policy—operate under duties of care and loyalty. That means avoiding misleading statements, managing conflicts, and charging only those fees and expenses promised in the documents.

- Compliance program: Written policies, a real Chief Compliance Officer (CCO), periodic testing, and a books-and-records system that captures orders, trade rationales, valuation memos, and marketing backups (especially for performance claims).

- Marketing discipline: If a deck or website touts “top-quartile” results or eye-popping Sharpe ratios, the team should be able to show the work—calculations, benchmark definitions, net-of-fee treatment, and inclusion/exclusion rules. Testimonials and third-party ratings are possible in some regimes but require specific disclosures and controls.

- Custody controls: In crypto, custody is existential. Strong managers segregate client assets, use qualified custodians or institutional-grade wallets with multi-party computation (MPC), require multiple approvals for transfers, and log every move. Many provide annual audited financial statements as an investor safeguard.

- Valuation governance: For actively traded tokens, pricing may be straightforward. For thinly traded assets, locked tokens, side pockets, or venture positions, the fund needs a methodology (pricing hierarchies, liquidity and discount frameworks, and back-testing against realized exits).

Investor takeaway: Ask for a recent audit letter, the custodian name(s), a summary of wallet policies (signers, thresholds, whitelists), and a sample valuation memo for an illiquid position.

Trading venues, market structure, and counterparty risk

Crypto market structure is unlike equities:

- Venue diversity: Spot trading often occurs on centralized exchanges; derivatives may trade on regulated futures venues or offshore platforms. Liquidity can be fragmented across regions, venues, and pairs.

- Counterparty tiers: Funds balance spread capture with counterparty safety: prime brokers, custodians with off-exchange settlement, and venues that support “cold-to-warm” transfer flows to minimize hot-wallet exposure.

- Settlement mechanics: In traditional markets, clearinghouses reduce bilateral risk. In crypto, settlement often happens at the venue, which concentrates risk. Good managers mitigate with pre-trade margin controls, withdrawal testing, and limits on exchange balances.

- On-chain execution: DeFi protocols enable swaps, lending, and liquidity provision directly on blockchains. That adds smart-contract risk and oracle dependencies; leading funds use protocol reviews, time-locked governance monitoring, and position limits.

Investor takeaway: Demand a counterparty framework—approved venues, capital limits per venue, criteria for onboarding/offboarding, and how the fund monitors solvency and withdrawals, especially in stress.

Stablecoins, staking, and yield—where rules meet innovation

Three areas deserve special attention:

- Stablecoins:

They’re vital for settlement and liquidity but raise questions: asset backing, redemption rights, reserve transparency, and jurisdictional treatment. Good funds restrict usage to well-capitalized, transparent issuers and keep concentration limits. - Staking:

Staking rewards look like yield but are protocol emissions tied to network security. Key questions: Who controls validator keys? How is slashing risk managed? Are rewards treated as income or as adjustments to basis (and how does the fund account for that)? - Lending and rehypothecation:

Off-chain lending can introduce hidden leverage and re-use of collateral. On-chain lending introduces smart-contract and oracle risk. A prudent fund discloses whether assets leave cold custody, the rehypothecation policy, and collateral waterfall in a counterparty default.

Investor takeaway: If a strategy promises “safe yield,” ask for a risk matrix that breaks down credit risk, protocol risk, liquidity risk, and operational risk—with limits and stop-loss triggers for each.

AML, sanctions, and data privacy—quiet but critical

A mature crypto fund’s onboarding and monitoring will feel familiar:

- KYC/AML: Collecting and refreshing investor documentation; screening against sanctions lists; verifying source of funds.

- Transaction monitoring: Using blockchain analytics to flag exposure to sanctioned addresses, mixers, or high-risk services; documenting overrides.

- Privacy and data: Handling personal data under local privacy laws; controlling access to investor information and trading data.

Investor takeaway: Ask which analytics tools are used, how alerts are triaged, and how long records are retained. These aren’t check-the-box questions; they indicate whether the firm can scale safely.

