This Content Is Only For Subscribers

Private equity (PE) isn’t just deal-making—it’s also a chain of tax choices that shapes what investors keep after fees. Here’s a clear, plain-English guide to the big ideas so you can read fund documents with confidence and ask sharper questions.

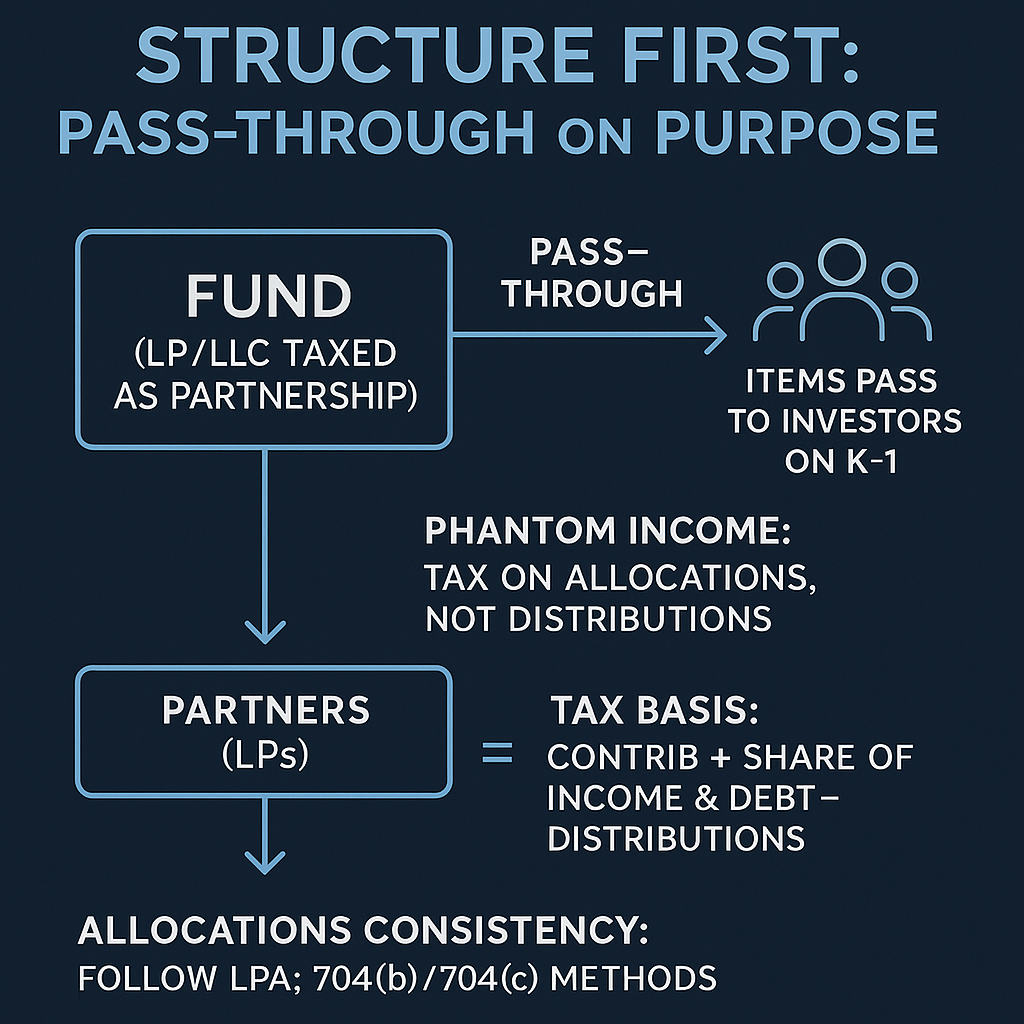

Structure first: pass-through on purpose

Most PE funds are LPs or LLCs taxed as partnerships. The fund generally doesn’t pay income tax; instead, items of income, gain, loss, and deduction pass through to investors on Schedule K-1.

Why it matters:

- You’re taxed on allocations, not distributions—so “phantom income” can happen.

- Your tax basis (contributions + share of income and debt − distributions) influences whether losses are usable and whether distributions are taxable.

- Allocations should follow the partnership agreement and be consistent over time, even if the math (704(b), 704(c)) looks gnarly.

Three investor lenses

U.S. taxable investors

- Character and holding period matter: >1-year gains are typically long-term capital gains; interest, fees, and short-term gains tend to be ordinary income.

- State taxes add a second layer. Some funds file composite returns or withhold on your behalf; others leave state filings to you.

