This Content Is Only For Subscribers

Private credit has quietly become one of the most significant shifts in modern finance. Once a niche corner of alternative investments, it is now a trillion-dollar market reshaping how companies borrow, how institutions allocate capital, and how investors think about risk and return.

In today’s investing landscape, private credit is no longer a supporting act—it’s a headliner. From middle-market lending to distressed debt, the sector has captured global attention and capital. But what is driving its growth, and what should investors watch for as the market evolves?

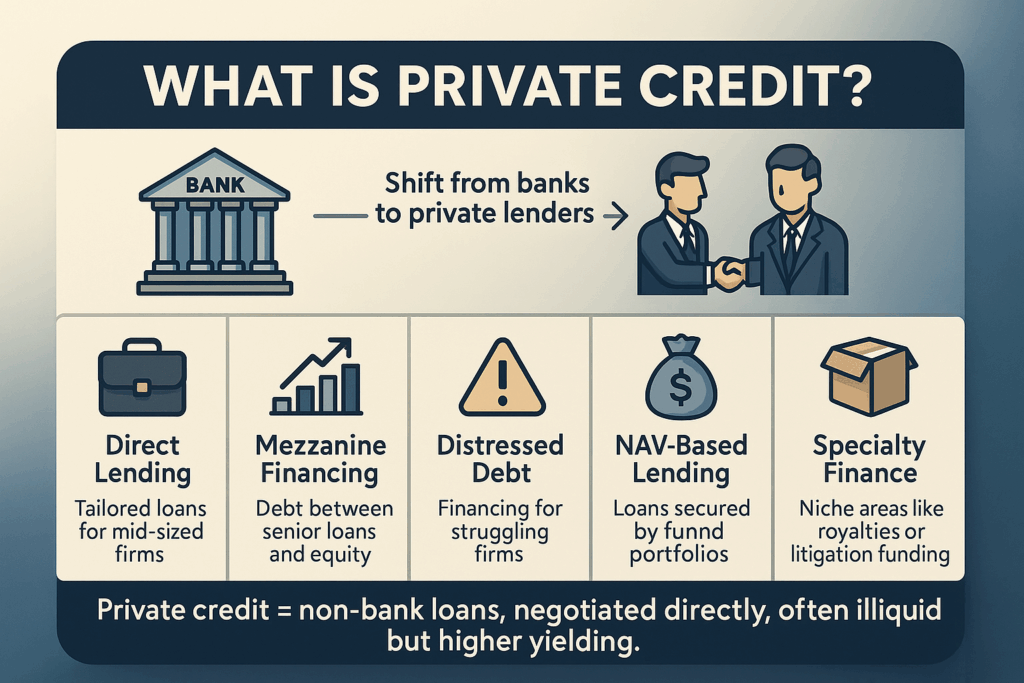

What Is Private Credit?

At its simplest, private credit refers to loans and debt financing provided by non-bank institutions, such as private funds, rather than traditional banks. It encompasses:

- Direct lending – customized loans to mid-sized companies, often with flexible terms.

- Mezzanine financing – subordinated debt that sits between senior loans and equity.

- Distressed debt – opportunities to lend to or invest in companies under financial stress.

- NAV-based financing – loans made against the value of a fund’s private equity portfolio, a fast-growing niche.

- Specialty finance – niche areas like litigation funding, royalties, trade finance, or equipment leasing.

Unlike public bonds or syndicated loans, private credit transactions are negotiated directly and are typically illiquid. That illiquidity comes with higher yields—one of the key attractions for investors.

