Planning for retirement can feel like a distant and abstract goal, especially when you’re juggling bills, student loans, or day-to-day expenses. But the sooner you start thinking strategically, the more time your money has to grow. One of the most powerful tools in your retirement toolbox is a tax-deferred retirement account, like a traditional IRA or a 401(k). These accounts don’t just let you save — they let your money grow faster by deferring taxes until you withdraw it in retirement.

In this article, we’ll break down the benefits of tax-deferred accounts, how they work, and why they might deserve a prominent place in your retirement plan.

What Does “Tax-Deferred” Mean?

When an account is tax-deferred, you don’t pay income taxes on the money you contribute or on any investment gains each year. Instead, taxes are postponed until you withdraw the funds, typically in retirement. This is different from taxable brokerage accounts, where you pay taxes annually on dividends, interest, and capital gains.

Here’s a simple example:

- Without tax deferral: You invest $6,000 a year in a taxable account that earns 7% annually. Each year, you pay taxes on the gains. Over 30 years, taxes chip away at your growth.

- With tax deferral: The same $6,000 goes into a traditional IRA. You don’t pay taxes on contributions or gains each year. Over 30 years, the account compounds more efficiently, potentially leaving you tens of thousands more at retirement.

By delaying taxes, your money can grow faster — and compounding works even harder in your favor.

How Tax-Deferred Accounts Work

The mechanics of a tax-deferred account are fairly straightforward:

- Contributions may be deductible: In a traditional IRA, the money you contribute can reduce your taxable income for that year (if you meet eligibility rules). This immediate tax break can be especially helpful if you’re in a higher tax bracket today.

- Investments grow without annual taxation: Stocks, bonds, mutual funds, or ETFs inside the account generate dividends, interest, and capital gains. Unlike a regular brokerage account, you don’t pay taxes on these gains every year.

- Taxes are paid upon withdrawal: When you start taking money out, typically after age 59½, withdrawals are taxed as ordinary income. The key is that you’re likely to be in a lower tax bracket in retirement, so the overall tax burden may be smaller.

This “pay later” system is why tax-deferred accounts are so powerful: you get the immediate benefit of tax-free growth while postponing the tax hit until a time when it may be less impactful.

Compounding Growth Is Your Secret Weapon

Compounding is often called the eighth wonder of the world, and tax-deferred accounts magnify it. Every dollar of investment gain that isn’t taxed each year can be reinvested, generating additional returns. Over decades, this snowball effect can be dramatic.

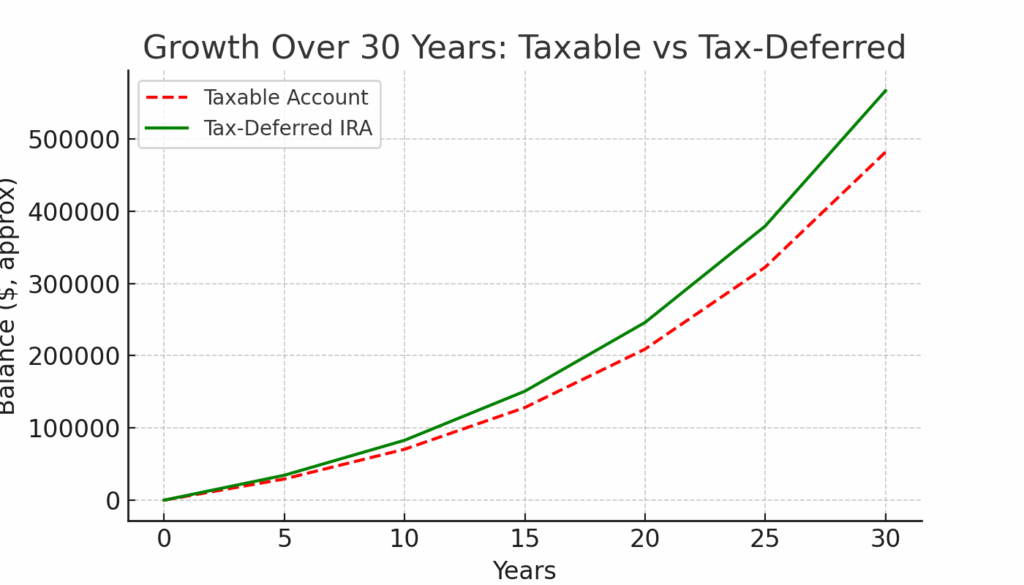

Let’s say you invest $6,000 a year in a traditional IRA earning 7% annually for 30 years:

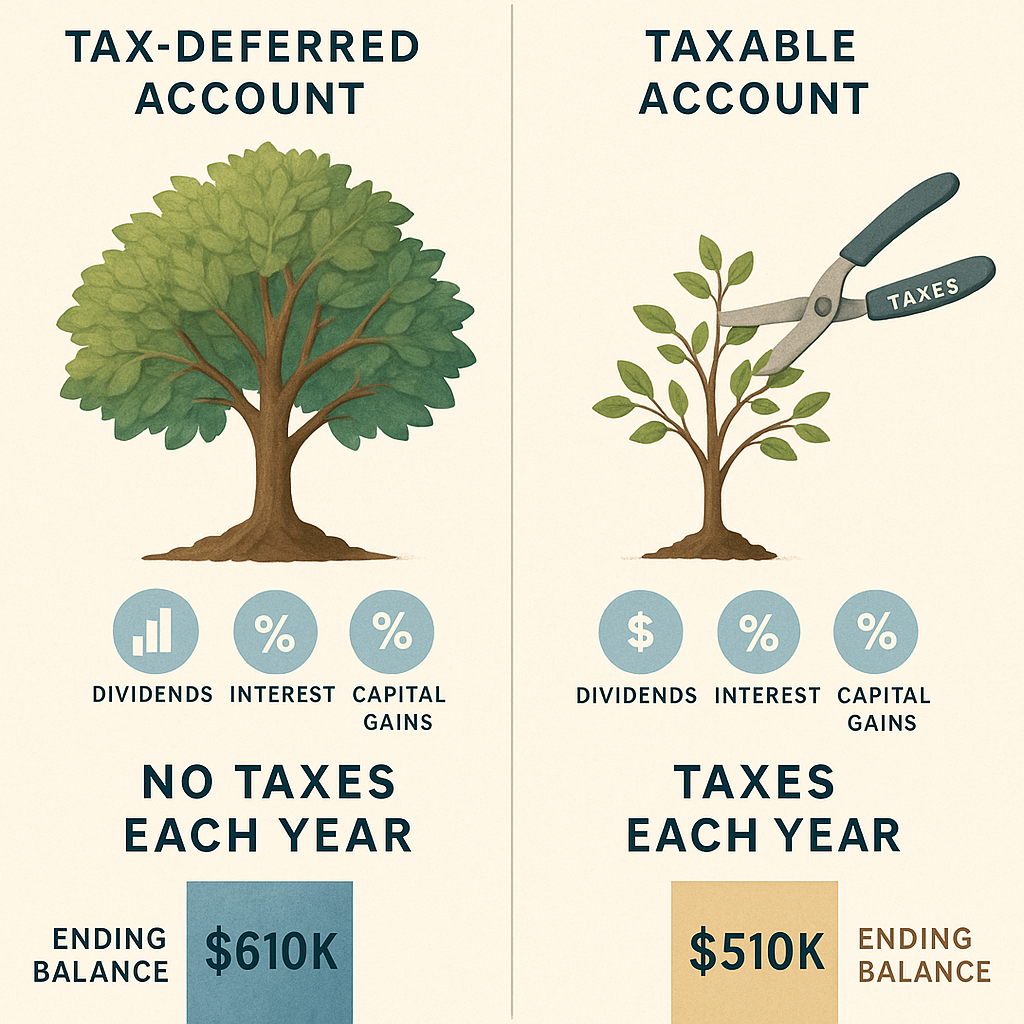

- In a taxable account, your ending balance might be around $510,000 after annual taxes on gains.

- In a tax-deferred IRA, your balance could grow to approximately $610,000 — a difference of $100,000, without increasing your contributions.

That’s the real benefit: letting the government temporarily “sit on” your taxes allows your investments to work harder for you.

Flexibility and Choice

Tax-deferred accounts aren’t just about tax savings. They also give you control over your investment strategy. Depending on the provider, you can choose from:

- Stocks — for higher growth potential

- Bonds — for stability and income

- Mutual funds and ETFs — for diversification

- Target-date funds — which automatically adjust your allocation as retirement approaches

This flexibility means you can tailor your portfolio to your risk tolerance, investment timeline, and retirement goals.

Additional Benefits

Beyond tax deferral and compounding, these accounts offer other advantages:

- Potential for employer matching: If you contribute to a 401(k), your employer may match a portion of your contributions, essentially giving you free money toward retirement.

- Disciplined saving: Because funds in a tax-deferred account are subject to early withdrawal penalties (typically before age 59½), these accounts encourage long-term savings.

- RMD planning: Traditional IRAs require Required Minimum Distributions (RMDs) starting at age 73, which helps structure retirement withdrawals. Planning around RMDs can also provide opportunities for tax management.

Comparing Tax-Deferred and Tax-Free Accounts

It’s important to distinguish between tax-deferred accounts and tax-free accounts, like Roth IRAs. Both offer significant tax benefits, but in different ways:

- Tax-deferred (traditional IRA, 401(k)): Tax deduction upfront, pay taxes on withdrawals later.

- Tax-free (Roth IRA): Pay taxes upfront, withdrawals in retirement are tax-free.

Choosing between the two often depends on your current tax bracket, expected retirement income, and personal preference for tax timing. Many investors benefit from a combination of both.

Why Start Early

Time is one of the most powerful factors in retirement savings. The earlier you start contributing to a tax-deferred account, the more opportunity compounding has to work its magic. Even modest annual contributions can grow significantly over decades, especially when the investments inside the account are allowed to grow without annual taxation.

For example, contributing $5,000 per year starting at age 25 could yield over $600,000 by age 65 at a 7% return — while starting at 35 might only yield about $330,000 under the same conditions. That’s the compounding advantage amplified by tax deferral.

Final Thoughts

Tax-deferred retirement accounts like traditional IRAs and 401(k)s are more than just accounts — they are strategic tools for growing wealth efficiently. By delaying taxes, maximizing compounding, and maintaining control over investments, these accounts can significantly improve your long-term financial outcomes.

For novice investors, the key takeaways are simple:

- Contribute early and consistently.

- Take advantage of employer matches if available.

- Use tax-deferred accounts to complement tax-free options like Roth IRAs.

Ultimately, the combination of tax deferral and disciplined investing gives your money a much better chance to grow, helping you reach retirement goals with greater security and peace of mind.

{kind=link}