Accounting, audits, and reporting

Crypto creates unique accounting wrinkles:

- Fair value: For liquid tokens, independent pricing feeds may be sufficient; for thin markets, price discovery requires conservative hierarchies and documented discounts.

- Principal–agent clarity: If a manager trades across multiple funds or accounts, allocation policies and trade tickets must show fairness.

- Financial statements: Annual audits, capital account statements, and clear fee/expense detail are non-negotiable for institutional LPs.

- Tax packages: Investor K-1s (or local equivalents) should categorize income, gains, and losses appropriately and provide the detail tax preparers need.

Investor takeaway: Review a sample investor statement and audit timeline. If the fund promises monthly NAVs, ask how often illiquid positions are re-marked and who approves changes.

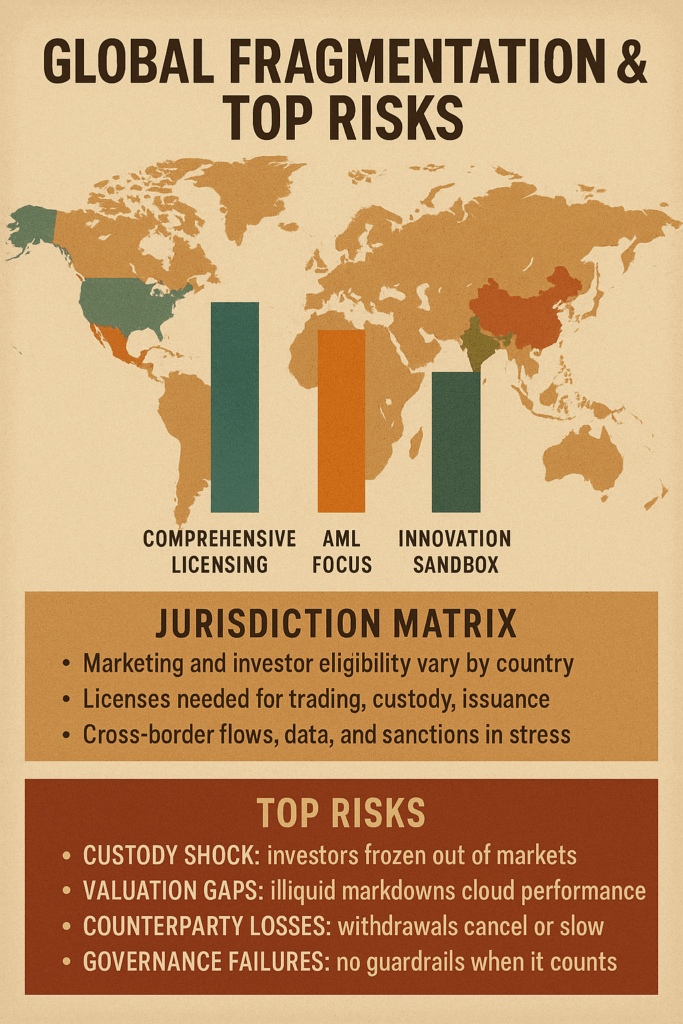

Global fragmentation: same melody, different lyrics

There is no single global crypto rulebook. Some jurisdictions have comprehensive licensing for trading, custody, and issuance; others focus on AML; others build “regulatory sandboxes” to supervise innovation. What this means for you:

- Marketing and investor eligibility are local. A manager allowed to solicit in one country may need separate approvals elsewhere—even for the same fund.

- Service-provider availability varies. Certain custodians, banks, and administrators operate only in select jurisdictions; that can affect onboarding times and operational resilience.

- Cross-border transfers add frictions. Data localization, sanctions screening, and reporting regimes can slow or block money movement in crisis scenarios—important when liquidity is everything.

Investor takeaway: For global managers, ask for a jurisdiction matrix listing where they can legally market, where investors are located, which filings are done, how they handle cross-border data flows, and what happens in a sanctions event.