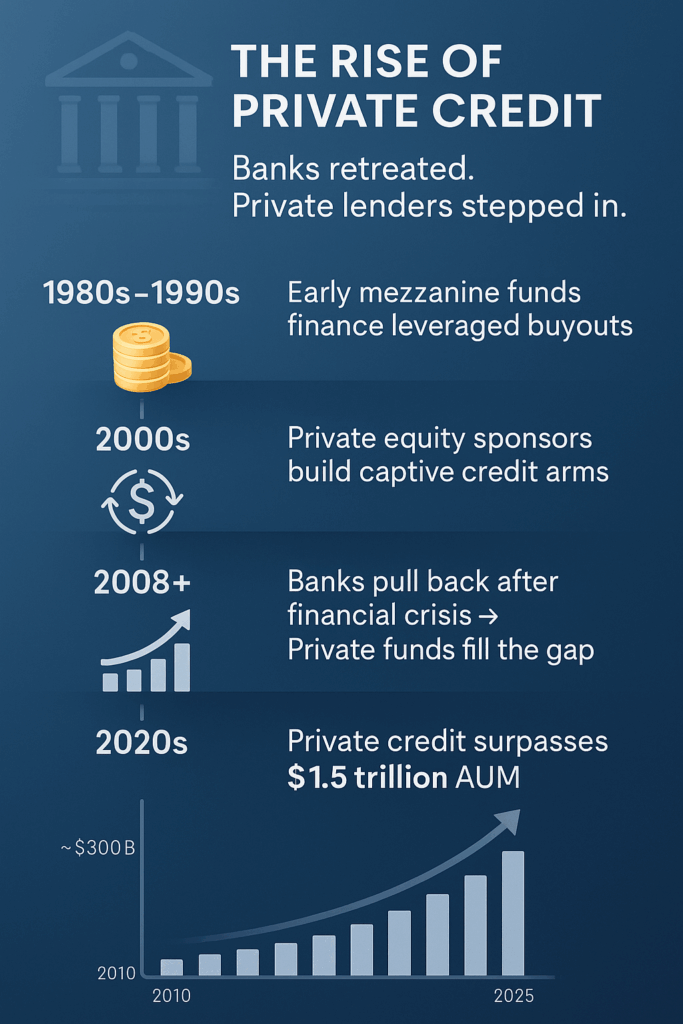

The Origins: Before and After 2008

Though private credit surged after the global financial crisis, its roots go back further.

- 1980s–1990s: Early mezzanine funds emerged to finance leveraged buyouts. Insurance companies and private partnerships provided subordinated debt alongside bank loans.

- 2000s: Private equity sponsors began building captive credit arms, seeing synergies between buyouts and debt financing.

- Post-2008: The financial crisis and regulatory reforms (Basel III, Dodd-Frank) fundamentally reshaped bank lending. Banks reduced risk appetite and balance-sheet exposure, particularly to mid-market and leveraged borrowers. Private funds stepped in to fill the vacuum.

From less than $300 billion in 2010, private credit assets under management swelled to more than $1.5 trillion by the mid-2020s. That growth has made private credit the third pillar of private markets, alongside private equity and real estate.

Why Private Credit Is Growing

1. The Search for Yield

During the decade of near-zero rates after 2008, pension funds, endowments, and insurers hunted for alternatives to government bonds. Private credit provided yields in the 6–12% range, attractive compared to 1–3% on traditional fixed income.

2. Flexibility for Borrowers

Private lenders can move faster and offer tailored structures. For a mid-sized company seeking a customized facility, private credit is often more practical than navigating the slower, standardized bank process.

3. Regulation and Bank Retreat

Post-crisis rules increased capital requirements for banks, discouraging them from holding leveraged loans. Non-bank lenders, less regulated, stepped in to serve the same borrowers.

4. Institutionalization of Alternatives

The rise of alternatives as a mainstream allocation—driven by endowments like Yale and mega-pensions—made private credit a natural extension. It fits between traditional fixed income and private equity, offering a blend of steady income and alternative risk premia.

5. Relationship to Private Equity

Private equity sponsors often prefer private credit lenders, who can execute quickly and offer larger, bespoke loans. This synergy has reinforced the rise of sponsor-backed lending, where private equity firms rely heavily on private credit to finance buyouts.

Key Trends Shaping the Market

Institutional Capital Floods In

Large pensions, sovereign wealth funds, and insurers are committing billions. In some cases, private credit allocations now approach 10–15% of total assets.

- Example: CalPERS and Canadian pensions have steadily increased private credit allocations since 2015, citing attractive risk-adjusted returns.

Mega-Funds vs. Specialists

A few global giants—Ares, Apollo, Blackstone, KKR—dominate large direct lending. But specialist managers are thriving in niches like healthcare lending, NAV loans, and emerging markets.

- Implication: Larger deals are concentrated among mega-funds, while smaller managers compete on specialization and agility.

Rise of Unitranche Lending

Unitranche structures, blending senior and subordinated debt into one facility, simplify financing for borrowers and deliver attractive pricing for lenders. These have become standard in sponsor-backed deals above $100 million.

Globalization of Private Credit

The U.S. accounts for more than two-thirds of the market, but Europe is growing rapidly. In Asia-Pacific, Japan, Australia, India, and Southeast Asia are seeing increasing institutional activity.

- Europe: Regulatory frameworks and bank conservatism are opening space for private funds.

- Asia: Still nascent, but rising demand for alternative credit to support growth companies.

