This Content Is Only For Subscribers

A Roth IRA is one of the most attractive retirement accounts available. Tax-free growth, tax-free withdrawals, and no required minimum distributions (RMDs) make it a powerful tool for building long-term wealth. But there’s one detail that trips up many savers: income limits.

Unlike traditional IRAs, where anyone with earned income can contribute (though deductions may be limited), Roth IRAs have strict rules about who can put money in directly. Understanding these limits—and the strategies around them—can mean the difference between missing out and maximizing your retirement plan.

Why Income Limits Exist

Congress designed Roth IRAs with an eye toward middle-income Americans. Since Roth contributions use after-tax dollars and grow tax-free, lawmakers wanted to ensure the benefits didn’t skew entirely toward high-income households.

The result: Roth IRAs come with a Modified Adjusted Gross Income (MAGI) phase-out range. If your income falls below the range, you can contribute the full annual amount. If it’s inside the range, you can contribute partially. If it’s above the top of the range, you can’t contribute directly at all.

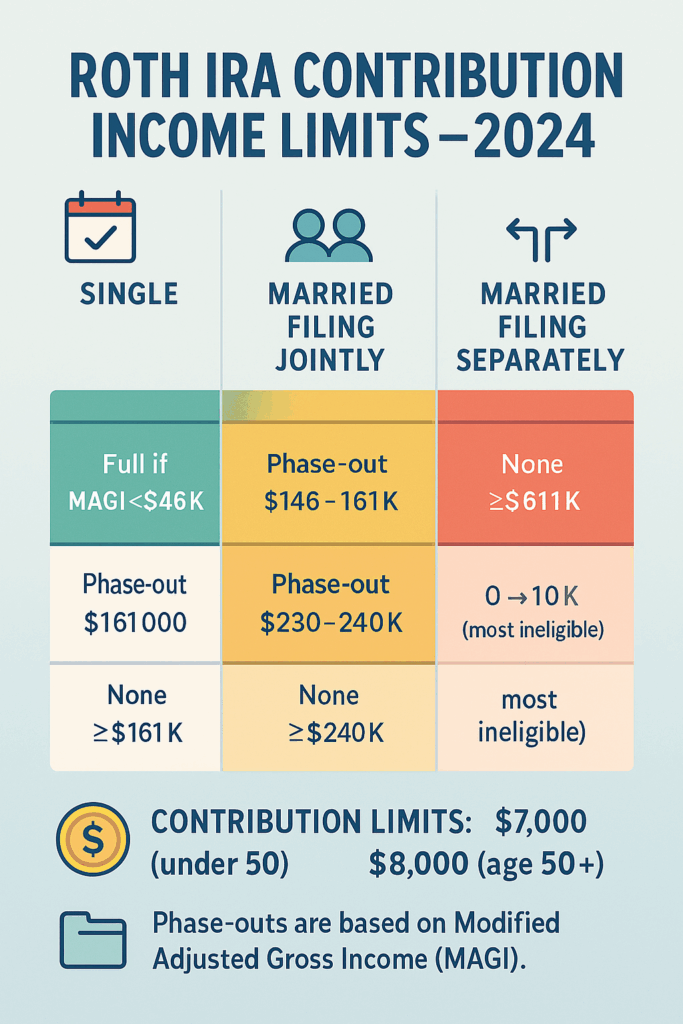

Contribution Limits for 2024

The annual limits are the same whether you contribute to a Roth IRA, a traditional IRA, or a combination of the two:

- $7,000 per year for those under age 50.

- $8,000 per year for those age 50 or older (thanks to a $1,000 “catch-up contribution”).

These numbers apply per person, not per household. A married couple with both partners eligible could contribute $7,000 each (or $8,000 each if both are 50+).

2024 Income Phase-Out Ranges

For 2024, the IRS set the Roth IRA income limits as follows:

- Single Filers: Full contribution if MAGI < $146,000. Phase-out between $146,000 and $161,000. No direct contribution if MAGI ≥ $161,000.

- Married Filing Jointly: Full contribution if MAGI < $230,000. Phase-out between $230,000 and $240,000. No direct contribution if MAGI ≥ $240,000.

- Married Filing Separately: Phase-out between $0 and $10,000—effectively, you cannot contribute if you file separately and live with your spouse at any point during the year.

Full, Partial, or No Contribution: Examples

Example 1: Below the Threshold

Sarah, single, earns $100,000 in MAGI. She can contribute the full $7,000 to a Roth IRA.

Example 2: Inside the Phase-Out Range

Michael, single, has a MAGI of $155,000. That’s $9,000 into the $15,000 phase-out band ($161,000 – $146,000). He can contribute only about 40% of the limit, or $2,800.

Example 3: Above the Threshold

Emily and Jason, married filing jointly, earn $250,000 MAGI. They exceed the $240,000 cap and cannot make direct Roth contributions at all.

