This Content Is Only For Subscribers

Investing is never static. Every decade, investors discover—or rediscover—asset classes that respond to shifting markets, regulations, and investor needs. In the 1980s, it was junk bonds. In the 1990s, it was hedge funds. In the 2000s, private equity gained center stage. And over the last decade, private credit has emerged as one of the fastest-growing and most important corners of global finance.

Private credit simply means lending that takes place outside of traditional banks or public bond markets. But while the definition is simple, the strategies within private credit are wide-ranging, from straightforward corporate loans to highly specialized financings linked to real estate, royalties, or even lawsuits. For investors, private credit has become a crucial way to generate yield, diversify portfolios, and access opportunities once reserved for institutions.

This article explores the major types of private credit strategies—direct lending, real estate credit, asset-backed and specialty finance, and distressed or opportunistic investing—alongside the history, growth drivers, risks, and future outlook of this evolving market.

How Private Credit Became a Market Powerhouse

To appreciate why private credit matters today, you have to rewind to the pre-2008 era. Back then, banks dominated corporate lending. If a midsize company needed to borrow $100 million to fund an acquisition or refinance debt, it called its bank. Banks issued loans, syndicated them, and kept credit flowing.

The Global Financial Crisis (GFC) changed everything. Regulators imposed new rules requiring banks to hold more capital and reduce riskier exposures. Loans to middle-market companies, real estate developers, or complex projects suddenly looked less attractive for banks.

At the same time, investors were dealing with a world of near-zero interest rates. Traditional bonds paid paltry yields, and savers struggled to generate income. This created an enormous gap: companies needed credit, and investors needed yield.

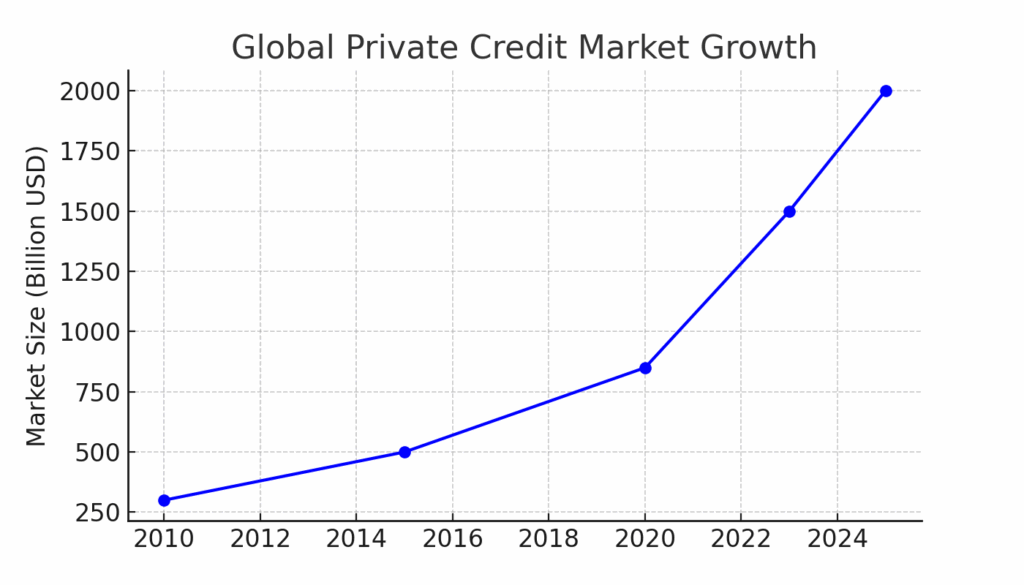

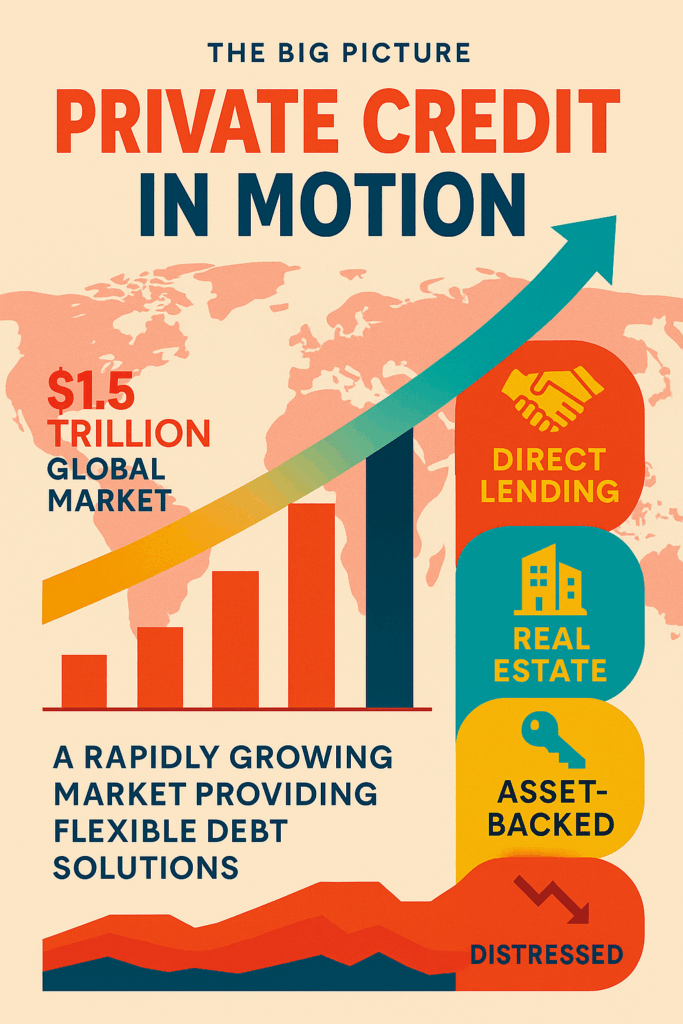

Private credit funds stepped into the breach. Managers raised pools of capital specifically to lend where banks no longer could. What began as a niche solution has ballooned into a $1.5 trillion global market as of 2023 (PitchBook). Analysts expect it could top $2 trillion by the middle of the decade.