Technology and Transparency

Private credit was once criticized as opaque. Now, technology platforms aggregate data on loan pricing and portfolio performance, while AI tools assist in underwriting and portfolio monitoring.

Regulatory Spotlight

With growth comes scrutiny. Regulators in the U.S. and EU are increasingly monitoring leverage levels, interconnectedness with banks, and systemic risks.

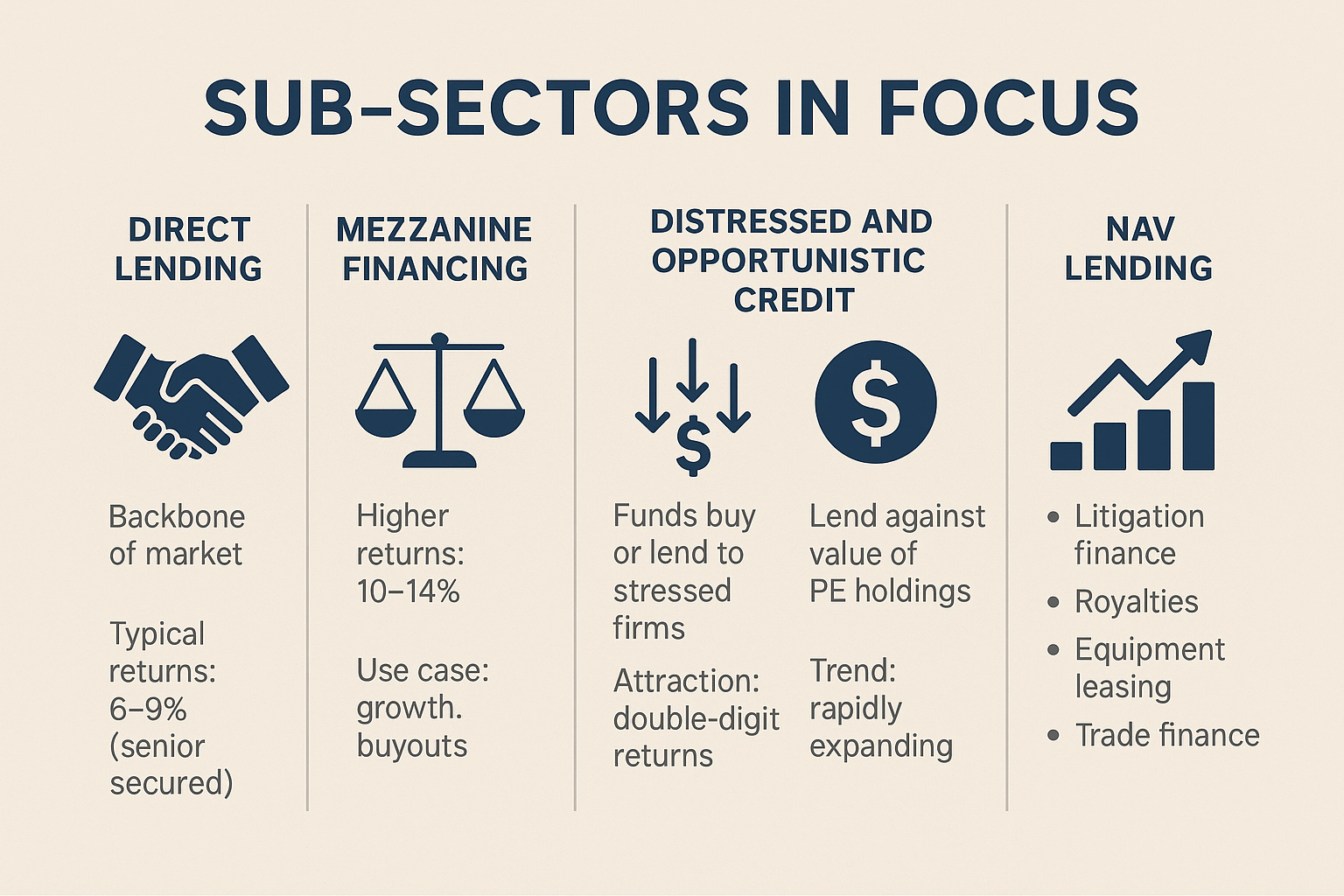

Sub-Sectors in Focus

1. Direct Lending

The backbone of the market. Mid-market companies use direct loans for acquisitions, growth, or refinancing.

- Typical returns: 6–9% (senior secured).

- Trend: Loans are often floating rate, making them attractive during rising-rate environments.

