This Content Is Only For Subscribers

When it comes to retirement savings, few vehicles are as powerful—or as misunderstood—as the Roth IRA. While traditional IRAs and 401(k)s are built on tax deferral, the Roth IRA flips the script: you contribute after-tax dollars today and enjoy tax-free growth and withdrawals later.

For many savers, especially those early in their careers or expecting higher taxes in the future, the Roth IRA is one of the best deals in personal finance. But to use it effectively, you need to understand how it works, its rules, and the strategies that unlock its full potential.

The Origins of the Roth IRA

The Roth IRA was introduced in 1997 under the Taxpayer Relief Act, spearheaded by Senator William Roth of Delaware. At the time, most Americans had access only to traditional IRAs and employer-sponsored plans like 401(k)s. Those accounts provided a tax deduction today but taxed withdrawals in retirement.

Lawmakers wanted a new type of retirement vehicle that would:

- Incentivize younger Americans to save early.

- Help reduce reliance on Social Security.

- Give savers flexibility in how and when they paid taxes.

The Roth IRA was designed as a complement to traditional accounts, not a replacement. By flipping the tax treatment, it allowed retirement savers to diversify their tax exposure, a concept now called tax diversification.

Since then, Roth-style accounts have expanded:

- Roth 401(k) (2006): Allowed after-tax contributions inside employer plans.

- Roth 403(b) and Roth TSP: Extended to non-profit and government employees.

- Roth Conversions: Rules expanded in 2010 to allow anyone, regardless of income, to convert.

Today, Roth IRAs are a staple of retirement planning, with tens of millions of accounts open nationwide.

