This Content Is Only For Subscribers

Saving for retirement can feel overwhelming, especially with the numerous account types, investment options, and tax rules. One of the most powerful and accessible tools available to most Americans is the Traditional Individual Retirement Account (IRA). It combines investment growth potential, tax advantages, and flexibility, making it a cornerstone of long-term financial planning.

Understanding how a Traditional IRA works — from contributions to growth and withdrawals — is crucial for building a secure retirement. This guide is designed for novice investors and provides practical, real-world advice.

What Is a Traditional IRA?

A Traditional IRA is a retirement account that offers tax advantages for long-term saving. Unlike employer-sponsored plans like a 401(k), a Traditional IRA is individually owned, giving you full control over contributions, investment choices, and timing of withdrawals.

Key Features:

- Tax-deductible contributions: You may reduce your taxable income for the year by contributing to a Traditional IRA.

- Tax-deferred growth: Investments inside the account grow without being taxed until withdrawn.

- Ordinary income taxation at withdrawal: Distributions are taxed as regular income in retirement.

This combination of features allows your money to grow faster over time because taxes do not reduce investment returns annually.

Contributions: Eligibility, Limits, and Deadlines

Contributing to a Traditional IRA is relatively simple, but understanding the rules is key.

Annual Limits

For 2025, the maximum contribution is:

- $7,000 if under 50 years old

- $8,000 if 50 or older (includes a $1,000 “catch-up” contribution)

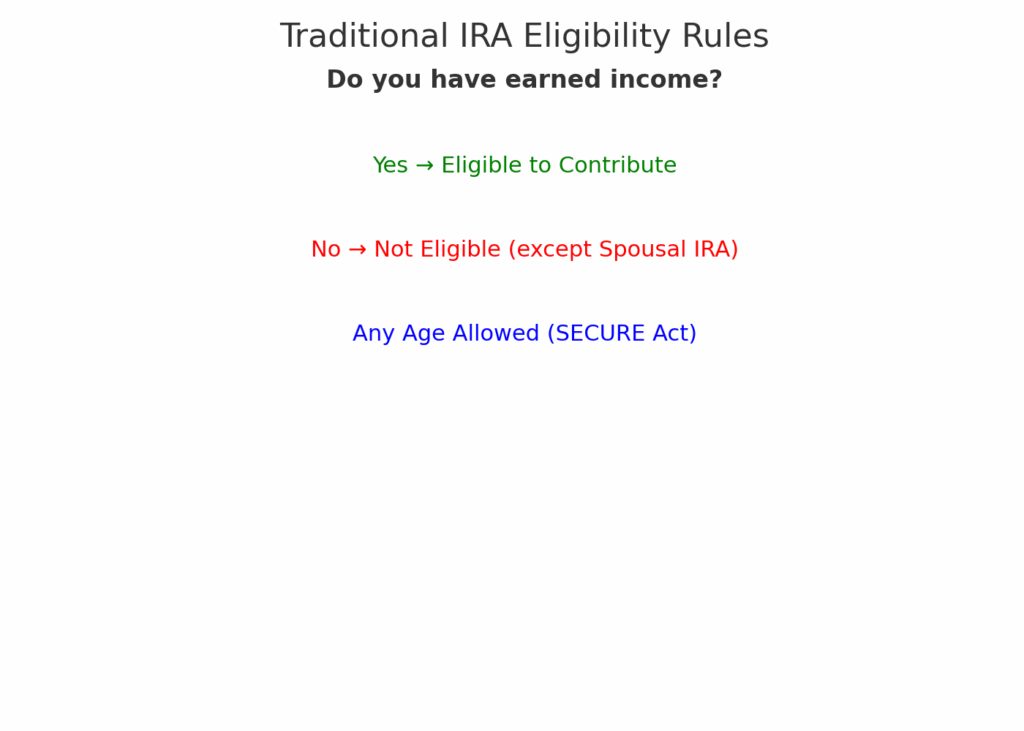

Earned Income Requirement

You must have earned income, such as wages, salaries, or self-employment income. Passive income like interest, dividends, rental income, or gifts does not qualify.

