This Content Is Only For Subscribers

When you hear the words hedge fund, you might picture a secretive group of elite financiers, whispering behind closed doors about billion-dollar trades. For many, hedge funds feel mysterious—complicated vehicles that only the ultra-wealthy can access. While there’s some truth to their exclusivity, hedge funds aren’t as impenetrable as they seem. At their core, they’re simply investment partnerships with a particular way of organizing money, people, and incentives.

If you’re a novice investor, understanding how hedge funds are structured can help demystify them. Whether you ever invest in one or just want to sharpen your financial literacy, knowing who runs these funds, how they’re compensated, and what motivates them is key to understanding their place in the broader financial world.

In this article, we’ll break down the fundamental structure of hedge funds—covering fees, managers, and incentives—so you can see what makes them tick.

What Exactly Is a Hedge Fund?

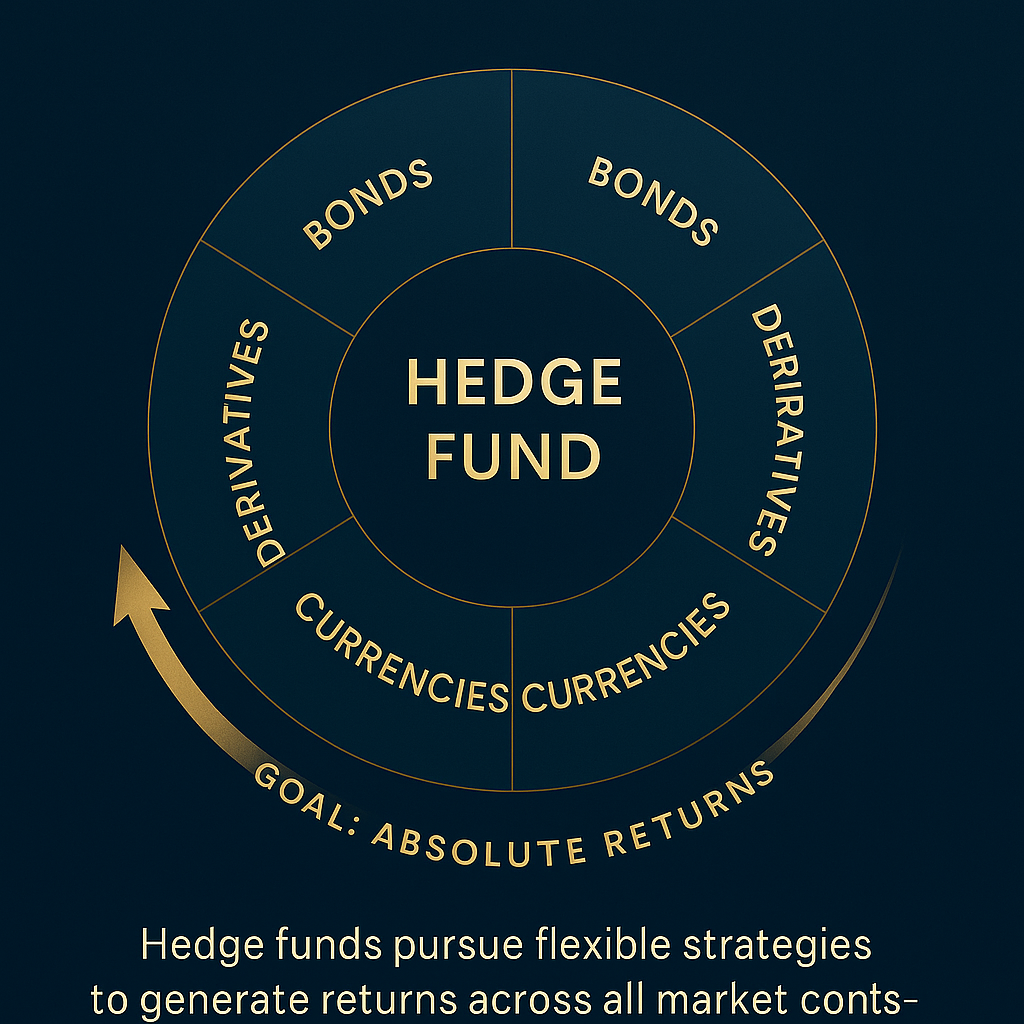

A hedge fund is a pooled investment vehicle, similar in spirit to a mutual fund or exchange-traded fund (ETF). Investors contribute money, which is then managed collectively according to the fund’s strategy. Unlike mutual funds or ETFs, however, hedge funds operate with far more flexibility. They can invest in stocks, bonds, derivatives, commodities, currencies, and sometimes even private companies or real estate.

