This Content Is Only For Subscribers

For anyone saving in a Traditional IRA, understanding Required Minimum Distributions (RMDs) is essential. RMDs are the minimum amounts you must withdraw from your Traditional IRA each year once you reach a certain age. Missing these withdrawals can result in significant tax penalties, so knowing the rules helps you plan for both taxes and retirement income.

What Are RMDs?

RMDs are government-mandated withdrawals from tax-deferred retirement accounts like Traditional IRAs, 401(k)s, and certain other qualified plans. The IRS requires them to ensure that retirement accounts are eventually taxed. Essentially, the government allows you to grow your investments tax-deferred for decades, but eventually you must pay income tax on the money you’ve saved.

Key points:

- Only Traditional IRAs and other tax-deferred accounts are subject to RMDs.

- Roth IRAs do not require RMDs during the owner’s lifetime, which makes them attractive for estate planning.

When Do RMDs Begin?

Recent changes in U.S. law have updated the starting age for RMDs:

- Age 73: Most individuals must take their first RMD.

- Age 75: Future cohorts may see the starting age shift to 75, depending on the law in effect when they reach retirement age.

- First RMD deadline: April 1 of the year following the year you turn 73.

- Subsequent RMDs: Must be taken by December 31 each year.

For example, if you turn 73 in 2025, your first RMD must be taken by April 1, 2026. Every year after that, you must take your RMD by December 31.

How RMDs Are Calculated

The amount you must withdraw is calculated using two factors:

- Your account balance at the end of the previous year

- Your life expectancy factor, provided by IRS tables

The IRS provides Uniform Lifetime Tables that assign a life expectancy factor based on age. The RMD is calculated as:

RMD= Life expectancy factor/Previous year-end IRA balance

Example:

- Jane has a Traditional IRA balance of $500,000 at the end of 2024.

- At age 73, the IRS life expectancy factor is 27.4.

- Her RMD for 2025 is:

$500,000÷27.4≈$18,248

Jane must withdraw at least $18,248 from her IRA in 2025 to satisfy RMD rules.

Special Considerations for Spouses

- If your spouse is more than 10 years younger, you may use the Joint Life and Last Survivor Expectancy Table, which results in a slightly lower RMD.

- This can help reduce taxes and allow your account to grow longer.

Taxes on RMDs

RMDs are taxed as ordinary income in the year you take them. For example:

- If your RMD is $18,248 and you are in the 22% federal tax bracket, you would owe approximately $4,015 in federal income tax on that withdrawal.

State taxes may also apply depending on where you live.

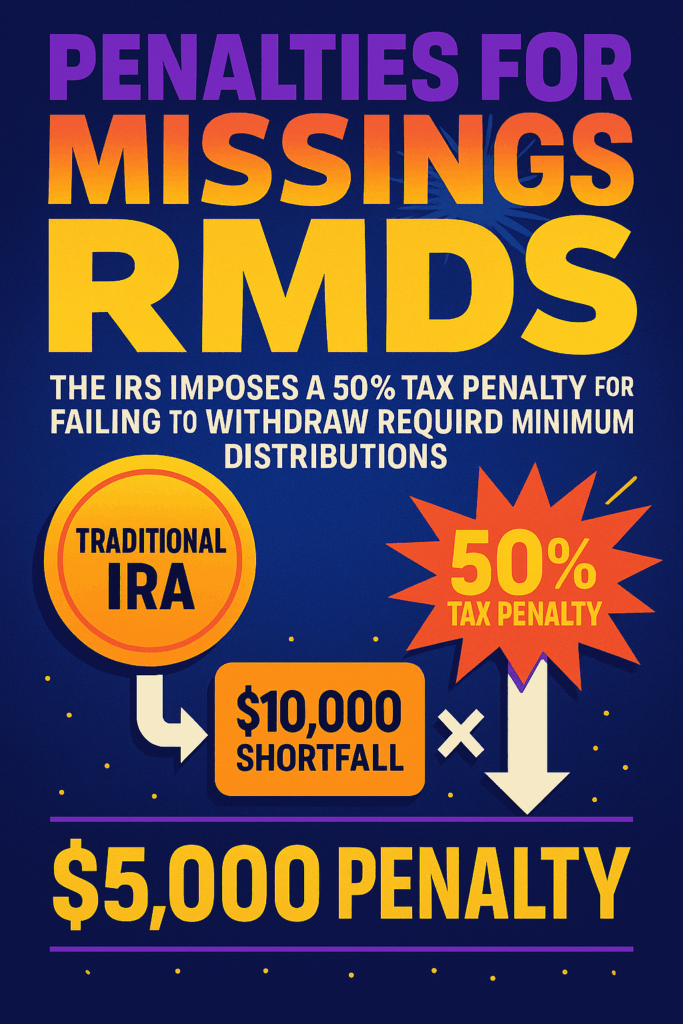

Penalties for Missing RMDs

Failing to take your RMD, or withdrawing less than the required amount, triggers a 50% excise tax on the amount that should have been withdrawn.