Contribution Deadline

Contributions for a given tax year can be made until the tax-filing deadline of the following year, usually April 15. This allows for some flexibility in planning contributions.

Eligibility and Special Scenarios

- Anyone with earned income can contribute. There’s no minimum age requirement, and even those just starting their first job can begin building a retirement fund.

- Spousal IRA: If one spouse has little or no earned income, contributions can still be made through a spousal IRA, provided the other spouse has sufficient earned income.

- No upper age limit: Thanks to the SECURE Act, you can contribute to a Traditional IRA at any age as long as you have earned income.

This means a wide range of individuals, from young professionals to self-employed entrepreneurs and stay-at-home parents, can benefit from a Traditional IRA.

Understanding Contribution Nuances

While the contribution limits seem straightforward, there are several subtleties that often confuse novice investors. For example, your ability to deduct Traditional IRA contributions depends on your income and whether you or your spouse participate in a workplace retirement plan. Here’s how it works:

- Single filers covered by a 401(k): For 2025, if your modified adjusted gross income (MAGI) is $73,000 or less, you can deduct the full contribution. Between $73,000 and $83,000, the deduction phases out. Above $83,000, you cannot deduct contributions.

- Married filing jointly, both covered by workplace plans: The phase-out range is $116,000 to $136,000.

- Married filing jointly, only one spouse covered: The non-covered spouse can deduct contributions fully if household MAGI is below $218,000, phasing out by $228,000.

Understanding these limits is critical because contributing without deductibility when you expect to be eligible could reduce tax benefits.