The term hedge fund comes from the early days of the industry, when managers often “hedged” their positions—buying some assets long (betting they would rise in value) and selling others short (betting they would fall). Today, not all hedge funds actually hedge. Instead, the term has become shorthand for an investment partnership that uses creative or aggressive strategies, often with the goal of generating “absolute returns” regardless of whether the market is going up or down.

But hedge funds are not open to everyone. In the U.S., for example, investors typically must qualify as “accredited” (meaning they have a certain income or net worth) to invest. This gatekeeping reflects both the risks involved and the sophisticated nature of the strategies used.

The Basic Legal Structure

At their foundation, most hedge funds are set up as limited partnerships (LPs) or limited liability companies (LLCs). Here’s what that means:

- General Partner (GP): This is the hedge fund manager or management company. The GP runs the fund, makes investment decisions, and shoulders most of the operational responsibility.

- Limited Partners (LPs): These are the investors—institutions, pension funds, wealthy individuals, or family offices—who provide the capital. As limited partners, their liability is restricted to the money they invest.

This partnership structure is intentional. It allows investors to pool money without being involved in day-to-day management, while giving the manager authority to pursue the fund’s strategy. In many ways, it mirrors a business startup: the GP is the entrepreneur, and the LPs are the backers.

The Fee Structure: How Hedge Funds Get Paid

One of the defining features of hedge funds is their fee structure. Unlike mutual funds, which usually charge a simple percentage of assets under management (AUM), hedge funds traditionally use a “2 and 20” model:

- Management Fee (the “2”): This is typically around 2% of the fund’s AUM, charged annually. It helps cover salaries, rent, research, technology, and other operational costs. Even if the fund loses money, the manager still collects this fee.

- Performance Fee (the “20”): This is usually 20% of the profits earned for investors. If the fund makes money, the manager shares directly in that upside.

This structure is designed to align the manager’s incentives with those of investors. The manager benefits when investors benefit, at least in theory.

Of course, fees vary. Some funds may charge 1.5% and 15%, or even less, especially as investors have pushed back against high costs in recent years. Larger funds or those with strong reputations may still command the traditional 2 and 20. The balance between fees and performance is one of the ongoing debates in the hedge fund industry.

High-Water Marks and Hurdle Rates

To make performance fees fairer, many hedge funds use mechanisms like:

- High-Water Mark: A rule stating that the manager only earns performance fees on profits above the fund’s previous peak value. This prevents managers from collecting fees twice for recovering from a loss.

- Hurdle Rate: A minimum rate of return (say, 5%) that the fund must exceed before charging performance fees. This ensures managers only profit if investors earn a meaningful return.

These details might sound technical, but they matter. They influence how managers take risks, how investors judge performance, and how long investors stick around when returns are bumpy.

The Role of the Hedge Fund Manager

The hedge fund manager is the central figure in the structure. Often, the manager is also the founder and public face of the fund. Investors typically choose hedge funds not just based on the strategy, but on their confidence in the manager’s skill, discipline, and judgment.

Managers wear several hats:

- Investment Decision-Maker: They design and execute the fund’s strategy—choosing investments, managing risk, and adjusting positions.

- Business Operator: They oversee the organization itself, hiring analysts, traders, compliance officers, and support staff.

- Marketer and Fundraiser: They pitch to potential investors, maintain relationships, and build the fund’s reputation.

It’s an intense role. Some managers become celebrities in the financial world, known for their bold calls or outsize personalities. Others stay behind the scenes, quietly compounding wealth for their clients.