Where the biggest risks hide (and how to assess them)

- Custody leakage:

The simplest test is: Can you show me, today, where the assets are and who can move them? Look for segregated wallets, whitelists, multi-approver policies, and transfer logs reviewed by someone not involved in trading. - Counterparty creep:

Yield often comes from counterparty risk. Ask for a top-ten exposure report by venue and borrower, with limits and rationale. - Valuation optimism:

Illiquid tokens, vested allocations, and side pockets are ripe for over-marking. Ask for the last three realized exits compared to their prior marks (that’s real back-testing). - Performance selection bias:

Crypto returns are volatile; managers may showcase a “best slice.” Insist on full-fund, net-of-fee performance with vintage and benchmark context, plus a loss ratio. - Governance gaps:

Who sits on the valuation committee? Who approves exceptions? What changed after the last compliance review? Good answers are calm and specific.

Twelve diligence questions to copy/paste

- Structure: Where is the fund domiciled? Master–feeder? Any side pockets?

- Eligibility & offering path: Who can invest? Is verification required?

- Strategy clarity: What percent is directional vs. market-neutral vs. venture vs. yield?

- Custody: Who is the custodian? MPC or hardware security? Transfer approvals? Whitelists?

- Counterparties: Approved venues list, exposure limits, and off-exchange settlement arrangements.

- DeFi use: Which protocols are in scope? Smart-contract audit policy? Position limits?

- Valuation: Price sources, liquidity discounts, and back-testing process.

- Leverage & liquidity: Gross and net exposure limits; gates, side pockets, and suspension policies.

- Fees & expenses: Management fee, performance fee, watermark/hurdle, and any pass-through expenses (data, borrowing, staking infrastructure).

- Audit & reporting: Auditor name, audit timing, NAV frequency, and sample investor statements.

- Compliance: Who is the CCO? Last review findings and resulting changes.

- Risk events: Describe a major stress or loss and what changed afterward.

How to read a crypto fund PPM (fast)

Focus on five things:

- Investment program: Exactly which assets and protocols are allowed or prohibited.

- Risk disclosures: Clear articulation of custody, counterparty, smart-contract, regulatory, and tax risks—specific to the strategy, not boilerplate.

- Conflicts & allocations: Cross-fund trading, principal transactions, affiliated entities (market makers, validators, OTC desks).

- Liquidity terms: Notice periods, gates, side pockets, suspension triggers, and how in-kind distributions (if any) are handled.

- Governance & controls: Committees (valuation, risk), escalation paths, and independent service providers (administrator, auditor, tax, legal).

If anything is vague, ask for a side letter or written clarification before you wire.

What the next few years likely bring (without the crystal ball)

- Convergence with traditional finance: More institutional custody, independent administrators, and standardized reporting. Expect clearer rules around stablecoins, staking, and tokenized real-world assets.

- Sharper borders between activities: Trading, custody, lending, and market making will be ring-fenced with different licenses and capital requirements. Funds will need to prove they don’t blur those lines.

- Higher bar for disclosures: Marketing claims will require substantiation and context, and regulators will expect performance to be shown net of fees with benchmark references and risk metrics.

- Operational resilience as alpha: In periods of market stress, funds that can withdraw, settle, and re-deploy quickly—without tripping internal risk limits—will outperform. That’s a controls problem as much as a trading one.

Bottom line

Regulation for crypto funds isn’t chaos—it’s an evolving patchwork that increasingly rhymes with traditional asset-management rules, with extra chapters for custody, market structure, and on-chain risk. As an investor, you don’t have to master every acronym. You do need to use regulation as a lens:

- Look for adviser maturity (fiduciary posture, CCO with teeth, real audits).

- Demand custody clarity (who can move assets, how, and under what controls).

- Test counterparty discipline (venue lists, exposure limits, withdrawal tests).

- Insist on valuation evidence (methodology and realized back-tests).

- Read for consistency across the deck, PPM, LPA, and investor letters.

Great crypto funds treat compliance and risk as part of their edge, not an afterthought. If a manager can walk you through safeguards with calm specifics—and show you the math, the memos, and the controls—they’re signaling something deeper than a bull-market story: they’re signaling they can protect your downside while hunting for the upside that brought you here in the first place.

{kind=link}