U.S. tax-exempts (endowments, foundations, pensions, IRAs)

- Watch for UBTI (unrelated business taxable income), including debt-financed income.

- Funds often use blocker corporations (frequently offshore) to prevent UBTI from passing through—effective, but with corporate-level tax leakage.

Non-U.S. investors

- The big worry is ECI (effectively connected income) from a U.S. trade or business, which can trigger U.S. filings.

- Blockers are commonly used for operating U.S. businesses; FIRPTA may bite on U.S. real estate.

Carry, fees, and offsets

- Management fees (often 1–2%) are fund expenses and generally ordinary income to the adviser.

- Carried interest typically seeks capital-gain treatment when the underlying gains are capital, but the three-year holding period rule can recharacterize some gains if exits are too quick.

- Fee offsets credit certain portfolio-company fees (monitoring/transaction) against management fees—good for LPs, but check which fees count and how offsets apply across co-investments.

- Fee waivers (waiving fees for a larger share of future profits) need real entrepreneurial risk to avoid ordinary-income treatment; they change timing and economics for everyone.

How tax shapes deals

Buying:

- Asset vs. stock purchases: assets can deliver a basis step-up and future depreciation/amortization, but sellers may resist. Elections (e.g., 338(h)(10) in certain situations) try to combine stock mechanics with asset tax treatment.

- Purchase price allocation drives future deductions—more allocated to amortizable intangibles usually means bigger deductions later.

During the hold:

- Interest-deductibility limits and NOL rules affect portfolio-company cash taxes.

- Growth can trigger state nexus—more filings, more complexity.

Exiting:

- Character (capital vs. ordinary), timing (earn-outs, installments), and cross-border withholding/treatiesinfluence the after-tax outcome.

K-1s, timing, and estimates

K-1s often arrive after April; most investors extend returns. Practical moves:

- Use prior-year K-1s and sponsor guidance for estimated payments.

- Track basis—distributions above basis can be taxable; losses need basis to be deductible.

- Watch capital account swings and ask for explanations of big moves (write-downs, 704(c) adjustments).

Cross-border layers

- Withholding. Non-U.S. holders may face U.S. withholding on dividends/interest; U.S. investors in foreign companies may face foreign withholding (potential foreign tax credits).

- Treaties can reduce withholding, but depend on residency and limitation-on-benefits tests.

- FATCA/CRS: be ready for W-8/W-9 documentation and occasional information reporting. It’s routine, but forms must stay current.

Credits, incentives, and ESG

Policy incentives—especially in energy and manufacturing—can boost returns:

- Transferable tax credits can be monetized but carry eligibility and recapture risks.

- State/local incentives (jobs or investment credits) come with compliance milestones.

- If you tout ESG outcomes tied to incentives, keep tax and legal teams aligned so the story and the qualificationsmatch.

Common pain points (and fixes)

UBTI surprises for tax-exempts

- Ask explicitly about blocker use for operating income and debt-financed situations.Phantom income and cash planning

Phantom income and cash planning

- Clarify whether the fund makes tax distributions and how it handles timing gaps between taxable allocations and cash exits.

State filing sprawl

- Will the fund handle composites/withholding, or are you filing in a dozen states

Carried-interest clock

- How does the GP manage exits under the three-year rule? What happens in the waterfall if a sale is early?

K-1 process

- What’s the timeline? Are draft K-1s or estimates provided? How are special items (foreign tax credits, PFIC/QEF statements) supported?Paperwork discipline

Paperwork discipline

- Ensure purchase price allocations, intercompany agreements, and debt terms are contemporaneous—not reconstructed later.

A tighter diligence checklist

- Structure map (feeders/blockers; who they protect and what they cost)

- UBTI/ECI policy (when blockers are used; impact on yield)

- Fee mechanics (offsets/waivers with numeric examples)

- Distribution policy (tax distributions? priorities and timing)

- State approach (composites/withholding vs. investor filings)

- K-1 workflow (timelines, estimates, support)

- Acquisition planning (asset vs. stock, elections, allocation logic)

- Exit playbook (character, earn-outs, withholding/treaties)

Bottom line

In private equity, tax is part of the return engine. Strong managers bake tax into the plan at formation (pass-throughs, blockers), at acquisition (basis step-ups, elections), during operations (interest limits, state nexus), and at exit (character and timing). You don’t need to memorize code sections—just bring the right questions. If the sponsor can explain structure, blockers, fee mechanics, distributions, state strategy, and K-1 timing with numbers, you’re far more likely to see the value created in the portfolio show up in your after-tax results.

{kind=link}