2. Mezzanine Financing

Provides higher returns (10–14%) but sits lower in the capital structure.

- Use case: Growth financings or buyouts where equity sponsors want to minimize dilution.

3. Distressed and Opportunistic Credit

Funds buy debt at discounts or lend to stressed borrowers.

- Attraction: Double-digit returns in dislocation cycles.

- Risk: Dependent on recovery rates and legal outcomes.

4. NAV Lending

A growing trend where credit funds lend against the net asset value of private equity portfolios.

- Why it matters: Helps PE sponsors provide liquidity to investors without selling assets prematurely.

- Trend: Rapidly expanding as PE seeks more flexible financing options.

5. Specialty Finance

Niche areas outside corporate lending:

- Litigation finance.

- Royalties in music or pharmaceuticals.

- Equipment leasing.

- Trade finance.

These offer uncorrelated cash flows and diversification.

Global Perspectives

United States

The largest and most mature private credit market. U.S. direct lending funds dominate deal volumes, and many sponsor-led buyouts are financed entirely by private credit clubs.

Europe

European private credit is growing fast, especially in the UK, France, and Germany. Regulatory capital requirements have made European banks conservative, leaving space for private lenders.

- Trend: ESG integration is particularly strong in Europe, with credit funds emphasizing sustainable lending.

Asia-Pacific

Still early but with immense potential. Japan’s institutional investors are deploying into private credit, while India and Southeast Asia present growth markets. Australia has seen strong fund launches focused on infrastructure and corporate lending.

Emerging Markets

Latin America and Africa offer high-yield opportunities but carry governance, political, and currency risks. Institutional appetite is cautious but rising.

Opportunities in Private Credit

- Sponsor-Backed Lending: Synergy with private equity ensures deal flow.

- Floating-Rate Income: Attractive in inflationary/rising-rate cycles.

- Global Diversification: Expanding opportunities in Europe and Asia.

- Niche Strategies: NAV loans, litigation finance, royalties.

- Dislocation Plays: Volatile markets often present distressed opportunities.

Risks Investors Must Watch

- Credit Risk: Defaults and restructurings can erode returns.

- Illiquidity: 5–10 year lockups typical; few secondary options.

- Crowding: More capital could push yields lower.

- Economic Cycles: A prolonged recession would test portfolio resilience.

- Regulation: Increased oversight could change market dynamics.

Case Examples

- Apollo & AT&T (2021): Apollo provided multi-billion-dollar financing to carve-out AT&T’s media assets, showing how mega-funds can replace bank syndicates.

- Mid-market U.S. Manufacturing Firm (2022): Received a $300M unitranche loan from a private credit club, replacing traditional bank debt.

- European Green Financing (2023): Ares financed a renewable energy developer in Spain, tying loan pricing to ESG performance metrics.

Evaluating Private Credit Funds (For Investors)

When allocating, investors should consider:

- Manager Track Record: Experience across cycles matters.

- Diversification: Sector, geography, and borrower concentration.

- Leverage Use: Some funds borrow at the fund level; higher leverage = higher risk.

- Fee Structures: Typically 1–1.5% management fee + 10–15% carry above hurdle.

- Liquidity Options: Closed-end funds dominate, but evergreen funds are emerging.

Looking Ahead: Scenarios

Optimistic Scenario

- Moderate economic growth.

- Continued demand for flexible, non-bank lending.

- Stable default rates (2–3%).

- Institutional allocations grow to 15–20%.

Bearish Scenario

- Deep recession.

- Default rates rise significantly (6–10%).

- Returns fall short, exposing weak underwriting.

- Regulatory clampdowns constrain growth.

Base Case

- Steady growth, with cyclical challenges.

- More competition but also more innovation.

- Continued global expansion, especially in Europe and Asia.

Lessons for Novice Investors

- Yield has a price. Higher returns mean higher risks.

- Diversification is key. Spread across managers and strategies.

- Cycles matter. Beware chasing peak-cycle deals.

- Manager selection drives outcomes. The gap between top- and bottom-quartile funds is wide.

Final Thoughts

Private credit has transformed from a post-crisis patch to a permanent fixture of global finance. It offers yield, diversification, and flexibility—but also carries risks tied to cycles, competition, and regulation.

For investors, the private credit market represents both opportunity and challenge. Those who approach it with discipline and long-term perspective may find it a powerful tool in portfolio construction. Those who chase yield without caution may find it less forgiving.

Either way, one thing is clear: private credit is no longer private—it’s reshaping the financial system for everyone.

{kind=link}