Example:

- If Jane only withdraws $10,000 instead of the required $18,248, she would owe 50% of the shortfall:

50%×($18,248−$10,000)=50%×$8,248=$4,124

This penalty is steep, making careful planning essential.

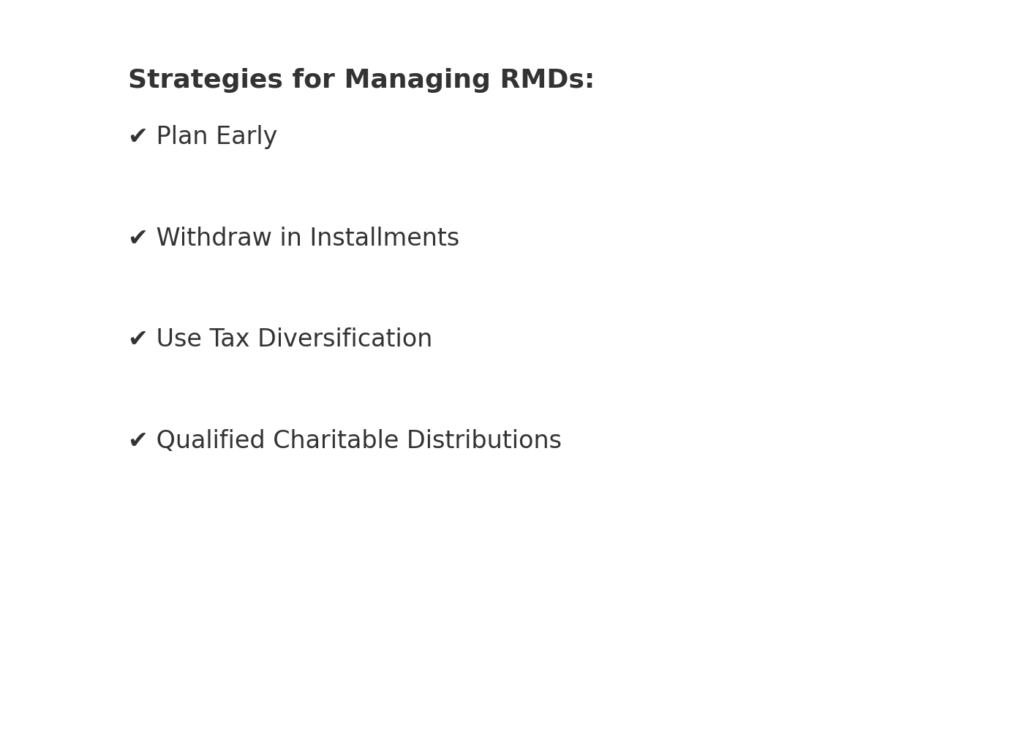

Strategies for Managing RMDs

1. Plan Withdrawals in Advance

Knowing your RMD amounts helps avoid last-minute stress and taxes. Use your IRA statements and IRS life expectancy tables to calculate each year’s required withdrawal early.

2. Withdraw in Installments

You don’t have to take your full RMD at once. Many retirees spread withdrawals over the year, which can help with cash flow and reduce the impact on tax brackets.

3. Consider Tax Diversification

- Withdraw from taxable accounts first if you want to let your IRA continue growing.

- Combine Traditional IRA withdrawals with Roth conversions or taxable account withdrawals to manage annual taxes strategically.

4. Use RMDs for Charitable Giving

- Individuals 70½ or older can make Qualified Charitable Distributions (QCDs) directly from their IRA, which counts toward the RMD but isn’t included in taxable income.

- This can reduce taxes while supporting charitable causes.

Planning for RMDs with Multiple Accounts

Many retirees have multiple Traditional IRAs or 401(k)s. The IRS allows aggregating RMDs across IRAs, meaning you can calculate the total required withdrawal and take it from any combination of your accounts.

