Planning for retirement can feel overwhelming. Between 401(k)s, pensions, Social Security, and brokerage accounts, the alphabet soup of financial terms often leaves new investors more confused than confident. But one tool stands out as both approachable and powerful: the Individual Retirement Account, better known as an IRA.

An IRA isn’t just a place to stash money. It’s a tax-advantaged account designed to help you save for your future in a way that regular savings or brokerage accounts can’t match. Whether you’re early in your career, starting a side hustle, or already in midlife and playing catch-up, understanding how IRAs work is one of the most important steps you can take toward financial independence.

This guide will break down what an IRA is, the different types, how contributions work, the tax benefits, and what you need to know to make the most of one.

IRA Basics: What Exactly Is an IRA?

At its core, an IRA is a special type of investment account that comes with tax benefits. The U.S. government introduced IRAs in 1974 as part of the Employee Retirement Income Security Act (ERISA) to encourage people to save for retirement outside of their workplace. While employer-sponsored plans like 401(k)s dominate retirement savings for many workers, IRAs provide flexibility for anyone with earned income — even if you’re self-employed or don’t have access to a retirement plan at work.

Here are the essentials:

- IRA stands for Individual Retirement Account. The “individual” part is key — unlike a 401(k), an IRA is set up and controlled by you, not your employer.

- You can open one at most major financial institutions: banks, brokerages, mutual fund companies, or online investing platforms.

- You fund it with money you earn from work (wages, salaries, self-employment income). Investment income, rental income, or gifts don’t count.

- Once funded, you can invest in a wide range of assets: stocks, bonds, ETFs, mutual funds, CDs, and sometimes even alternative investments like real estate (through specialized self-directed IRAs).

The tax advantages of IRAs are what make them so powerful. Depending on the type of IRA, your contributions might be tax-deductible, your money may grow tax-deferred, or your withdrawals in retirement could even be tax-free.

Why IRAs Matter

If you’re new to investing, you might be wondering: Why bother with an IRA when I can just invest in a regular brokerage account?

The answer lies in tax treatment. In a regular brokerage account, you’ll pay taxes every year on dividends, interest, and any gains you realize when you sell investments. In an IRA, the government offers a trade-off: you commit to using the money for retirement, and in return, your investments either grow tax-deferred (you pay taxes later) or tax-free (you never pay taxes on growth, depending on the IRA type).

That difference can be massive. Consider two investors, Alex and Jordan, who each invest $6,000 annually for 30 years and earn an average return of 7%:

- Alex invests in a taxable account. By the end, after paying annual taxes on gains and income, their balance is significantly reduced.

- Jordan invests in an IRA. Because taxes are deferred (or eliminated in a Roth), Jordan’s account compounds more efficiently, often leaving them with tens of thousands more for retirement.

Simply put: IRAs supercharge compounding by letting your money grow without being chipped away by yearly taxes.

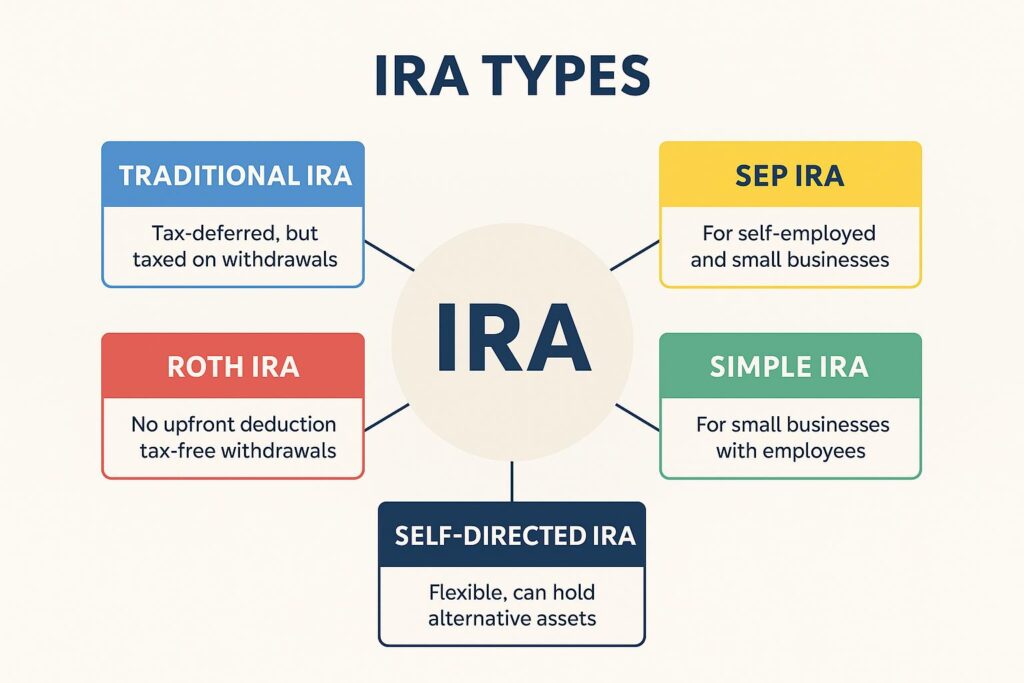

The Main Types of IRAs

There isn’t just one kind of IRA — the rules, benefits, and eligibility vary depending on which type you choose. Here are the most common ones:

1. Traditional IRA

- Tax treatment: Contributions may be deductible, reducing your taxable income in the year you contribute. The money then grows tax-deferred until you withdraw it in retirement, at which point it’s taxed as ordinary income.

- Best for: People who want a tax break now and expect to be in the same or lower tax bracket when they retire.

2. Roth IRA

- Tax treatment: Contributions are made with after-tax dollars (no immediate deduction), but withdrawals in retirement are completely tax-free, including investment gains.

- Best for: People who expect to be in a higher tax bracket later, or who want to lock in tax-free income in retirement.

- Withdrawal rules: Contributions can be withdrawn at any time, tax- and penalty-free. Earnings, however, generally require that the account be at least five years old and the owner be 59½ or older (or meet another qualified exception) to be withdrawn tax-free.

3. SEP IRA (Simplified Employee Pension)

- Who it’s for: Self-employed people or small business owners.

- How it works: Contributions are made by the employer (which can be you, if you’re self-employed). They can be up to 25% of compensation, subject to an annual dollar limit. This makes it a powerful tool for entrepreneurs.

4. SIMPLE IRA (Savings Incentive Match Plan for Employees)

- Who it’s for: Small businesses with generally 100 or fewer employees who earned at least $5,000 in the prior year.

- How it works: Employers are required to make contributions, either through matching or fixed contributions for each eligible employee.

5. Self-Directed IRA

- What it offers: Greater flexibility. Investors can hold alternative assets like real estate, private equity, or precious metals.

- Caution: These accounts come with higher risks, more fees, and stricter IRS rules. Mistakes can trigger penalties.

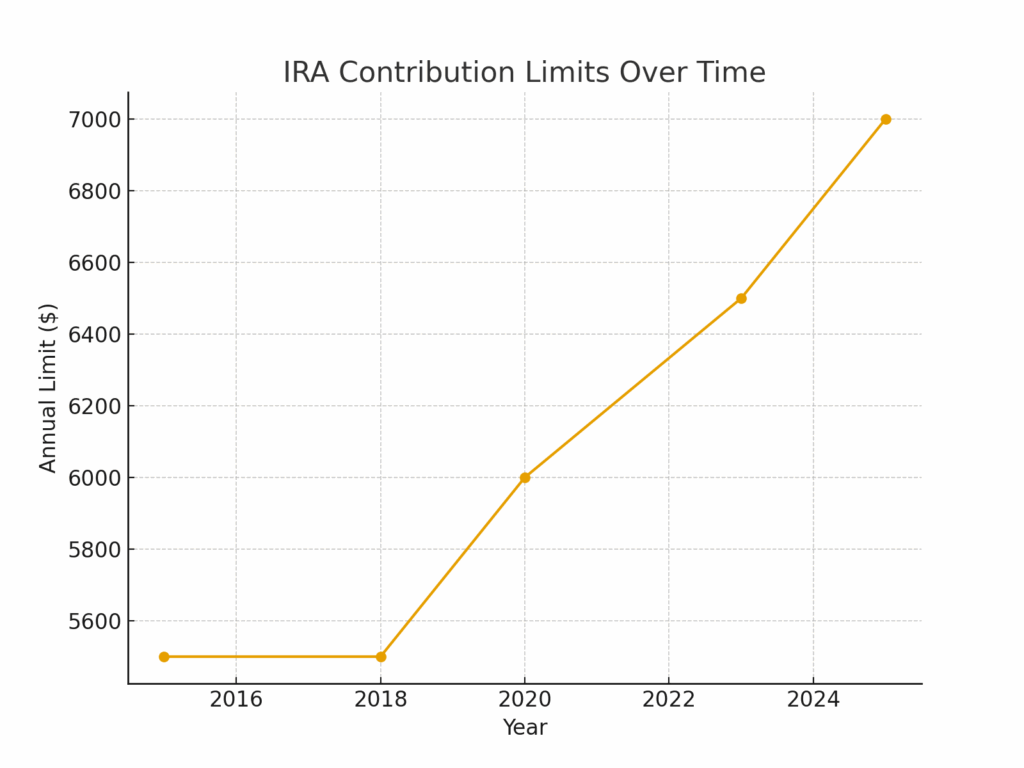

Contribution Rules

Each year, the IRS sets limits on how much you can contribute to an IRA. These rules exist to prevent IRAs from becoming unlimited tax shelters.

