This Content Is Only For Subscribers

Private equity often conjures images of billion-dollar buyouts, complex financial engineering, and boardroom battles that reshape entire industries. For many novice investors, the world of private equity feels like a closed club—exclusive, mysterious, and sometimes intimidating. Yet beneath the jargon and headlines lie fascinating stories, and more importantly, lessons that anyone can learn about business, risk, and value creation.

In this article, we’ll explore some of the most iconic private equity deals of the past four decades. These transactions are memorable not only because of their size, but also because of what they reveal about how private equity firms operate—the strategies that succeed, the pitfalls that destroy value, and the lasting impact on companies and economies.

Private Equity 101: Setting the Stage

Before diving into case studies, let’s ground ourselves in the basics.

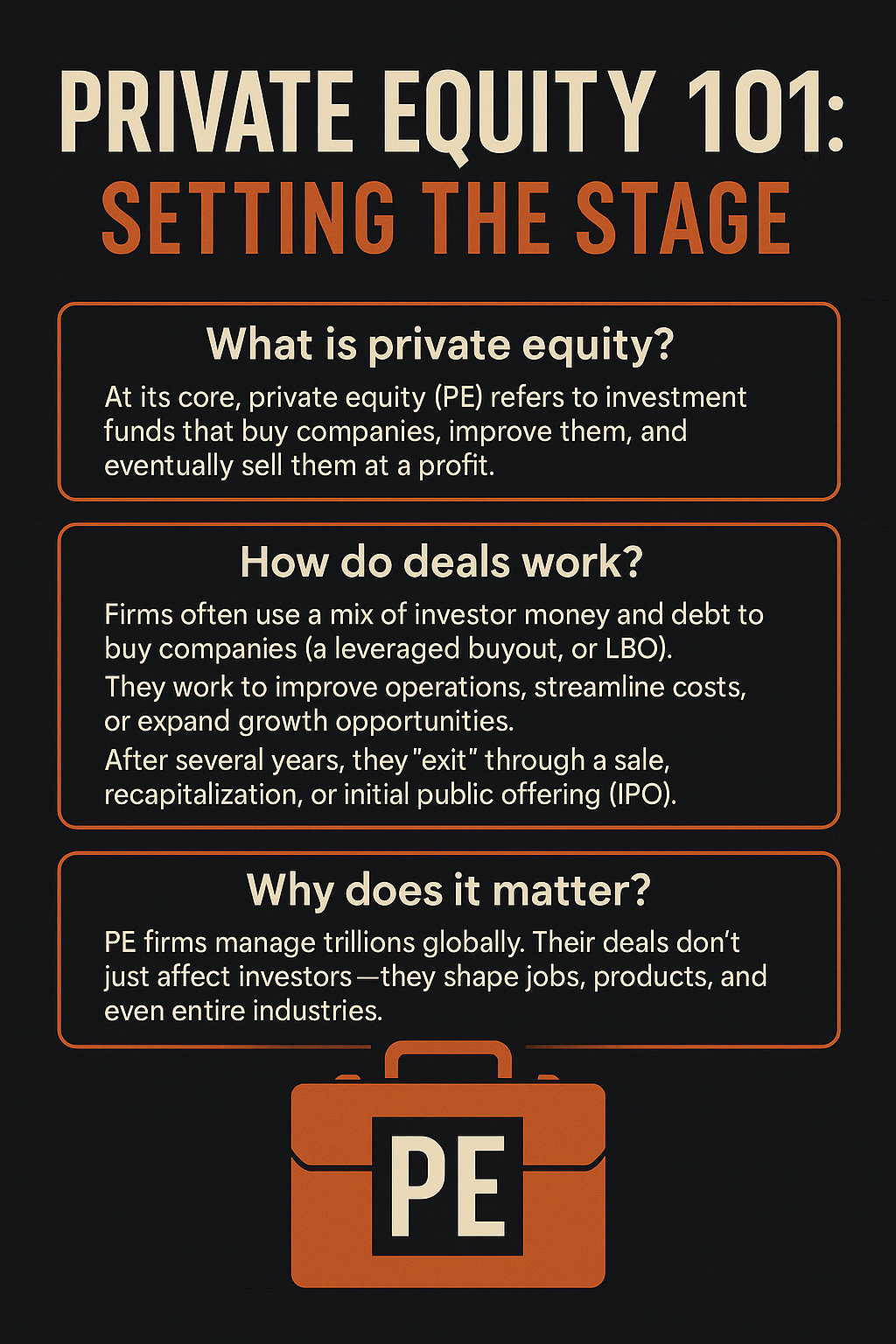

What is private equity?

