This Content Is Only For Subscribers

For investors exploring private credit, direct lending to middle-market companies is often the most familiar and widely implemented strategy. These loans provide an opportunity to earn attractive yields while financing companies that are too large for small-business loans but too small, or too complex, to access public capital markets.

This article dives into what direct lending is, how it works, the types of loans involved, potential returns, risks, and why it has become one of the fastest-growing segments of private credit.

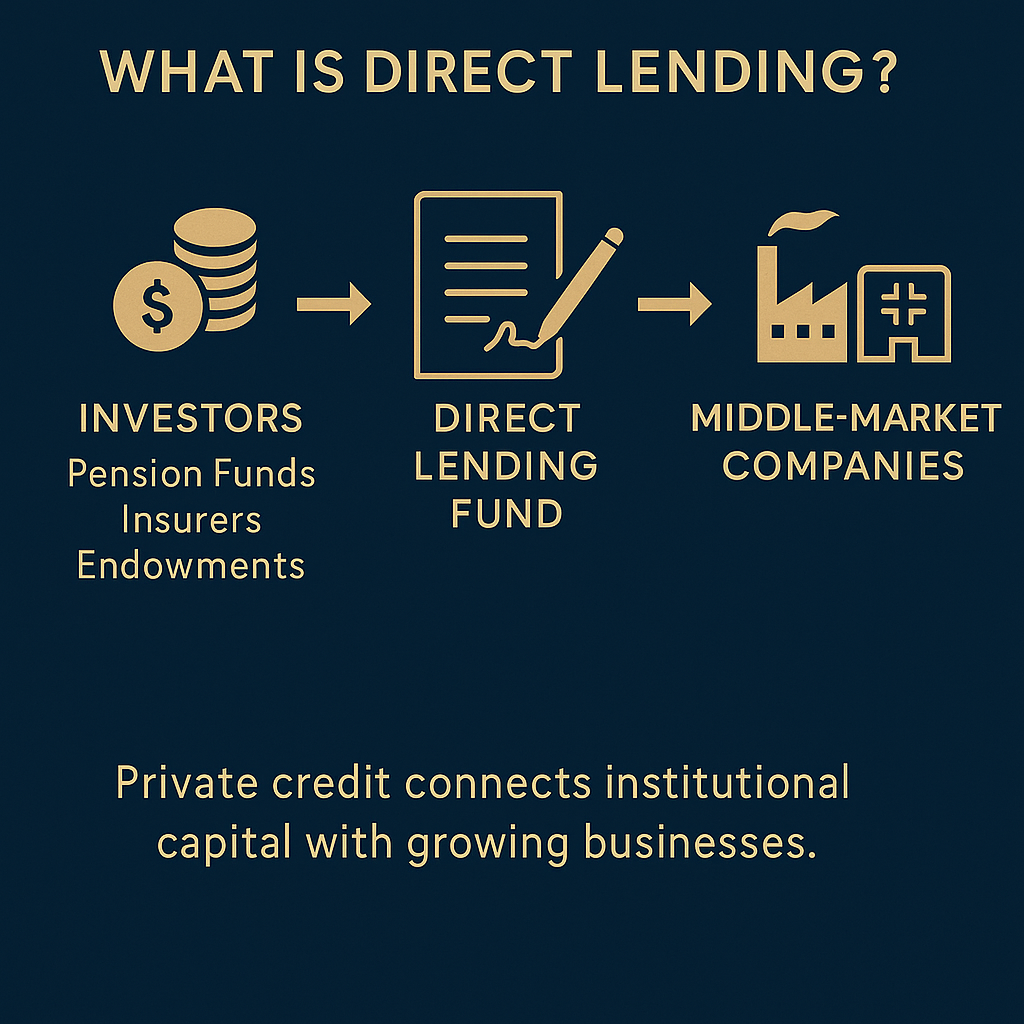

What Is Direct Lending?