The Investment Committee

While the manager is often the star, many hedge funds operate with an investment committee. This group—sometimes just a few senior professionals, sometimes a larger team—reviews strategies, debates risks, and signs off on major decisions.

The committee helps balance the manager’s vision with collective oversight. It also signals to investors that the fund’s process isn’t a one-person show. At large funds, the committee might resemble a corporate boardroom, complete with formal voting. At smaller funds, it may be more of a collaborative discussion.

Incentives and Alignment of Interests

Why do hedge funds use such elaborate fee structures and governance systems? The answer lies in incentives.

For hedge funds to succeed, the interests of managers and investors need to be aligned. If managers earned only a flat salary, they might lack motivation to chase strong returns. If they earned only performance fees, they might take reckless risks. The mix of management and performance fees is designed to strike a balance: stability for the fund’s operations plus upside for strong performance.

Still, conflicts can arise. For example, a manager might be tempted to take big risks to earn performance fees, especially if they’re already earning steady management fees. That’s why structures like high-water marks and independent risk teams are so important.

Investors also look for “skin in the game”—when managers invest their own money in the fund. If the manager is risking their own wealth alongside investors, it’s a strong sign their incentives are aligned.

Beyond the Basics: Service Providers and Infrastructure

Hedge funds don’t operate in a vacuum. They rely on a web of service providers to function:

- Prime Brokers: Large banks that provide financing, securities lending, and trade execution.

- Administrators: Independent firms that handle accounting, valuation, and investor reporting.

- Auditors: External firms that verify financial statements.

- Lawyers and Compliance Experts: Professionals who ensure the fund follows regulations.

This infrastructure may not make headlines, but it’s essential. It provides credibility and transparency to investors, while freeing the manager to focus on strategy.

