This Content Is Only For Subscribers

If you’ve ever felt locked out of contributing to a Roth IRA because of income limits, or if you’ve wondered how to shift your retirement savings into more tax-friendly territory, the answer may be a Roth IRA conversion.

Conversions let you move money from a pre-tax account—like a traditional IRA or a 401(k)—into a Roth IRA. You’ll pay taxes today, but once inside the Roth, that money grows tax-free and can be withdrawn tax-free in retirement. Done thoughtfully, conversions can save you tens of thousands in taxes over a lifetime.

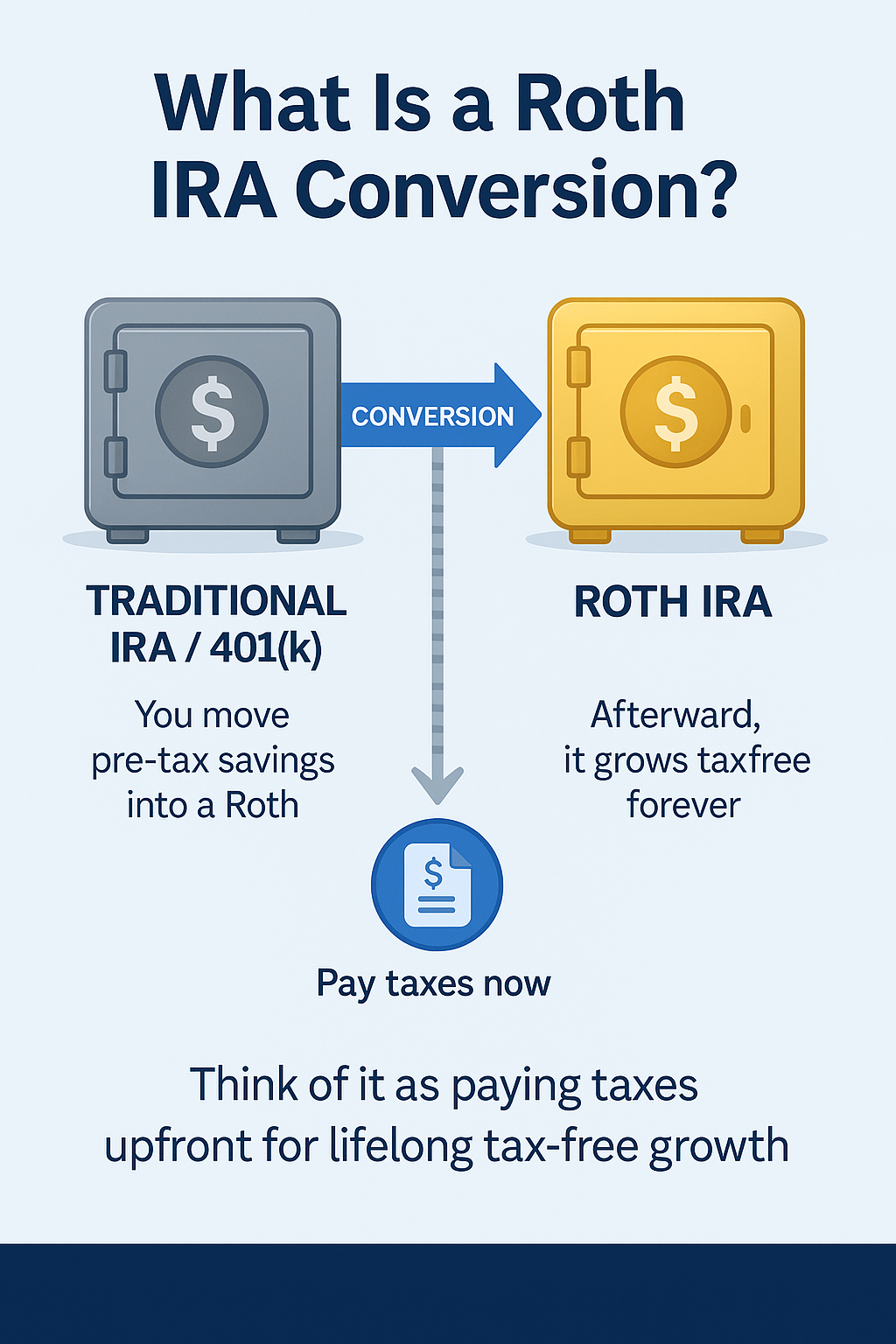

What Is a Roth IRA Conversion?

A Roth IRA conversion is the process of taking money from a pre-tax retirement account and moving it into a Roth IRA.

- Source accounts: Traditional IRA, SEP IRA, SIMPLE IRA (after two years), and eligible 401(k)/403(b) balances.

- Tax impact: Any pre-tax dollars you convert are added to your taxable income for the year.

- Result: Once in the Roth, the converted money grows tax-free and can eventually be withdrawn tax-free.

Think of it as paying your tax bill early in exchange for permanent tax freedom later.