The Core Features That Set Roth IRAs Apart

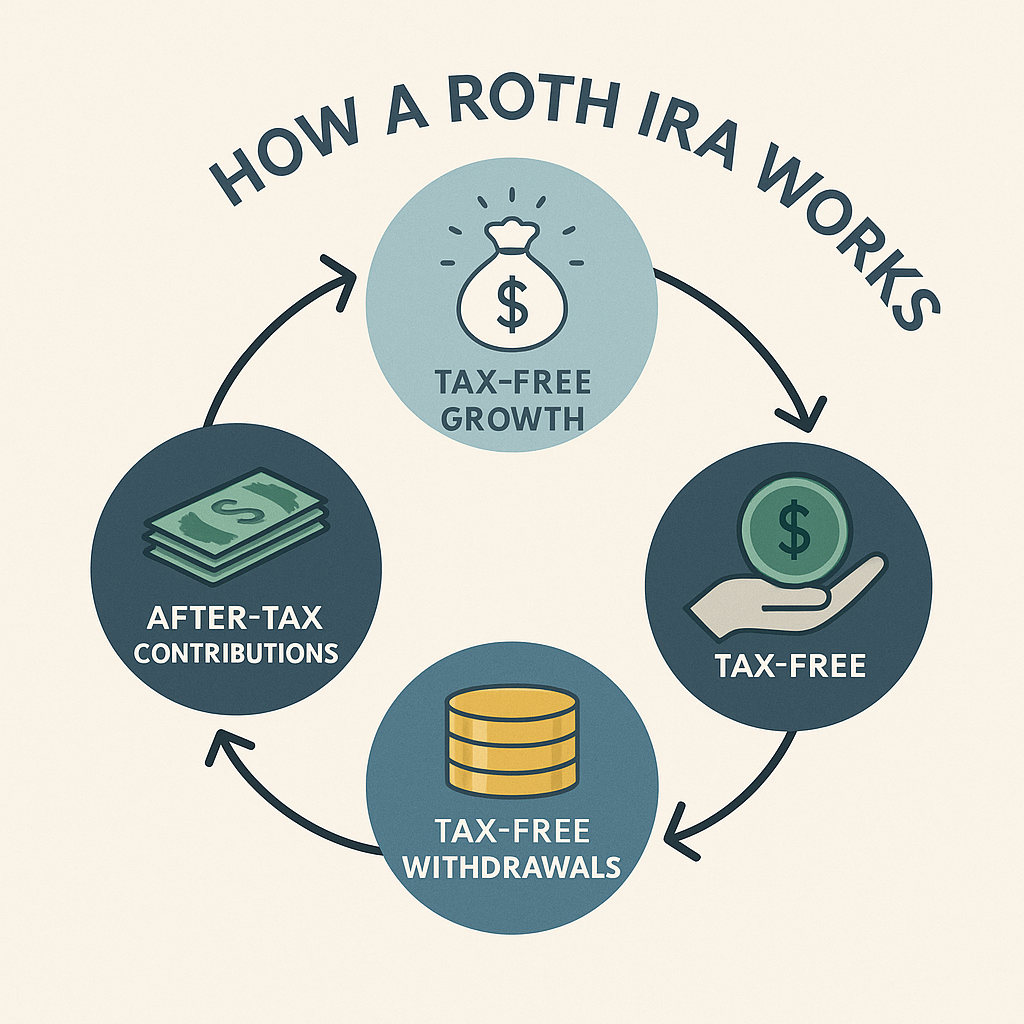

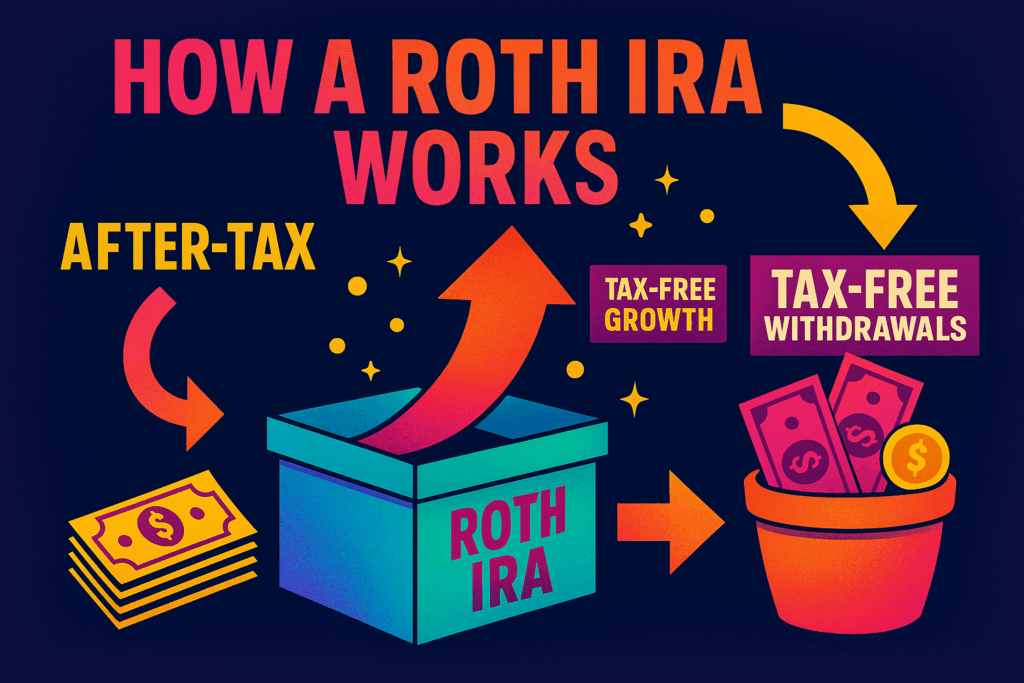

1. After-Tax Contributions

You don’t get a tax deduction when you contribute. But that’s the trade-off that unlocks future tax-free withdrawals.

2. Tax-Free Growth

All dividends, interest, and capital gains inside a Roth grow without yearly taxation. That means no capital gains taxes, no dividend taxes, no headaches every April.

3. Qualified Withdrawals Are Tax-Free

Once you’re age 59½ and meet the five-year holding requirement, both your contributions and earnings come out completely tax-free.

4. No Required Minimum Distributions (RMDs)

Unlike traditional IRAs, Roths don’t force withdrawals during your lifetime. This makes them excellent for estate planning and long-term compounding.

5. Flexible Contribution Withdrawals

You can withdraw contributions (but not earnings) anytime, penalty-free. This unique feature makes Roths more versatile than most people realize.

Contribution Limits and Income Eligibility

For 2024:

- Annual contribution limit: $7,000 (or $8,000 if 50+).

- Income phase-out:

- Single filers: begins at $146,000, ends at $161,000.

- Married filing jointly: begins at $230,000, ends at $240,000.

These limits are indexed to inflation, so they increase every few years.

Example Scenarios

- Anna (single, income $100,000): Can contribute the full $7,000.

- Tom & Lisa (joint income $240,000): Cannot contribute directly. Instead, they can use a backdoor Roth strategy by contributing to a traditional IRA and converting.

Contributions vs. Conversions

It’s important to distinguish between two ways of funding a Roth IRA:

- Contributions: Depositing new after-tax money each year, subject to income and annual limits.

- Conversions: Moving money from a pre-tax IRA or 401(k) into a Roth IRA, paying taxes on the conversion.

Conversions are especially powerful for high earners who can’t contribute directly due to income limits.

