This Content Is Only For Subscribers

If you scan the portfolios of large pensions, endowments, and insurers today, one thing stands out: allocations to private credit keep rising. A decade ago, private credit was niche. Today, it is a core part of many institutional portfolios, often rivaling allocations to hedge funds or traditional fixed income.

So why the shift? The answer lies in a mix of economics, market structure, and strategy. Understanding these drivers helps investors—both big and small—grasp why this once-obscure asset class has become mainstream.

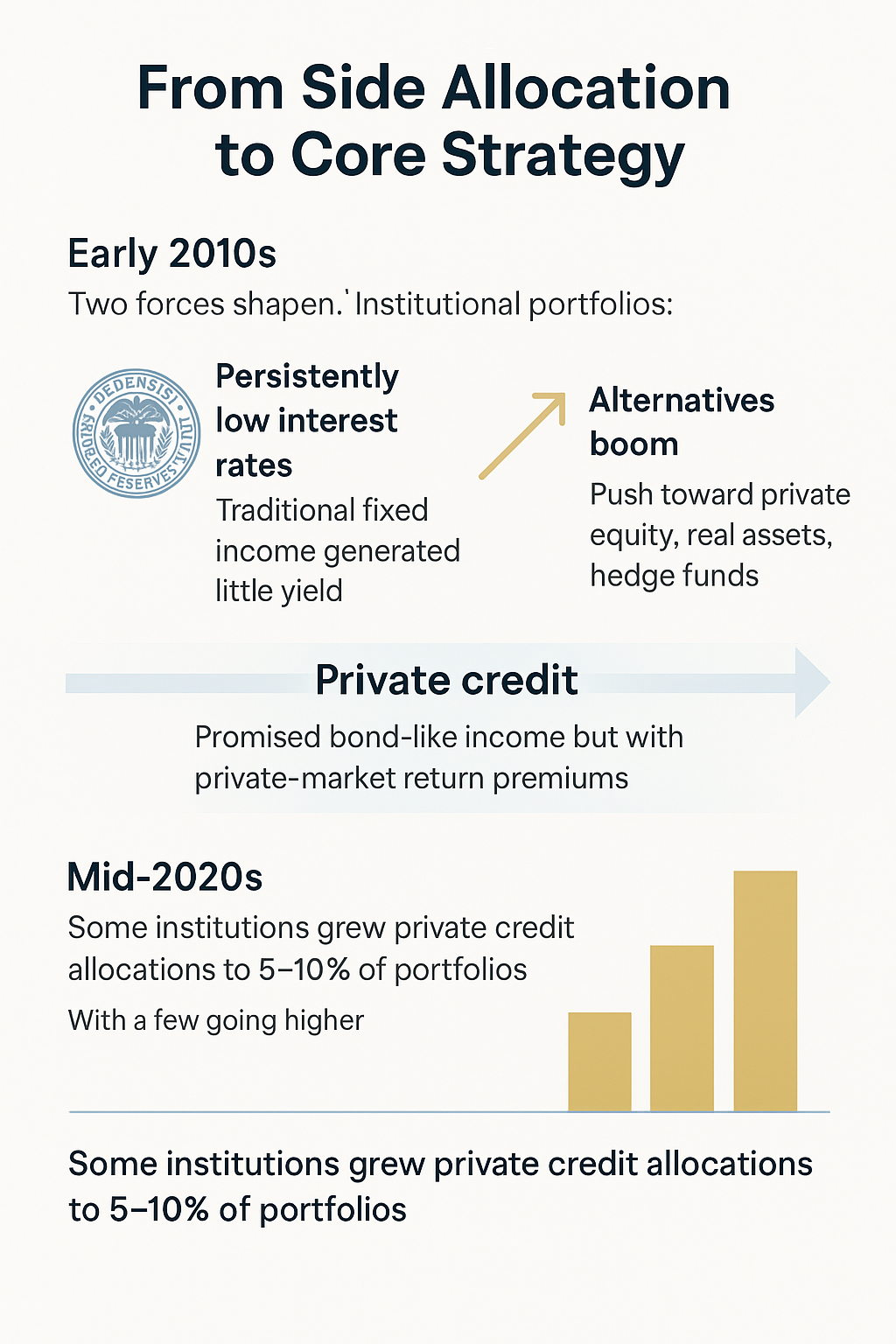

From Side Allocation to Core Strategy

In the early 2010s, institutional portfolios were shaped by two forces:

- Persistently low interest rates meant traditional fixed income generated little yield.

- Alternatives boom—pioneered by the “endowment model”—pushed investors toward private equity, real assets, and hedge funds.