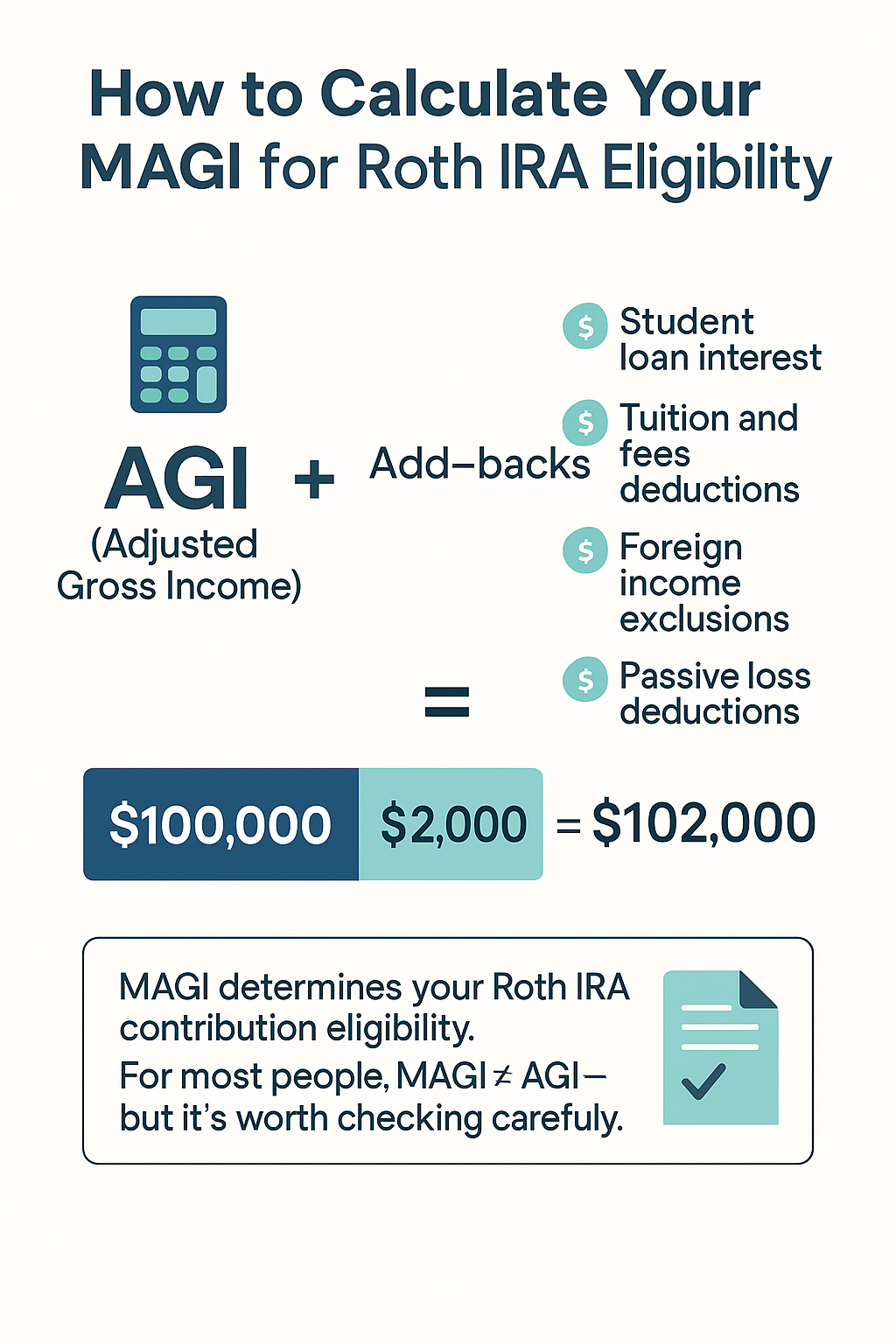

How to Calculate Your MAGI

The IRS defines Modified Adjusted Gross Income (MAGI) for Roth eligibility as your Adjusted Gross Income (AGI) plus certain add-backs. Common adjustments include:

- Student loan interest deductions.

- Tuition and fees deductions.

- Foreign earned income exclusions.

- Passive loss deductions.

For most people, MAGI is very close to AGI, but it’s worth double-checking with tax software or a CPA.

What If You Earn Too Much?

Being over the income limit doesn’t mean the Roth IRA is off-limits forever. Savers have options:

1. The Backdoor Roth IRA

This strategy involves:

- Contributing to a traditional IRA with after-tax dollars (non-deductible contribution).

- Converting that contribution to a Roth IRA.

Since there are no income limits on conversions, this effectively bypasses the direct contribution restriction.

Caution: The pro-rata rule can complicate things if you already have pre-tax IRA balances.

2. The Mega Backdoor Roth

Some 401(k) plans allow after-tax contributions beyond the standard limits. These can be rolled over into a Roth IRA or Roth 401(k), allowing tens of thousands of dollars in Roth contributions annually.

3. Roth Conversions in Retirement Planning

Even high earners who can’t contribute directly may find it smart to convert existing pre-tax accounts during low-income years, such as early retirement before Social Security or RMDs begin.

Why Income Planning Matters

Income-based eligibility rules make Roth IRAs not just about saving but also about tax planning. A bonus, capital gain, or business income could unexpectedly push you into the phase-out range, shrinking or eliminating your ability to contribute directly.

Strategies to stay eligible may include:

- Increasing 401(k) contributions to lower MAGI.

- Using pre-tax health savings account (HSA) contributions.

- Timing the realization of investment gains.

The Big Picture: Contribution Strategy

Here’s how investors often prioritize:

- Contribute enough to your 401(k) to get the employer match. Free money is hard to beat.

- Max out your Roth IRA if eligible. Locking in tax-free growth is incredibly powerful.

- Return to your 401(k) or taxable accounts. Once Roth and match are maxed, put remaining savings there.

For higher earners, step 2 may involve the backdoor Roth.

Key Takeaways

- Roth IRAs have strict income eligibility rules tied to your MAGI.

- For 2024, single filers phase out between $146,000–$161,000; married joint filers between $230,000–$240,000.

- Contribution limits are $7,000 ($8,000 if 50+).

- If your income is too high, strategies like the backdoor Roth can keep the door open.

Final Thoughts

The Roth IRA is one of the most flexible and powerful accounts for retirement savings, but income limits add complexity. By understanding how the phase-out ranges work—and using strategies like backdoor contributions—you can ensure you don’t miss out on the chance to build a tax-free income stream for the future.

Planning ahead, checking your MAGI, and adjusting contributions before year-end can help you take full advantage of what the Roth IRA offers.

{kind=link}