This Content Is Only For Subscribers

In traditional finance, the phrase “farming” has nothing to do with money. In crypto, though, it became the buzzword of 2020. During what enthusiasts called “DeFi Summer,” thousands of investors rushed into yield farming—a practice that promised double- and even triple-digit annual returns on digital assets.

For many, yield farming looked like free money: put your tokens into a pool, and watch them grow. But behind the catchy term lies a set of strategies that are powerful, complex, and risky. To understand decentralized finance, it helps to grasp how yield farming works—and why it can be both an innovation and a gamble.

The Roots of Yield Farming

Yield farming grew out of the lending and liquidity models of DeFi. Protocols like Compound and Aave let users lend their crypto to earn interest. Others, like Uniswap, let users provide liquidity for trading pairs.

Then came the twist: incentive tokens. In 2020, Compound began distributing its governance token, COMP, to users who borrowed and lent on the platform. This effectively gave users extra rewards on top of interest—and kicked off the yield farming boom.

Soon, nearly every protocol issued its own token to attract users. Investors hopped from one pool to another, “farming” the best yields.

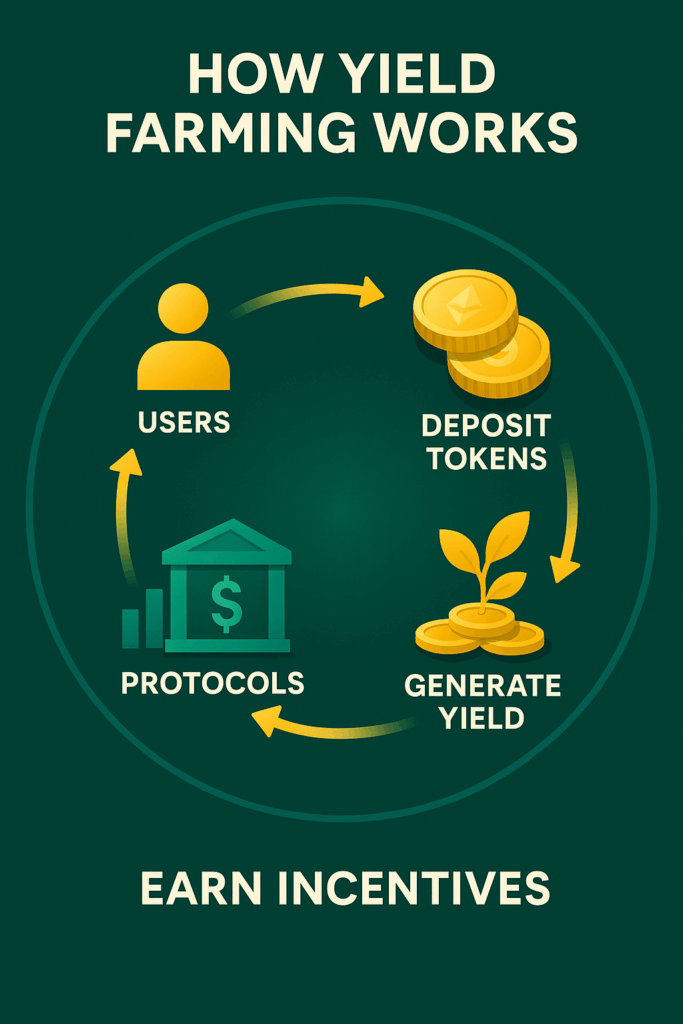

How Yield Farming Works in Practice

At its simplest, yield farming is about putting your crypto to work. Instead of letting tokens sit idle, you deposit them into smart contracts that generate returns.

Here are the main ways it works:

1. Lending and Borrowing

- You deposit crypto (say, ETH or USDC) into a protocol like Aave.

- Borrowers take out loans against collateral.

- The smart contract automatically pays you interest.

- On top of that, you might receive protocol tokens as an incentive.

2. Liquidity Pools (AMMs)

- Platforms like Uniswap and Curve need liquidity so users can trade tokens.

- You provide a pair of tokens (e.g., ETH + USDC) to a pool.