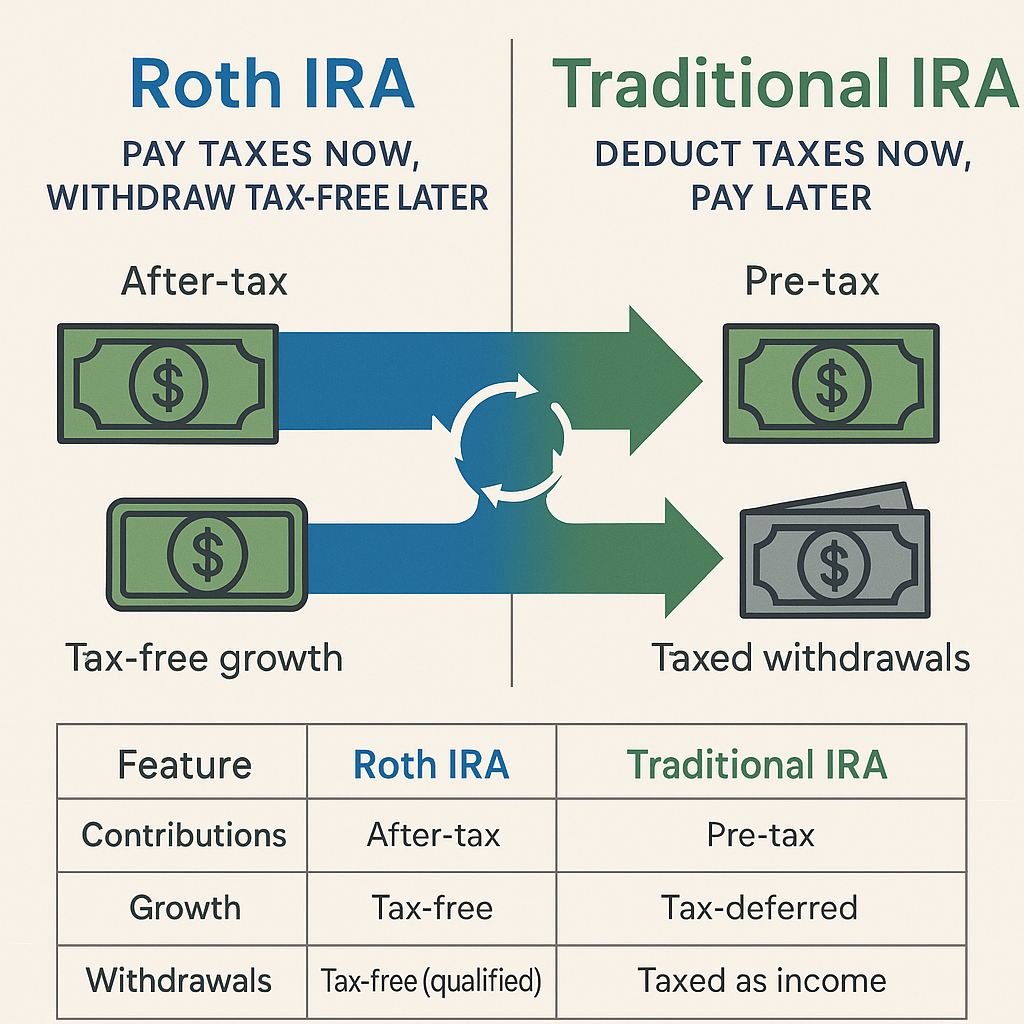

Roth IRA vs. Traditional IRA: A Deeper Comparison

The difference between Roth and traditional IRAs boils down to when you pay taxes:

- Traditional IRA: You pay no tax now, but withdrawals are taxed as income later.

- Roth IRA: You pay tax now, but withdrawals are tax-free later.

Numerical Comparisons

Same Tax Rate Now and Later

If your tax bracket is 25% today and 25% in retirement, both Roth and traditional produce the same after-tax wealth.

Higher Tax Rate in Retirement

- Pay 22% now in a Roth, withdraw at 28% later? The Roth wins.

- For younger workers, this scenario is common since earnings (and tax brackets) tend to rise.

dLower Tax Rate in Retirement

- Pay 32% now, but only 22% later? Traditional IRA wins.

- This often applies to those in peak-earning years who expect to downshift in retirement.

Case Study: $6,000 Annual Contribution for 30 Years

- Traditional IRA (25% retirement tax rate): Balance grows to ~$610,000, but only ~$457,000 is spendable after tax.

- Roth IRA: Same balance (~$610,000), but all tax-free.

That’s why Roths are often recommended for younger workers and those who expect higher future tax rates.

The Power of Tax-Free Compounding

Roth IRAs shine because all growth compounds free of taxes.

Example:

Two investors each contribute $6,000/year for 30 years at 7%.

- Taxable account (15% annual tax drag): ~$510,000.

- Roth IRA: ~$610,000, all tax-free.

That $100,000+ difference is purely due to eliminating annual taxes.