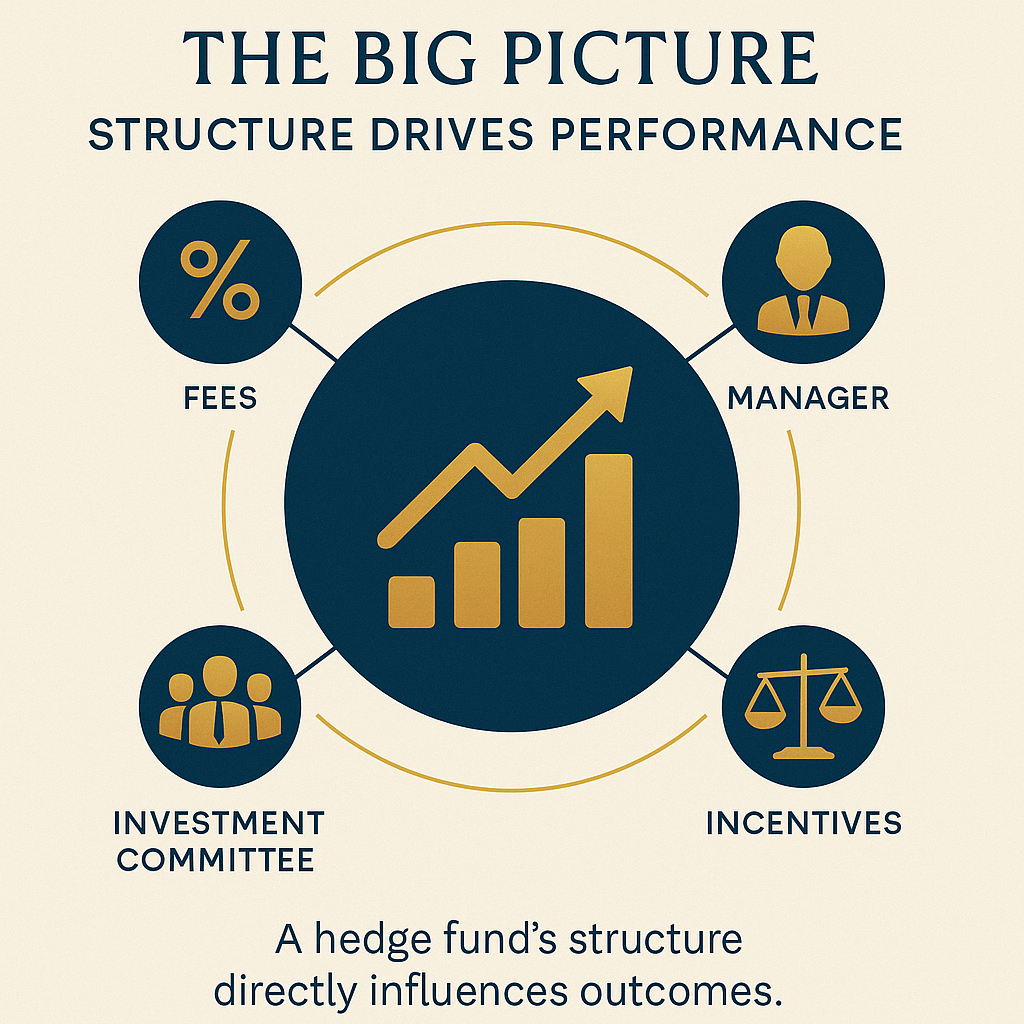

Why Structure Matters to Investors

For novice investors, hedge fund structures might seem like inside baseball. But they matter more than you think. The way fees are set, the way managers are incentivized, and the way oversight works all affect the kinds of returns investors can expect.

Consider two funds with similar strategies: one charges high fees but has a disciplined manager with significant personal capital invested; the other charges low fees but has weak oversight and no high-water mark. Which would you trust more? Understanding structure helps you make that judgment.

The Evolution of Hedge Fund Structures

The hedge fund industry has evolved dramatically over the past few decades. In the 1980s and 1990s, hedge funds were small, nimble, and often operated by a single star manager. Today, many have grown into multi-billion-dollar institutions with hundreds of employees.

This growth has led to more formalized structures, stronger governance, and increased regulation. Investors now demand greater transparency, and regulators keep a closer eye on systemic risks. While some smaller funds still operate with a boutique feel, the largest resemble global asset-management firms.

Risks and Criticisms

No discussion of hedge fund structures would be complete without addressing the risks and criticisms.

- High Fees: Many critics argue that the traditional fee model favors managers too heavily, especially when returns don’t justify the costs.

- Complexity: Hedge funds can use leverage, derivatives, and exotic strategies that are hard for investors to fully understand.

- Liquidity: Investors may face restrictions on withdrawing their money, sometimes waiting months or even years.

- Concentration of Power: In some funds, a single manager wields enormous influence, creating “key person risk.”

These risks don’t make hedge funds bad investments, but they highlight why understanding structure is essential.

Key Takeaways for Novice Investors

If you’re new to investing, here are the main points to remember about hedge fund structures:

- Hedge funds are typically structured as partnerships, with managers (general partners) running the fund and investors (limited partners) providing capital.

- Fees usually combine a management fee (to cover costs) and a performance fee (to share profits). Look out for mechanisms like high-water marks and hurdle rates.

- The manager is the central figure, but investment committees and service providers add oversight and credibility.

- Incentives are everything. The best funds align the manager’s interests with investors’ through fees, personal investment, and governance.

- Structure matters because it shapes risk, transparency, and potential returns.

Final Thoughts

Hedge funds can seem intimidating, but at their heart they’re just structured partnerships designed to pool money and chase returns in flexible ways. Their fee models, managerial setups, and incentive structures exist to balance risk and reward between managers and investors.

For novice investors, you don’t need to master every technical detail. What matters most is grasping the big picture: hedge funds are run by people whose interests may or may not align with yours. By understanding the structure, you can better evaluate whether a fund is worth the fees, the risks, and the commitment.

And remember—hedge funds are just one part of the investing universe. They’re not right for everyone, and they’re not always the “smart money” they claim to be. But they do offer valuable lessons in how incentives drive behavior, how structures shape outcomes, and how investors and managers navigate the fine balance of risk and reward.

{kind=link}