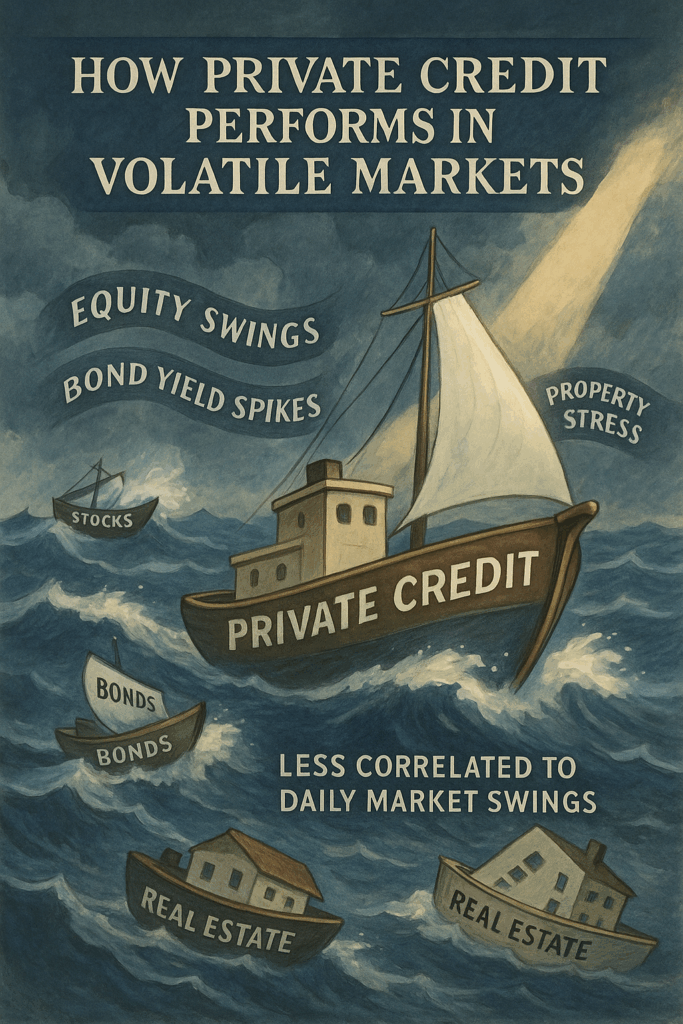

Periods of volatility are when an investment strategy is truly tested. Equity markets can swing 10% in a month, bond yields can spike in days, and even supposedly “safe” assets like real estate can feel pressure. For investors, these times often reveal which parts of their portfolio are resilient—and which are vulnerable.

One asset class that has drawn increasing attention during market turbulence is private credit. By definition, private credit refers to non-bank lending to businesses and projects outside of the traditional public debt markets. These loans are negotiated privately, typically between institutional investors or private credit funds and borrowers. The lack of public trading means private credit is less exposed to daily market swings. But does that mean it performs well during volatility? Let’s dig deeper.