At its core, private equity (PE) refers to investment funds that buy companies, improve them, and eventually sell them at a profit. The firms raise money from institutional investors—pension funds, endowments, wealthy families—and use that capital to acquire businesses.

How do deals work?

- Firms often use a mix of investor money and debt to buy companies (a leveraged buyout, or LBO).

- They work to improve operations, streamline costs, or expand growth opportunities.

- After several years, they “exit” through a sale, recapitalization, or initial public offering (IPO).

Why does it matter?

PE firms manage trillions globally. Their deals don’t just affect investors—they shape jobs, products, and even entire industries.

Case Study #1: KKR and the RJR Nabisco Buyout

When people think of private equity legends, one deal always comes to mind: the 1988 leveraged buyout of RJR Nabisco by Kohlberg Kravis Roberts (KKR). At $25 billion, it was the largest buyout in history at the time, and it remains a defining example of both the power and controversy of private equity.

The setup:

RJR Nabisco was a giant conglomerate, best known for tobacco and food brands like Oreo and Ritz. Its CEO, F. Ross Johnson, felt undervalued by the stock market and launched a management-led buyout attempt.

The bidding war:

Once Johnson’s bid went public, private equity firms smelled opportunity. KKR, already famous for pioneering leveraged buyouts, jumped in. A fierce bidding war ensued, with competing offers escalating the price.

The outcome:

KKR ultimately won with a $25 billion offer. The deal became legendary after being chronicled in the book Barbarians at the Gate. While it cemented KKR’s reputation, the heavy debt burden strained RJR Nabisco, leading to years of financial stress.

Lessons:

- Leverage cuts both ways. Debt can magnify returns but can also cripple a company.

- Bidding wars can destroy value. Overpaying in the heat of competition often hurts long-term results.

- Narratives matter. The RJR Nabisco saga shaped how the public views private equity—ruthless, bold, but also risky.

Case Study #2: Blackstone and Hilton Hotels

Fast forward to 2007, on the eve of the financial crisis. Blackstone Group made headlines by acquiring Hilton Hotels for $26 billion, one of the largest hotel deals ever. Many analysts criticized the move, calling it reckless given the looming downturn. But what followed turned out to be one of the most successful private equity deals in history.

The setup:

Blackstone, founded in 1985, had grown into a PE powerhouse. By 2007, it saw Hilton as a global brand with untapped potential in international markets.

The challenge:

Months after the acquisition, the 2008 global financial crisis hit. Hotel demand plunged, financing dried up, and Blackstone’s debt-heavy purchase looked like a disaster.

The turnaround:

Instead of panicking, Blackstone worked with Hilton’s management to restructure operations, expand franchising, and reposition the brand. They focused on long-term growth rather than short-term panic.

The outcome:

In 2013, Hilton went public in what was then the largest-ever hotel IPO. Blackstone ultimately made a profit of around $14 billion on the deal, one of the biggest windfalls in private equity history.

Lessons:

- Patience matters. Weathering downturns can pay off if the fundamentals are strong.

- Operational improvement drives value. Blackstone’s focus wasn’t just financial—it was about making Hilton better.

- Timing isn’t everything. Even a “badly timed” deal can succeed with discipline and strategy.

Case Study #3: Bain Capital and Toys “R” Us

Not every private equity story ends well. The tale of Toys “R” Us highlights the risks of leverage, shifting markets, and slow adaptation.

The setup:

In 2005, Bain Capital, KKR, and Vornado Realty Trust teamed up to buy Toys “R” Us for $6.6 billion. At the time, the iconic toy retailer faced challenges from Walmart, Target, and online retailers, but investors believed the brand still had magic.

The challenge:

The buyout saddled Toys “R” Us with more than $5 billion in debt. As e-commerce boomed, the company struggled to invest in technology and customer experience. The debt burden limited flexibility.

The outcome:

By 2017, Toys “R” Us filed for bankruptcy, closing hundreds of stores and laying off tens of thousands of workers. While other factors contributed—like changing consumer habits and online competition—the heavy debt from the buyout was a major factor.

Lessons:

- Debt can limit adaptation. Companies need room to invest and evolve.