- For 2025, individuals can contribute up to $7,000 per year (or $8,000 if you’re age 50 or older, thanks to “catch-up” contributions). These limits are set annually by the IRS and may be adjusted for inflation.

- You must have earned income equal to or greater than your contribution amount (or, if less, your taxable compensation).

- Contributions usually must be made by the tax-filing deadline (typically April 15 of the following year).

Income also plays a role: high earners may face limits on whether they can deduct traditional IRA contributions or contribute directly to a Roth IRA. Still, there are strategies like the “backdoor Roth IRA” that advanced investors sometimes use to work around these limits. This strategy is legal but requires careful tax reporting (Form 8606) and can create complications if you have other pre-tax IRA balances.

Withdrawals and Penalties

The tax benefits of IRAs come with strings attached. The government doesn’t want you treating an IRA like a regular checking account.

- Early withdrawals: If you take money out of a traditional IRA before age 59½, you’ll generally owe both income tax and a 10% penalty.

- Exceptions: Certain expenses, like first-time home purchases (up to $10,000), qualified education costs, or certain medical expenses, can qualify for penalty-free withdrawals.

- Required Minimum Distributions (RMDs): As of current law, RMDs for most traditional IRAs begin at age 73(this change took effect in 2023). Future law raises the starting age to 75 for later cohorts, so the exact start age depends on your birth year. Roth IRAs, however, do not require RMDs during your lifetime, making them a valuable estate-planning tool.

Investment Options Inside an IRA

An IRA is just the account — what really matters is what you put inside it. Think of it like a suitcase: the tax benefits come from the suitcase itself, but the contents (stocks, bonds, funds, etc.) determine how your money grows.

Most IRA providers offer access to:

- Stocks: Individual company shares. Higher risk, higher reward.

- Bonds: More stable, income-focused investments.

- Mutual funds and ETFs: Diversified baskets of investments, often a solid choice for beginners.

- Target-date funds: Prebuilt funds that automatically adjust their mix of investments as you approach retirement.

For most novice investors, a mix of low-cost index funds or target-date funds inside an IRA offers a balance of simplicity and long-term growth potential.

Tax Benefits in Action

To see the impact of an IRA’s tax perks, let’s compare two scenarios:

- Scenario A: Regular brokerage account. You invest $6,000 per year for 30 years with a 7% return. Because of taxes on dividends and capital gains, you might end up with around $510,000.

- Scenario B: IRA account. Same contributions and returns, but with tax-deferred or tax-free growth. You could have closer to $610,000 by retirement.

That $100,000 difference doesn’t come from investing more — it comes from avoiding the yearly tax drag.

Common Misconceptions About IRAs

Because IRAs can seem complex, plenty of myths swirl around them:

- “IRAs are only for people without a 401(k).” Not true — you can contribute to both, though your ability to deduct contributions may be limited if you have a 401(k).

- “You can only have one IRA.” Also false — you can have multiple IRAs (traditional, Roth, SEP, etc.), though your combined annual contributions can’t exceed the yearly limit.

- “IRAs lock up your money until retirement.” Mostly true, but there are penalty-free exceptions for certain expenses. Plus, Roth contributions (but not earnings) can be withdrawn at any time without penalty.

How to Open an IRA

Getting started is easier than most people think. The process usually looks like this:

- Choose a provider – Banks, brokerage firms, or online investment platforms. Look for low fees and strong customer support.

- Decide on account type – Traditional or Roth are the most common starting points.

- Fund the account – Transfer money from your bank or roll over funds from another retirement account.

- Pick investments – Select stocks, funds, or other assets that fit your long-term goals.

- Set up contributions – Automate deposits monthly or yearly to stay on track.

The Role of IRAs in a Bigger Retirement Plan

An IRA is a powerful piece of the puzzle, but it’s rarely the whole picture. For most savers, retirement income will come from a mix of:

- Social Security

- Employer plans (401(k), 403(b), etc.)

- IRAs

- Personal savings or taxable investment accounts

The beauty of an IRA is its flexibility. You don’t need an employer to sponsor it, you control the investments, and you can tailor contributions to your situation. Over decades, even modest contributions add up in surprising ways.

Final Thoughts

An IRA may sound like just another financial acronym, but in practice, it’s one of the simplest and most effective tools for building wealth over time. By combining tax advantages with investment flexibility, IRAs give everyday investors a fighting chance to retire comfortably — even without a hefty paycheck or an employer-sponsored plan.

Whether you’re 22 and just opening your first account, or 52 and looking to maximize catch-up contributions, the principles are the same: start early if you can, contribute regularly, and let time and compounding do their work.

In the end, an IRA isn’t just an account. It’s a commitment to your future self — a way to ensure that when retirement comes, you have the freedom and security you deserve.

{kind=link}