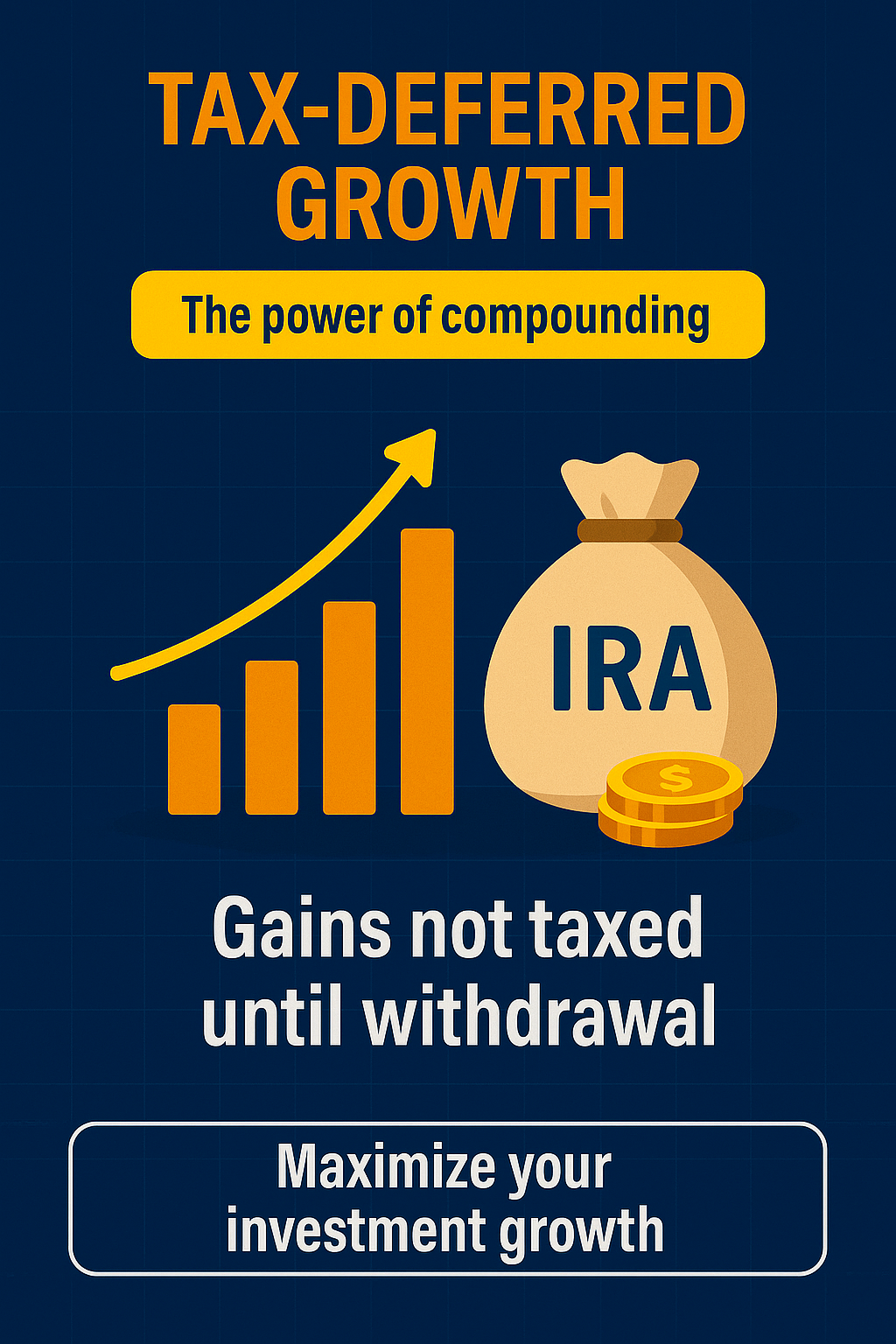

Investment Options and Growth Potential

The real power of a Traditional IRA lies in the ability to grow your investments tax-deferred.

Investment Choices

Within a Traditional IRA, you can invest in:

- Individual stocks for growth potential

- Bonds for stability and predictable income

- Mutual funds and ETFs for diversification

- Target-date funds that automatically adjust the allocation based on your retirement timeline

The Power of Compounding

Because taxes are deferred, your investments can grow exponentially over time. For example:

- Alex invests $6,000 annually in a taxable account for 30 years at 7% annual returns. After taxes on dividends and capital gains, Alex may end up with around $510,000.

- Jordan invests the same amount in a Traditional IRA. With tax-deferred growth, Jordan could have closer to $610,000 — a difference of $100,000, achieved purely through tax deferral.

Even small contributions made consistently can add up significantly over decades.

Real-Life Example

Consider Sarah, who starts contributing $200 per month to a Traditional IRA at age 25, with a 6% average annual return:

- By age 65, her account could grow to over $290,000.

- If she waits until age 35 to start the same contributions, her balance would only reach about $150,000.

This illustrates the importance of starting early, even with modest monthly contributions.

Maximizing Growth: Choosing Investments Wisely

While tax-deferred growth is powerful, investment selection inside your IRA matters even more. Many beginners make the mistake of holding cash or low-yield CDs in their IRA, which may protect against risk but limits long-term growth. To balance risk and reward:

- Younger investors: Consider a higher allocation to stocks or stock index funds. The long investment horizon allows you to recover from short-term volatility.

- Mid-career investors: Balance equities with bonds or bond funds to reduce risk while maintaining growth potential.

- Near-retirement investors: Gradually shift to more conservative investments to preserve capital while still beating inflation.

Case Study: Aggressive vs. Conservative Investing

- Jake starts at 25, investing $200 per month aggressively in a mix of 90% equities and 10% bonds, achieving 8% average annual returns. By 65, his IRA could grow to around $380,000.

- Mike, also starting at 25, invests the same amount conservatively in 40% equities and 60% bonds, earning 5% annually. His balance at retirement might reach only $245,000.

This shows the long-term impact of investment strategy in addition to consistent contributions and tax-deferred growth.

Withdrawals: Timing and Rules

While Traditional IRAs offer tax advantages, the IRS has rules governing withdrawals.

Standard Withdrawals

- Age 59½ or older: Withdrawals are penalty-free but are taxed as ordinary income.

- Early withdrawals: Generally incur a 10% penalty plus income tax.

Exceptions to Early Withdrawal Penalties

Certain circumstances allow penalty-free withdrawals, including:

- First-time home purchases (up to $10,000)

- Qualified education expenses

- Certain medical expenses

- Health insurance premiums during unemployment

- Total and permanent disability

Required Minimum Distributions (RMDs)

- Begin at age 73, based on account balance and life expectancy

- Required withdrawals prevent indefinite tax deferral

- Failure to take RMDs triggers a 50% penalty on the amount not withdrawn

Planning for RMDs is essential to avoid unexpected tax bills in retirement.