- Industry trends matter. Even the best-known brands can falter if they don’t keep up with consumers.

- PE reputations suffer in failures. The Toys “R” Us case fueled public skepticism about private equity.

Case Study #4: Silver Lake and Dell Technologies

Not all deals are household names, but some reshape industries quietly. In 2013, Silver Lake Partners and Michael Dell took Dell private in a $24 billion buyout. The goal was to give Dell breathing room to reinvent itself away from Wall Street’s quarterly pressures.

The setup:

Dell, once the world’s leading PC maker, was losing ground to smartphones, tablets, and cloud computing. Michael Dell believed the company could pivot to enterprise technology but needed privacy to execute the turnaround.

The strategy:

Going private allowed Dell to invest heavily in servers, storage, and IT services without scrutiny from public shareholders. Silver Lake provided the financial backing to make it possible.

The outcome:

By 2018, Dell returned to public markets after acquiring EMC, a giant in data storage. The deal created one of the largest tech companies in the world, with a strong position in enterprise solutions.

Lessons:

- Going private can create breathing room. Companies can transform outside the spotlight.

- Partnership matters. The alignment between Michael Dell and Silver Lake was key.

- Tech pivots require patience. Reinvention is rarely immediate, but private equity can provide the runway.

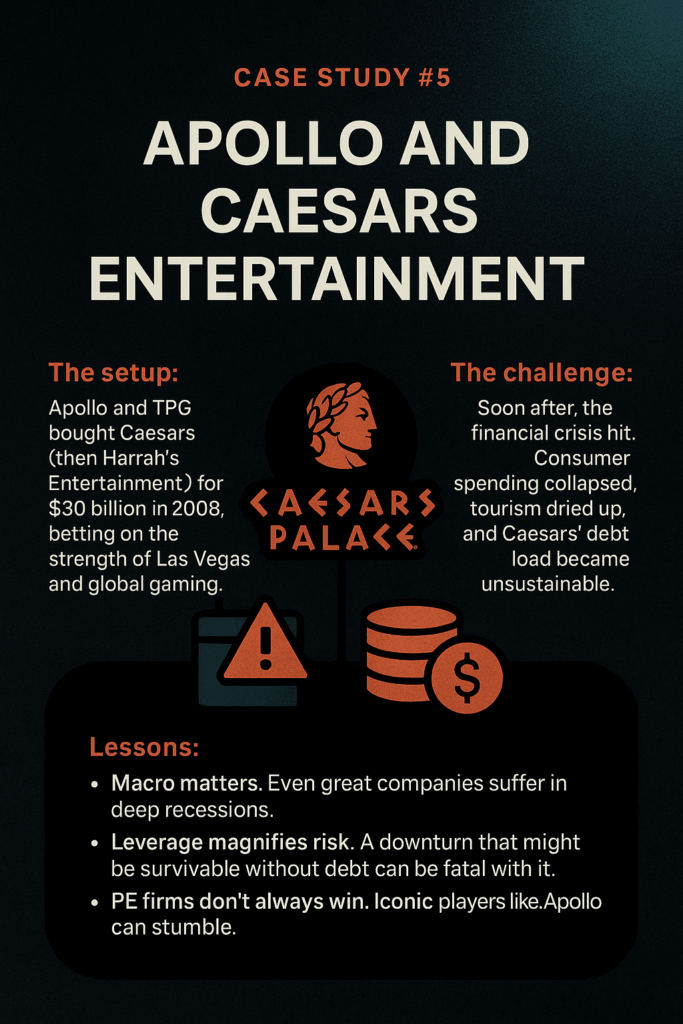

Case Study #5: Apollo and Caesars Entertainment

Sometimes private equity bets look promising but unravel spectacularly. Apollo Global Management’s acquisition of Caesars Entertainment in 2008 shows how external shocks and high leverage can destroy even well-laid plans.

The setup:

Apollo and TPG bought Caesars (then Harrah’s Entertainment) for $30 billion in 2008, betting on the strength of Las Vegas and global gaming.

The challenge:

Soon after, the financial crisis hit. Consumer spending collapsed, tourism dried up, and Caesars’ debt load became unsustainable.

The outcome:

Caesars filed for bankruptcy in 2015, wiping out billions in value. The deal became a cautionary tale of what happens when debt and timing collide.

Lessons:

- Macro matters. Even great companies suffer in deep recessions.