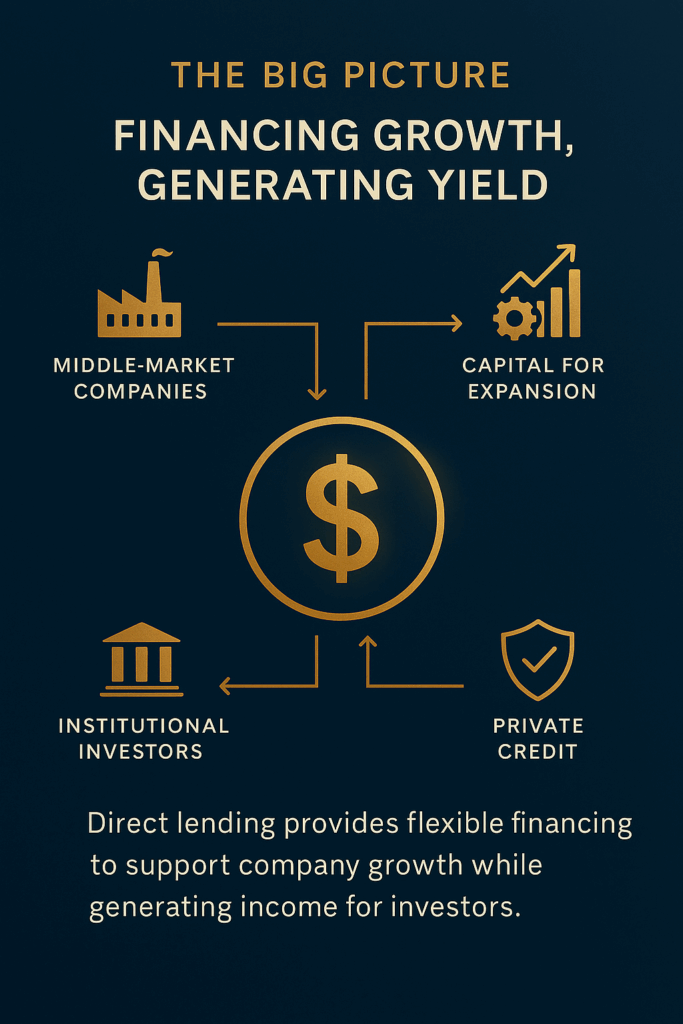

Direct lending is the practice of private funds lending money directly to companies, rather than investing in public bonds or purchasing syndicated bank loans. These funds raise capital from institutional investors—pension funds, insurance companies, endowments, and family offices—and deploy it to provide loans to businesses in need of capital.

Unlike traditional bank lending, direct lending funds can offer customized loan structures, faster approval processes, and flexibility in terms and covenants. Borrowers benefit from access to capital that might otherwise be unavailable, while investors gain exposure to private companies with potential for consistent income.

Who Are Middle-Market Companies?

Middle-market companies are typically defined by annual revenues between $50 million and $1 billion. They operate in a wide range of industries, including healthcare, manufacturing, technology, consumer goods, and business services.

These companies often need capital for:

- Acquisitions or buyouts

- Working capital and operational expansion

- Recapitalizations or refinancing existing debt

Unlike large public corporations that can issue bonds in global markets, middle-market companies often lack access to public debt, making private credit a crucial funding source.

Types of Direct Lending

Direct lending funds employ several loan structures, each with varying risk and return profiles:

1. Senior Secured Loans

Senior loans have first claim on a company’s assets if it defaults. They are typically lower risk than other private credit strategies and offer interest rates above public bonds.

Example: A manufacturing firm borrows $75 million to acquire a smaller competitor. The loan is senior secured, backed by the firm’s assets, and pays SOFR + 600 basis points.

2. Unitranche Loans

Unitranche loans combine senior and subordinated debt into a single loan structure. This simplifies administration for the borrower while offering investors blended yield, often higher than traditional senior loans.

Example: A tech company with $200 million in revenue wants to fund a new product line. A direct lending fund provides a $50 million unitranche loan at 9% interest, blending senior and mezzanine risk.

3. Mezzanine or Second-Lien Loans

These loans are subordinate to senior debt but often offer higher yields to compensate for increased risk. Mezzanine loans may include equity kickers, such as warrants, to participate in potential upside.

Example: A healthcare provider seeks $40 million for expansion. A mezzanine loan at 12% includes a small equity stake for investors, providing upside if the company grows rapidly.

Why Direct Lending Has Grown

Several factors have fueled the expansion of direct lending in the last decade:

- Bank Retreat: Post-2008 regulations limited banks’ lending capacity, leaving a gap for private funds to fill.

- Private Equity Demand: Many middle-market companies are backed by private equity sponsors who prefer direct lending for quick, flexible financing.

- Investor Appetite for Yield: In low-interest-rate environments, direct lending offers returns higher than public bonds, with downside protection from collateral.

According to Preqin, direct lending funds represent the largest segment of private credit, with billions deployed annually to middle-market borrowers.

Returns and Investor Benefits

Direct lending typically provides stable, predictable income, often in the 7–12% annual range, depending on the loan type and borrower profile. Because many loans are floating rate, investors can benefit when interest rates rise.

Other benefits include:

- Collateral protections: Most loans are secured by company assets.

- Covenants: Loan agreements may include financial tests and operational restrictions to reduce risk.

- Diversification: Investing in multiple loans across industries and geographies reduces exposure to any single borrower.

Risks of Direct Lending

While direct lending can be attractive, it carries risks investors must understand:

- Credit Risk: Borrowers may default if business conditions deteriorate.

- Illiquidity: Loans are often held until maturity, making early exit difficult.

- Economic Cycles: Recessions increase default rates, especially in cyclical industries.

- Sponsor Dependency: Loans to private equity-backed companies rely on the sponsor’s ability to manage operations and support the company financially.

Careful underwriting, diversification, and ongoing monitoring are critical to mitigating these risks.

Portfolio Role

Direct lending is often used as a core income strategy within broader portfolios. It can complement public bonds, equities, and other private market investments:

- Income generation: Regular interest payments can help meet cash flow needs.

- Low equity correlation: Defaults tend to be idiosyncratic rather than systemic.

- Inflation hedge: Floating-rate loans rise with benchmark interest rates, offsetting inflation.

Investors should assess how direct lending fits their risk tolerance, time horizon, and overall asset allocation.

Conclusion

Direct lending to middle-market companies is one of the most accessible and widely used private credit strategies. It provides companies with flexible financing while offering investors the opportunity to earn attractive yields, backed by collateral and covenants.

For novice investors, the key takeaway is that not all private credit is created equal. Direct lending stands out for its combination of risk-adjusted returns, structural protections, and portfolio diversification benefits. Understanding the mechanics of these loans—and the underlying companies—is essential for anyone considering exposure to this growing asset class.

{kind=link}