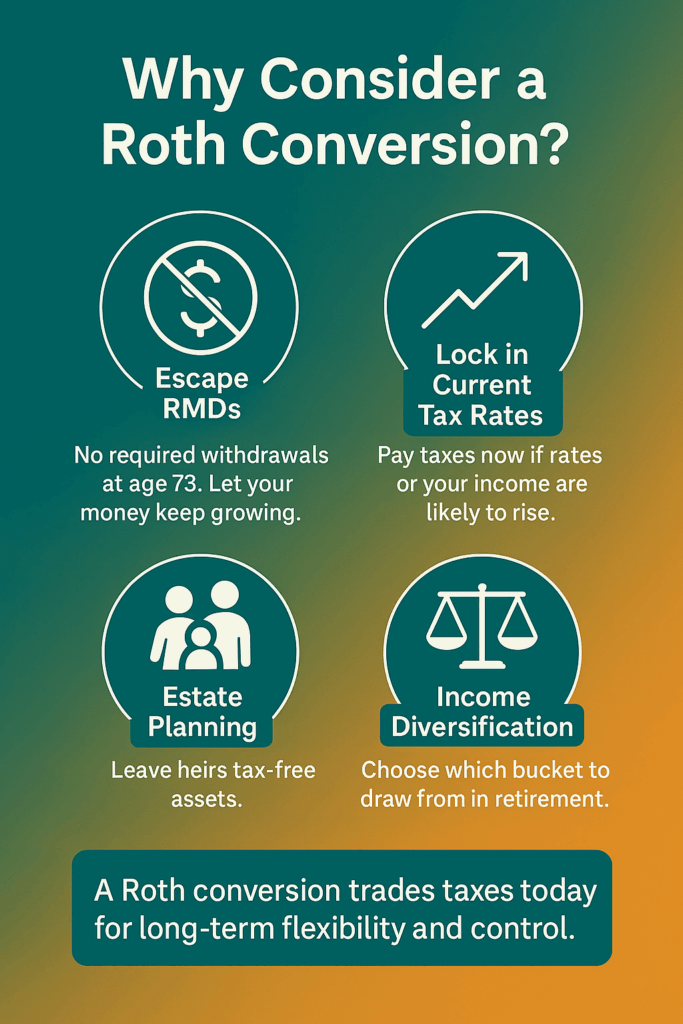

Why Consider a Conversion?

- Escape RMDs

Traditional IRAs and 401(k)s force you to take required minimum distributions starting at age 73. Roth IRAs do not, allowing your money to grow longer or be left to heirs. - Lock in Current Tax Rates

If you expect tax rates to rise—or your personal income to rise—a conversion now may be cheaper than paying taxes later. - Estate Planning

Leaving heirs a Roth IRA means they inherit a tax-free account. They’ll still face distribution rules, but withdrawals won’t create taxable income. - Income Diversification in Retirement

Having both pre-tax and Roth accounts lets you decide which bucket to pull from each year, giving you more control over taxable income and Medicare premiums.

When Conversions Make Sense

Early Retirement “Gap Years”

Between retirement and age 73 (when RMDs begin), many retirees have lower taxable income. These years can be ideal for strategic conversions.

Market Downturns

If your portfolio value falls, converting at a lower account value means a smaller tax bill. When the market recovers, that growth happens inside the Roth tax-free.

Years with Low or No Income

Sabbaticals, career breaks, or a temporary dip in business income can be great opportunities to convert while staying in a low tax bracket.

Before Big Tax Law Changes

If you believe future tax rates will be higher—whether due to expiring tax cuts or fiscal policy—it may make sense to convert now.

How to Do a Roth Conversion

- Open a Roth IRA

If you don’t already have one, open a Roth IRA at a brokerage or bank. - Choose the Amount to Convert

Decide how much to move from your traditional account. This amount is treated as taxable income. - Pay Taxes

Set aside cash outside the account to pay the conversion taxes. Using IRA funds to pay the tax reduces the long-term benefit. - Move the Funds

You can transfer directly between custodians or do a rollover. A direct transfer avoids the risk of missing deadlines. - Track the Five-Year Rule

Each conversion has its own five-year clock for the 10% penalty if you’re under 59½.

Managing the Tax Bill

The biggest hurdle to Roth conversions is the tax bill. Strategies to manage it include:

- Partial Conversions: Spread conversions across several years to avoid jumping tax brackets.

- Bracket Filling: Convert just enough to top off your current bracket (e.g., to the top of the 22% bracket).

- Coordinate With Deductions: If you have large deductions in a given year (medical expenses, charitable giving), convert more that year.

Example: Bracket Filling

Karen, age 60, has $50,000 of taxable income and is in the 12% bracket (up to ~$94,300 for married couples in 2024). She could convert ~$40,000 from her traditional IRA to a Roth and still stay in the 12% bracket, paying relatively low taxes on that amount.

Pitfalls to Avoid

- Converting Too Much at Once

A big conversion can push you into higher tax brackets, costing more than the long-term benefit. - Forgetting the Pro-Rata Rule

If you have both pre-tax and after-tax dollars in IRAs, the IRS requires conversions to include a proportional share of each. This can complicate “backdoor” strategies. - Not Filing Form 8606

This IRS form reports non-deductible contributions and conversions. Missing it can lead to double taxation. - Paying Taxes from the IRA

Using converted dollars to cover the tax reduces your Roth balance and potential growth.

Advanced Strategy: The Roth Conversion Ladder

Early retirees sometimes use a Roth conversion ladder:

- Convert a set amount each year.

- Wait five years for each conversion to “season.”

- Withdraw converted dollars penalty-free to cover living expenses before age 59½.

This strategy requires careful planning but can bridge the gap between early retirement and Social Security.

Who Should Avoid Conversions?

- Those Already in High Brackets: If you’re in the 35–37% bracket now and expect lower income later, a conversion could cost more than it saves.

- Those Without Cash to Pay Taxes: Using IRA funds to pay the tax reduces the benefit.

- Short-Term Investors: If you’ll need the money soon, paying taxes now may not be worth it.

Final Thoughts

A Roth IRA conversion can be one of the most powerful retirement-planning tools available—but only if done thoughtfully. The decision comes down to a trade-off: paying taxes today for tax freedom tomorrow.

By choosing the right timing, spreading conversions strategically, and keeping an eye on your tax bracket, you can make conversions work for you. For some, they’re a way to bypass income limits; for others, they’re a smart play for estate planning. Either way, conversions give you control over your retirement tax picture—and that control can make all the difference.

{kind=link}