- Leverage magnifies risk. A downturn that might be survivable without debt can be fatal with it.

- PE firms don’t always win. Iconic players like Apollo can stumble.

Case Study #6: The TXU Energy Buyout

Another cautionary tale unfolded in 2007 when KKR, Texas Pacific Group (TPG), and Goldman Sachs led a $45 billion buyout of TXU, the largest utility in Texas. At the time, it was the biggest leveraged buyout ever attempted.

The setup:

The firms bet on rising natural gas prices, which would make TXU’s coal-fired power plants more profitable.

The challenge:

Instead, natural gas prices collapsed, renewable energy grew more competitive, and regulatory pressures mounted. The company’s debt load—over $40 billion—became unbearable.

The outcome:

By 2014, TXU (renamed Energy Future Holdings) filed for one of the largest bankruptcies in U.S. history. The deal is often cited as an example of private equity overreach.

Lessons:

- Commodity bets are risky. Macro shifts in energy markets can upend even the best-laid plans.

- Size doesn’t equal safety. Being the biggest buyout ever didn’t protect TXU.

- Assumptions matter. A deal based on a single market forecast can be devastating when that forecast fails.

Case Study #7: Blackstone and Invitation Homes

Private equity isn’t just about corporate boardrooms—it can touch people’s daily lives. After the 2008 housing crisis, Blackstone became the largest owner of single-family rental homes in the U.S. through its subsidiary Invitation Homes.

The setup:

Millions of homes went into foreclosure during the crisis. Blackstone saw an opportunity to buy distressed properties at deep discounts.

The strategy:

The firm acquired tens of thousands of homes, renovated them, and rented them out, effectively institutionalizing single-family rentals.

The outcome:

By 2017, Invitation Homes went public in a $1.5 billion IPO. The business gave Blackstone strong returns, though it also sparked debates about Wall Street’s role in the housing market.

Lessons:

- Crisis creates opportunity. Bold moves in downturns can pay off.

- Social impact matters. Deals that affect everyday people attract scrutiny.

- Innovation in asset classes. PE can reshape entire markets, not just companies.

Broader Themes Across the Deals

Looking across these iconic case studies, certain themes stand out:

- Leverage is a double-edged sword. It can create value when growth materializes but destroys flexibility when conditions sour.

- Operational improvement is key. The best deals (like Hilton) succeed because PE firms add value beyond financial engineering.

- Industry trends matter. No amount of structuring can save a company that fails to adapt to shifting markets.

- Partnership and leadership drive outcomes. When management and investors are aligned, companies have a better chance to thrive.

- Timing and macro conditions play a role. Even smart deals can collapse if the economy turns.

What Novice Investors Can Take Away

You may not be investing in billion-dollar buyouts, but the principles still apply:

- Diversify your risks. Don’t let one investment dominate your portfolio. Example: Instead of putting 80% of your savings in one stock, spread it across funds or sectors.

- Think long term. Like Blackstone with Hilton, patience can turn a near-disaster into a triumph. For individuals, this might mean sticking with your retirement contributions through downturns.

- Avoid overpaying. Excitement can lead to inflated prices. This applies whether you’re buying a stock at record highs or bidding on a house in a hot market.

- Watch the big picture. Economic cycles, interest rates, and industry trends affect all investments, not just private equity. For example, rising rates can weigh on housing and tech stocks.

- Look for real improvement. Whether in your own finances or in stocks you buy, seek situations where value can be added—not just shuffled around.

These stories also highlight a subtler point: investing is as much about avoiding mistakes as chasing big wins. Many failed buyouts (Toys “R” Us, TXU, Caesars) could have been avoided by respecting debt levels, questioning assumptions, and not ignoring big industry shifts.

Closing Thoughts

Private equity may seem like a world apart, filled with billion-dollar deals and complex strategies. But at its heart, it’s about something simple: buying businesses, improving them, and selling them for more.

The case studies of RJR Nabisco, Hilton, Toys “R” Us, Dell, Caesars, TXU, and Invitation Homes show the highs and lows of that journey. They reveal the power of bold bets, the dangers of over-leverage, and the importance of timing, discipline, and vision.

For novice investors, these stories offer more than entertainment. They remind us that the principles of success in investing—discipline, patience, and understanding risk—are universal, whether you’re running a household budget or a multibillion-dollar fund.

{kind=link}