- Example:

- IRA 1 RMD = $10,000

- IRA 2 RMD = $8,000

- Total RMD = $18,000 → you can withdraw all $18,000 from IRA 2 alone if you prefer.

This flexibility allows better management of investments and cash flow.

Real-Life Scenario

Mark, age 73, has:

- Traditional IRA 1: $300,000

- Traditional IRA 2: $200,000

Using the IRS table, his total RMD = $500,000 ÷ 27.4 = $18,248

Mark decides to withdraw the entire $18,248 from IRA 2. This satisfies the IRS requirement without touching IRA 1, allowing that account to continue growing.

Common Misconceptions About RMDs

- “Roth IRAs require RMDs.”

❌ False. Roth IRAs don’t require withdrawals during the owner’s lifetime. - “I can wait until April 15 to withdraw my RMD each year.”

⚠️ Not entirely. While the first RMD can be delayed to April 1 of the year following the year you turn 73, subsequent RMDs are due by December 31 of each year. - “I can avoid RMDs by keeping money invested.”

❌ False. Taxes and penalties apply if RMDs are not taken.

Planning Tips for Novice Investors

- Track your RMDs using IRS tables or your brokerage’s RMD calculator.

- Withdraw early in the year to ensure you don’t forget.

- Consider consulting a tax professional if you have multiple IRAs or other retirement accounts.

- Explore QCDs if charitable giving is part of your financial plan.

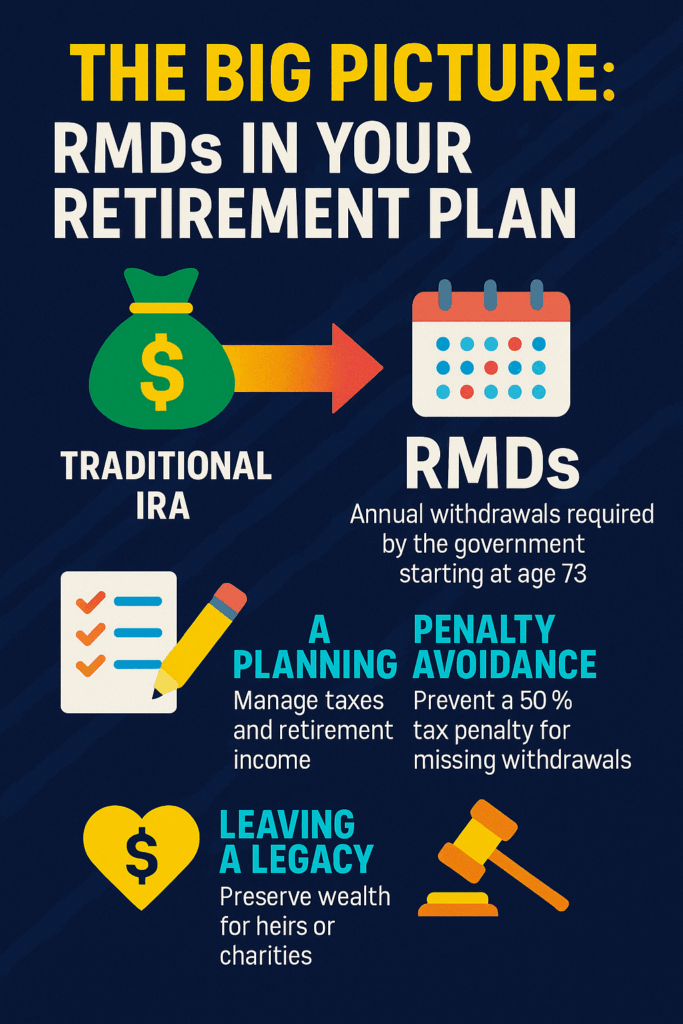

Why RMDs Matter

RMDs are not just a tax requirement—they are a retirement planning tool. By planning withdrawals strategically, you can:

- Avoid steep penalties

- Manage tax brackets in retirement

- Preserve wealth for heirs or charitable causes

Final Thoughts

Required Minimum Distributions are an essential part of managing Traditional IRAs. While the rules can feel complex, understanding when to withdraw, how much to withdraw, and how RMDs are taxed ensures your retirement savings are used efficiently and effectively.

By planning ahead, leveraging aggregation strategies, and considering charitable options, you can meet IRS requirements while maximizing your long-term financial goals. For novice investors, taking the time to understand RMDs now will pay dividends in retirement peace of mind.

{kind=link}