Private credit fit neatly between those worlds: it promised bond-like income but with private-market return premiums.

By the mid-2020s, some institutions had grown allocations to 5–10% of total portfolios, with a few going higher. For pensions and insurers managing hundreds of billions, that translates into tens of billions directed at private credit funds.

The Core Drivers Behind Institutional Allocations

1) Yield Enhancement

The most straightforward driver is yield.

- Public bonds: Investment-grade corporates typically yield a few percentage points above Treasuries.

- Private credit: Direct loans to mid-market borrowers may yield 6–12%, sometimes more in distressed or specialty finance.

For institutions under pressure to meet fixed obligations—pension payments, insurance liabilities—those extra percentage points are valuable.

Investor takeaway: Yield alone doesn’t explain everything, but it’s the primary entry point.

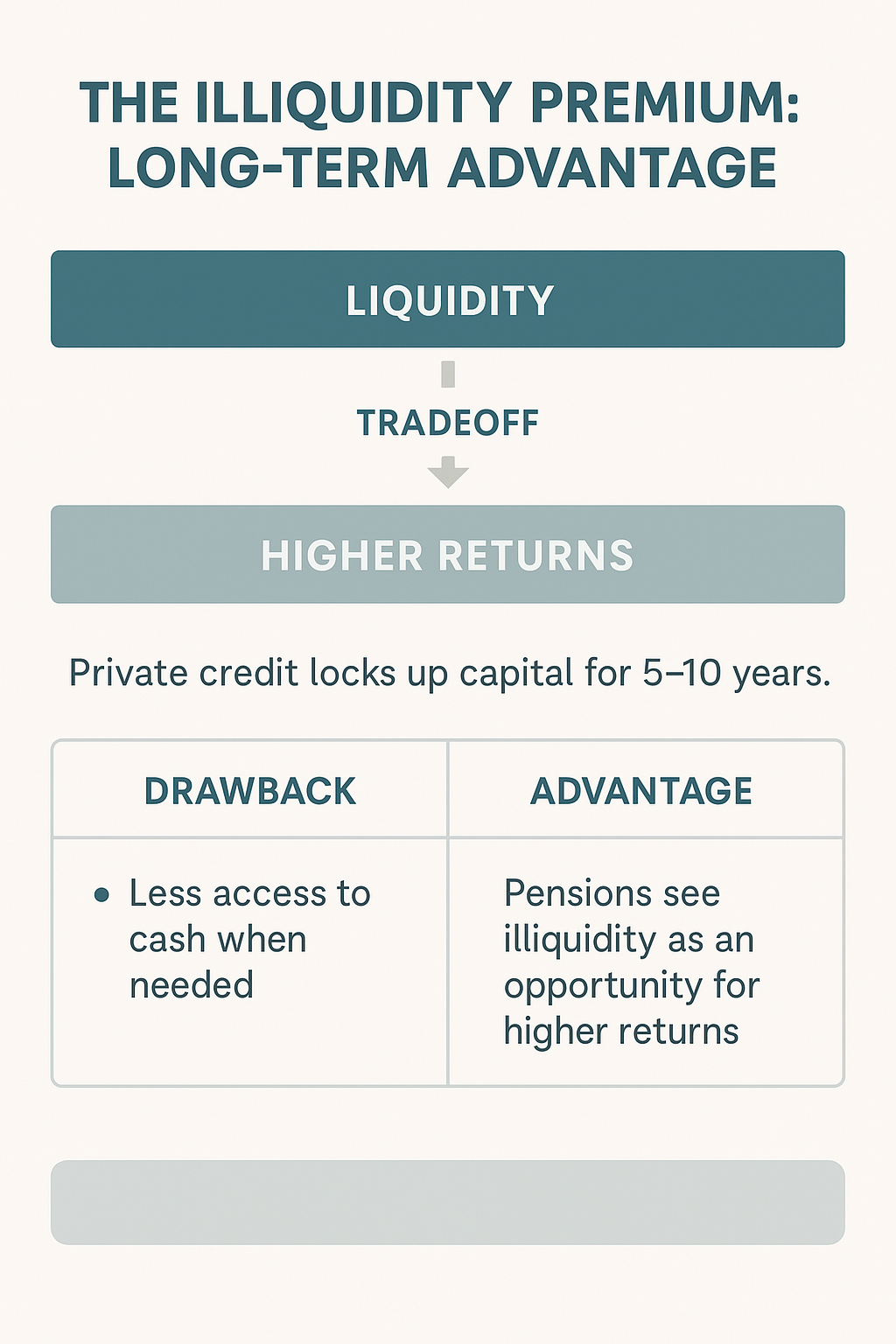

2) Illiquidity Premium

Private credit locks up capital. Funds are usually closed-end, with 5–10 year lives. That illiquidity is a drawback for some, but institutions with long-term horizons can view it differently: as an illiquidity premium they are compensated for.