Tax Advantages Explained

The tax benefits of a Traditional IRA are multifaceted:

- Immediate deduction: Contributions can lower your taxable income, especially beneficial if you are in a higher tax bracket.

- Tax-deferred growth: Earnings accumulate without annual taxation, maximizing compounding.

- Potentially lower taxes in retirement: Ideally, withdrawals are made when your income is lower, reducing the tax burden.

For many investors, these benefits can result in tens or hundreds of thousands of dollars more in retirementcompared to a taxable account.

Benefits Beyond Taxes

- Investment flexibility: Choose investments that align with your risk tolerance and long-term goals.

- Accessibility: Almost anyone with earned income can open an account.

- Discipline: Penalties for early withdrawals encourage long-term savings.

- Estate planning: IRAs can be passed on to heirs, though taxes may apply.

Strategies to Maximize Your IRA

For novice investors, consider:

- Start early and stay consistent: Even small monthly contributions grow substantially over time.

- Diversify investments: Combine stocks, bonds, and funds to balance risk.

- Monitor contribution limits: Avoid over-contributions to prevent penalties.

- Plan withdrawals carefully: Understand RMDs, taxes, and potential penalties.

- Combine with other accounts: Use a mix of 401(k)s, Roth IRAs, and taxable accounts for tax diversification.

Advanced Strategies

- Backdoor Roth IRA: High-income earners can contribute to a Traditional IRA and convert to a Roth IRA, enabling tax-free growth later.

- Rebalancing: Periodically adjusting your portfolio ensures your investments align with risk tolerance and retirement goals.

- Integrating multiple accounts: Coordinating IRA contributions with 401(k)s and Roth IRAs can optimize long-term tax efficiency.

Comparing Traditional IRAs with Other Accounts

- 401(k): Employer-sponsored, often with matching contributions and higher limits.

- Roth IRA: Contributions are after-tax, but withdrawals are tax-free.

Many investors use both Traditional and Roth accounts to create a tax-diverse retirement strategy, reducing risk and optimizing tax outcomes.

Common Myths About Traditional IRAs

- “Only for people without a 401(k).” False — you can contribute to both.

- “You can only have one IRA.” False — you can hold multiple IRAs, though annual contributions are capped.

- “Withdrawals are always penalized.” False — there are exceptions for first-time home purchases, education, and medical expenses.

Planning for Retirement

A Traditional IRA is just one piece of a comprehensive retirement strategy. Other sources of retirement income may include:

- Social Security benefits

- Employer-sponsored plans (401(k), 403(b))

- Personal savings and brokerage accounts

Combining these sources allows for a diversified income strategy that balances risk, taxes, and growth potential.

Example: Integrated Retirement Strategy

Susan, age 35, contributes $6,000 per year to her Traditional IRA, $10,000 to her 401(k), and $2,000 to a taxable brokerage account. This diversified strategy:

- Reduces taxable income today via the Traditional IRA and 401(k)

- Offers tax-free growth potential later via a Roth conversion strategy

- Provides flexibility in early retirement via taxable accounts

Over decades, this approach can help her manage taxes and maintain cash flow flexibility, maximizing long-term retirement security.

Final Thoughts

A Traditional IRA is a versatile, tax-advantaged tool for retirement planning. By combining consistent contributions, tax-deferred growth, and strategic withdrawal planning, almost any worker can build a meaningful retirement fund.

Key takeaways for novice investors:

- Start early — even modest contributions compound significantly over time.

- Maximize contributions within IRS limits.

- Diversify your investments to balance growth and risk.

- Understand withdrawals and plan for taxes.

- Integrate IRAs with other retirement accounts for a tax-efficient strategy.

Whether you are 22 or 52, a Traditional IRA offers the opportunity to grow your savings more effectively than taxable accounts alone, providing both financial security and peace of mind.

{kind=link}