- In return, you earn a share of trading fees.

- Some pools also distribute governance tokens, adding to your yield.

3. Staking

- Some protocols let you stake tokens—locking them up to secure the network.

- In exchange, you receive rewards (sometimes in the same token, sometimes in others).

- Staking can be as simple as one-click deposits or as complex as validator operations.

4. Yield Aggregators

- Platforms like Yearn Finance automatically move funds between pools to maximize returns.

- Instead of monitoring dozens of opportunities, you deposit once, and the aggregator does the farming for you.

The Math Behind the Yields

Yields are usually shown as APY (annual percentage yield). But these rates can be misleading.

- High yields often mean high risk. A pool offering 200% APY is usually compensating for volatility, illiquidity, or low adoption.

- Yields fluctuate constantly. As more people enter a pool, returns often drop.

- Token incentives are temporary. Once rewards end, yields may fall dramatically.

In other words: what looks like free money usually comes with strings attached.

Risks of Yield Farming

Yield farming isn’t a guaranteed win. Here are the biggest dangers:

1. Smart Contract Bugs

If there’s an error in the code, hackers can exploit it and drain funds. Billions of dollars have been lost in DeFi exploits.

2. Impermanent Loss

When you provide liquidity in an AMM, price swings between the two tokens can leave you worse off than simply holding them. This “impermanent loss” can eat into or erase your gains.

3. Volatile Token Rewards

Many protocols reward users in their own tokens. If those tokens crash in price (as often happens), yields shrink or vanish.

4. Leverage and Liquidations

Some farmers borrow against their deposits to farm more aggressively. If collateral values fall, they can be liquidated instantly.

5. Regulatory Uncertainty

Governments are still figuring out how to treat DeFi. New rules could limit access or add compliance requirements.

Case Studies: Lessons from DeFi Summer

- Compound (2020): Launched COMP token incentives, igniting the first wave of yield farming. Early users made enormous returns, but yields fell as more joined.

- SushiSwap (2020): A fork of Uniswap, it attracted users by offering high SUSHI token rewards. The platform survived early controversies and remains a major DEX today.

- Terra’s Anchor Protocol (2021–2022): Promised ~20% APY on stablecoins. When Terra’s UST collapsed in 2022, Anchor collapsed too, showing the risks of unsustainable yields.

Why People Still Farm

Despite risks, yield farming remains popular because:

- It generates passive income. Even modest yields can beat bank interest rates.

- It drives protocol growth. Incentives attract liquidity, which makes DeFi apps usable.

- It’s innovative. Yield farming experiments with models of decentralized incentives that traditional finance can’t easily replicate.

For some, it’s speculation. For others, it’s a way to participate in shaping the future of finance.

Yield Farming vs. Traditional Banking

| Feature | Yield Farming | Traditional Banking |

| Custody | Self-managed via wallets | Bank holds your funds |

| Risk Protection | None (user bears all risks) | Deposit insurance, oversight |

| Returns | Variable, often high | Low but stable |

| Transparency | On-chain, auditable | Opaque balance sheets |

| Accessibility | Open to anyone with internet | Restricted by KYC, geography |

The contrast highlights why yield farming excites some and alarms others.

Lessons for Novice Investors

Even if you never farm yields yourself, there are takeaways:

- High returns usually mean high risk. If a yield seems too good to be true, it probably is.

- Complexity creates pitfalls. The more steps involved, the greater the chance of mistakes or losses.

- Diversify. Don’t put all funds in one pool or protocol.

- Know what you’re farming. Understand the risks of both the base assets and the reward tokens.

- Stay cautious with leverage. Farming with borrowed funds magnifies both gains and losses.

Final Thoughts

Yield farming is one of the most creative—and controversial—developments in decentralized finance. It combines lending, trading, and incentives in ways traditional banks can’t. At its best, it rewards early adopters and fuels innovation. At its worst, it can trap newcomers chasing unrealistic returns.

For novice investors, the key isn’t to dive into the latest pool, but to understand what yield farming reveals: in DeFi, incentives drive behavior, and risk is never far from reward.

{kind=link}