Now scale it: max contributions for 40 years at 7% could leave you with over $1.3 million tax-free.

Withdrawal Rules in Detail

Ordering Rules

When you withdraw, the IRS uses this sequence:

- Contributions.

- Conversions.

- Earnings.

Qualified Withdrawals

- Must be age 59½ or older.

- Must have held the Roth at least 5 years.

Penalty Exceptions

You can avoid the 10% penalty (but not always taxes) if funds are used for:

- First-time home purchase (up to $10,000).

- Education expenses.

- Disability.

- Medical expenses above 7.5% of AGI.

The Five-Year Rule Explained

The five-year rule trips up many investors. The essentials:

- The clock starts January 1 of the year you made your first contribution.

- Each conversion has its own 5-year clock.

- Contributions are always available penalty-free.

Strategy tip: Start your Roth early, even with $100, to get your 5-year clock running.

Roth Conversions in Depth

Why Convert?

- Avoid RMDs.

- Pay taxes now at lower rates.

- Leave heirs tax-free assets.

Best Times to Convert

- Early retirement years (before Social Security/RMDs).

- Market downturns (convert at lower values).

- Gap years with temporarily lower income.

Conversion Ladder Strategy

Convert a portion each year for 5–10 years, keeping yourself in a lower bracket. Over time, you build a tax-free Roth “pipeline” while smoothing out taxes.

Roth IRA Use Cases

Young Professional

- Lower income now, higher income later.

- Contribute as much as possible early.

Mid-Career Saver

- Already has large pre-tax balances.

- Use Roth for diversification.

Entrepreneur

- Income fluctuates, great opportunity for conversions in low years.

Near Retiree

- Use conversions before RMD age.

- Best for leaving tax-free money to heirs.

Coordinating Roths with Other Accounts

Roths work best as part of a balanced strategy:

- 401(k): Max out employer match.

- Traditional IRA: Use when tax deduction is more valuable.

- HSA: Use for healthcare with triple tax advantage.

- Taxable accounts: Provide liquidity but taxed annually.

Asset location tip: Put growth-oriented assets (stocks, small-cap funds) in Roths to maximize tax-free compounding.

Roths in Estate Planning

Roth IRAs are one of the most efficient wealth-transfer tools.

- No RMDs for original owner.

- Heirs get 10 years to withdraw.

- Spouses can roll into their own Roth.

- Trusts can control distributions for minors or heirs with poor financial discipline.

Because withdrawals are tax-free, heirs inherit the full value—unlike taxable traditional IRAs.

Special Uses of Roth IRAs

- First-Time Homebuyers: Up to $10,000 of earnings penalty-free.

- Education Expenses: Withdraw without penalty, though taxed if earnings.

- Emergency Fund: Contributions always accessible.

- FIRE Movement: Roth conversion ladders let early retirees tap money before 59½.

Myths and Misconceptions

- “Roths are only for young people.” False—estate planning benefits older savers too.

- “All Roth withdrawals are tax-free.” False—only qualified withdrawals are.

- “You can’t touch a Roth until retirement.” False—contributions are always accessible.

- “Conversions must be all or nothing.” False—you can spread them over years.

Global Perspective

Other countries have Roth-like accounts:

- UK ISAs: After-tax contributions, tax-free withdrawals.

- Canada TFSA: Similar to Roth, but higher flexibility.

- Australia Superannuation: Has tax-advantaged components.

The U.S. Roth remains unique for its combination of rules, but global parallels show how valuable tax-free retirement accounts are.

FAQs (Expanded)

- Can I contribute to both Roth and Traditional IRAs? Yes, but the combined limit applies.

- Can I lose money in a Roth? Yes, investment risk still applies.

- What if I exceed the income limit? Remove excess or face a 6% penalty each year.

- Can I roll a Roth 401(k) into a Roth IRA? Yes, and doing so avoids RMDs.

- Should I prioritize Roth or Traditional? Depends on your current vs. future tax rate.

Practical Checklist for Roth Savers

- ✅ Contribute as early as possible each year.

- ✅ Automate contributions.

- ✅ Track your five-year rule.

- ✅ Keep records of contributions vs. conversions.

- ✅ Revisit Roth vs. Traditional each year as income changes.

- ✅ Plan conversions strategically, not impulsively.

Final Thoughts

The Roth IRA isn’t just an account—it’s a strategy. It provides tax-free growth, flexible withdrawals, estate-planning advantages, and peace of mind against future tax uncertainty.

Whether you’re a young saver just starting out or a retiree planning your legacy, the Roth IRA has a role. By combining smart contributions, strategic conversions, and careful withdrawal planning, you can unlock one of the most powerful tools in personal finance.

{kind=link}