Pensions and endowments don’t need to mark portfolios to market daily. They can sacrifice liquidity for higher returns. In fact, many see this as a natural portfolio advantage over retail investors who demand liquidity.

3) Diversification of Income Sources

Public credit markets tend to move together, especially during stress. Private credit adds a new set of exposures: bespoke loans to mid-market companies, asset-backed specialty finance, NAV loans. These don’t always move in sync with Treasuries or high-yield bonds.

For institutions seeking stable, less correlated cash flows, private credit provides diversification.

4) Floating-Rate Protection

Most direct loans are floating-rate. When central banks raise rates, coupon income rises.

In the 2022–2023 hiking cycle, this was a gift for private credit managers. Yields on direct loans jumped into double digits, giving investors an income boost while many other assets struggled.

Caveat: Higher rates can stress borrowers—but on a portfolio level, floating-rate coupons have made private credit an effective inflation hedge.

5) Bank Retrenchment and Structural Demand

Since 2008, banks have pulled back from leveraged lending due to regulatory capital rules. That left a financing gap, particularly for mid-market companies and private equity buyouts.

Private credit managers filled the void. Institutions recognized this wasn’t a temporary shift but a structural change in how companies borrow. Allocating to private credit wasn’t just a yield play—it was a way to tap into a growing, durable financing channel.

6) Alignment With Private Equity

Many institutions already have large private equity allocations. Private credit is a natural complement:

- Sponsors rely on private credit for buyout financing.

- Co-investment opportunities allow institutions to access both the equity and the debt side of a deal.

- Cash flows from private credit can help fund capital calls for private equity commitments.

In short, private credit fits neatly into the private-markets ecosystem institutions already embrace.

7) Innovation and Access Vehicles

Allocations also rose because the product menu expanded:

- Mega-funds handle multi-billion-dollar commitments from the largest pensions.

- Specialty funds target niches (litigation finance, royalties, trade finance).

- Evergreen vehicles offer periodic liquidity, attractive to insurers and wealth platforms.

Institutions no longer had to shoehorn themselves into generic direct lending—they could tailor exposure.

The Benefits They See

Institutions cite several benefits when justifying their allocations:

- Attractive risk-adjusted returns compared to public credit.

- Income generation to match liabilities.

- Diversification versus equity-dominated alternatives.

- Control and governance—direct lender relationships can provide more influence than owning public bonds.

- Lower volatility—valuations are marked quarterly, dampening mark-to-market swings.

The Concerns They Weigh

Allocating more isn’t without debate. Common concerns include:

- Credit risk: Borrowers are often non-investment grade. Default cycles could hurt.

- Illiquidity: Lockups mean no easy exit in downturns.

- Manager dispersion: Top-quartile vs. bottom-quartile funds show wide performance gaps.

- Systemic oversight: Regulators are paying closer attention to leverage and transparency in private credit.

Institutions recognize these risks, but many believe the benefits outweigh them—especially when allocations are spread across multiple managers and strategies.

Examples of Institutional Moves

- Pension funds: Canada’s large pensions (e.g., CPPIB, Ontario Teachers’) have built significant private credit portfolios, often via direct platforms.

- Insurance companies: U.S. and European insurers are major allocators, matching long-term liabilities with illiquid but higher-yielding credit.

- Endowments: U.S. university endowments treat private credit as a staple in the alternatives bucket.

The trend is broad: not just a few innovators, but mainstream institutions making multi-billion-dollar commitments.

What It Means for Individual Investors

While individuals may not have the scale of a sovereign wealth fund, the institutional trend still matters:

- Signal effect: When big allocators commit, it validates private credit as a durable asset class.

- Access expansion: As demand rises, managers are creating retail-friendly vehicles (non-traded BDCs, interval funds).

- Competition risk: Institutional capital may compress spreads over time, making early movers better rewarded.

For individuals, following the logic of institutional allocators—seeking yield, diversification, inflation protection—can guide portfolio construction, even if the vehicles differ.

Final Thoughts

Institutions are not allocating more to private credit by accident. They see it as a solution to the twin challenges of low yields in public credit and the need for diversified, stable income in a volatile world. Add in structural tailwinds from bank retrenchment and private equity synergy, and the rationale is clear.

For investors of any size, the lesson is this: private credit isn’t just a passing trend. Institutions are making it a permanent pillar of their portfolios. The question isn’t whether allocations will grow—it’s how the asset class will evolve as trillions more flow in.

{kind=link}