Why Volatile Markets Create Opportunity for Private Credit

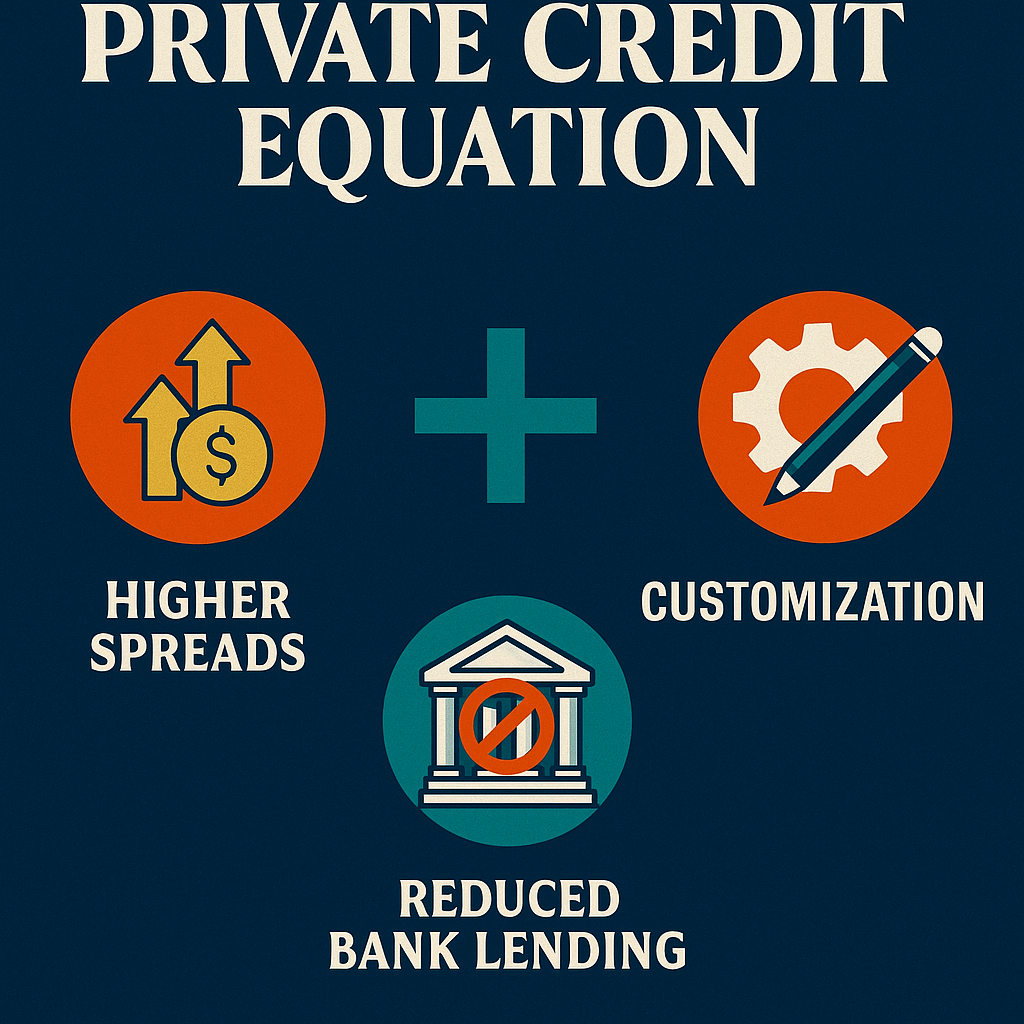

When public markets are unstable, banks and bond investors often pull back, making it harder for companies to access financing. This “funding gap” creates opportunity for private lenders.

- Reduced Bank Lending: After the 2008 financial crisis and again during the COVID-19 downturn, banks tightened lending standards. Private credit funds stepped in, offering loans where traditional institutions hesitated.

- Higher Spreads: With uncertainty high, borrowers are often willing to pay a premium for reliable access to capital. This translates into higher yields for private credit investors.

- Customization: Unlike standardized bonds, private loans can be structured with flexible terms to match both borrower needs and investor protections. This flexibility is particularly valuable during uncertain times.

In short, volatility often drives demand for private credit rather than diminishing it.

The Cushion of Floating-Rate Structures

One of private credit’s strengths in volatile environments is the prevalence of floating-rate loans. Many loans are tied to benchmarks like SOFR (Secured Overnight Financing Rate) plus a spread. When interest rates rise—often in response to inflation or market stress—private credit investors see higher yields.

In contrast, public fixed-rate bonds lose value when rates rise because their coupons don’t adjust. This dynamic makes private credit relatively resilient in interest-rate-driven volatility.

Illiquidity: A Double-Edged Sword

Private credit is not traded on exchanges. While this means its valuations don’t swing with the same visible volatility as public markets, it also means investors can’t easily exit positions.

- Stability Advantage: Because private loans are not marked-to-market daily, investors are spared the psychological impact of watching values whipsaw. This can lead to steadier reported returns in a portfolio.

- Liquidity Drawback: On the flip side, investors who suddenly need cash won’t find private credit as flexible. Lock-up periods can last several years, making it critical for investors to allocate only capital they can keep committed long term.

During volatile periods, the illiquidity premium is often seen as a trade-off worth accepting—so long as investors plan appropriately.

Risk Management in Private Credit

Private credit isn’t risk-free. Defaults can rise during economic downturns, especially in cyclical industries. However, private credit managers often take proactive steps to mitigate risks:

- Stronger Covenants: Many private loans include protective covenants requiring borrowers to meet certain financial benchmarks. This gives lenders early warning signs and leverage in negotiations.

- Collateralization: Loans are often secured against assets, such as real estate, equipment, or receivables. In the event of default, this collateral can help protect investors’ capital.

- Active Monitoring: Unlike bondholders in large public issuances, private lenders are often in close contact with management teams, receiving detailed reporting and sometimes board representation.

This hands-on approach can provide an additional layer of defense during volatile markets compared to passive exposure in public bonds.

Historical Performance During Volatility

Looking at recent history provides useful insights:

- Global Financial Crisis (2008–2009): While many leveraged loans in the syndicated loan market suffered, private credit managers who focused on middle-market lending generally outperformed public debt benchmarks. Their ability to negotiate terms and work directly with borrowers helped mitigate losses.

- COVID-19 Pandemic (2020): When markets froze in March 2020, private credit funds initially faced concerns about defaults. However, many loans performed well thanks to sector diversification, covenant protections, and the fact that companies were highly motivated to maintain private lending relationships. By late 2020, fundraising for private credit had surged as investors sought yield and stability.

- Rising Rates (2022–2023): With central banks hiking interest rates aggressively, many bond markets posted negative returns. Meanwhile, floating-rate private loans adjusted upward, providing attractive income streams and protecting investors from rate-driven losses.

These episodes suggest that private credit can be more resilient than public debt in turbulent times, though outcomes depend heavily on manager quality and borrower selection.

Comparing to Public Debt

In volatile markets, public debt often suffers from both price volatility and liquidity challenges. Bond ETFs, for instance, can trade at discounts to net asset value when markets are stressed.

Private credit, while less liquid, doesn’t face daily repricing pressure. For long-term investors, this can mean steadier returns and less correlation with equity market swings. However, the trade-off is opacity—valuations are estimated periodically, and investors must rely on fund managers’ reporting.

The Bottom Line for Investors

Private credit is not immune to volatility, but it tends to be less reactive and often more opportunistic during market stress. The combination of floating rates, negotiated protections, and direct borrower relationships gives it resilience that traditional public debt may lack.

That said, performance hinges on manager selection. Inexperienced lenders, poor underwriting, or concentration in vulnerable industries can expose investors to higher losses during downturns. For those considering allocations, due diligence is critical.

Ultimately, private credit’s relative stability and income potential make it a valuable diversifier in volatile markets—but only for investors prepared to accept its illiquidity and complexity.

{kind=link}