Why Investors Care About Private Credit

Private credit sits at the intersection of opportunity and necessity. For companies, it’s a source of flexible financing when public debt markets or banks are not an option. For investors, it offers several appealing features:

- Attractive yields: Loans often pay 2–5% more than comparable public bonds.

- Downside protections: Many deals are secured by assets and structured with covenants.

- Diversification: Returns have historically shown low correlation to equities.

- Floating-rate exposure: Many loans reset with interest rates, providing a hedge against inflation.

The trade-offs are real: private credit is illiquid (capital is locked up for years), risky (borrowers may default), and complex (strategies vary widely). But for investors willing to accept those challenges, the potential rewards can be compelling.

The Major Strategies in Private Credit

Let’s walk through the four dominant categories of private credit, with examples of how each works.

1. Direct Lending to Middle-Market Companies

Direct lending is the foundation of private credit. These are loans—usually senior secured—made directly to middle-market companies that lack easy access to public bond markets.

Who borrows? Companies with annual revenues between $50 million and $1 billion. They’re too small to issue bonds efficiently but too large or complex for a simple bank loan.

Loan types:

- Senior secured loans (first claim on assets).

- Unitranche loans (a blend of senior and subordinated debt in one package).

- Second-lien or mezzanine loans (riskier layers of capital).

Case Example: Healthcare Expansion

A regional healthcare provider with $500 million in revenue wants to acquire a competitor. A private credit fund offers a $150 million unitranche loan with a floating rate of SOFR + 650 basis points. Investors earn steady income; the company gets financing without diluting equity ownership.

Case Example: Tech Recapitalization

A software company backed by private equity needs to refinance existing debt. A direct lending fund steps in with a $75 million senior loan. Investors benefit from recurring subscription revenues as collateral.

New Angle: Why Direct Lending Took Off

Direct lending became especially popular in the 2010s when private equity firms began relying on it to fund buyouts. Rather than negotiate with a syndicate of banks, sponsors could work with one or two private credit funds to secure all financing in a single package. This speed and certainty of execution was worth paying a higher interest rate.

Risks: If economic conditions deteriorate, companies may struggle to meet obligations. Even senior loans can default. Funds mitigate risk by diversifying across dozens or hundreds of borrowers.

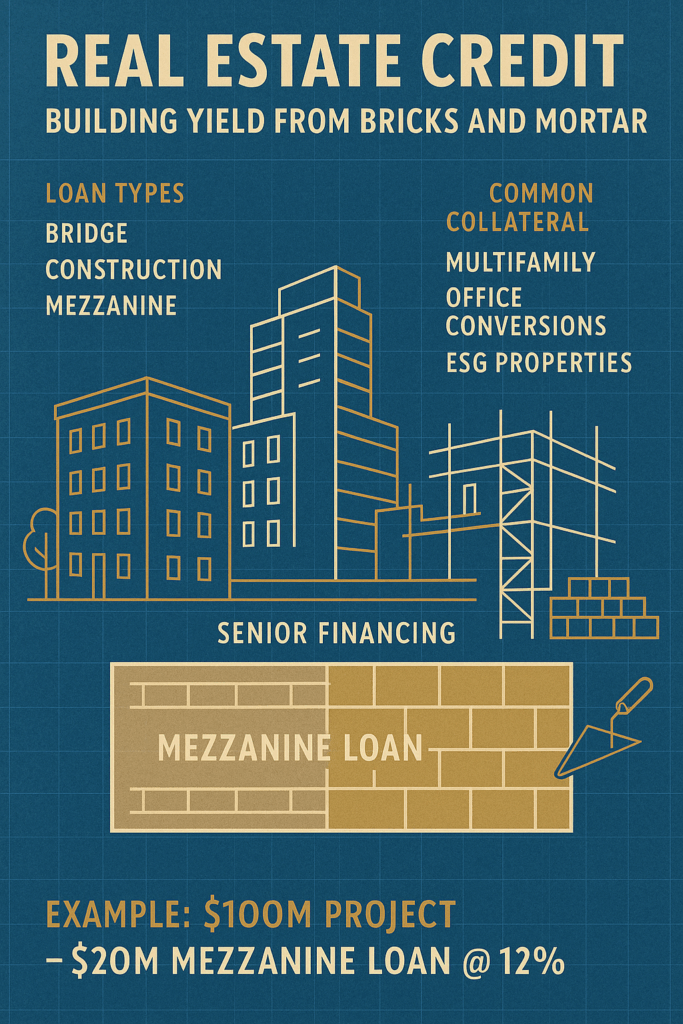

2. Real Estate-Backed Credit Opportunities

Private credit also flourishes in real estate, where funds provide loans backed by physical properties. Unlike direct ownership, lending offers steady income with the property serving as collateral.

Key structures:

- Bridge loans: Short-term financing until permanent capital is secured.

- Construction loans: Funding new developments.

- Mezzanine loans: Subordinate to senior debt but ahead of equity.

Case Example: Multifamily Development

A developer plans a $100 million apartment project. A bank provides $65 million in senior financing. A private credit fund adds a $20 million mezzanine loan at 12% interest. If the project succeeds, investors earn high returns. If not, they have a claim on the building.

Case Example: Office-to-Residential Conversion

In the wake of remote work, office buildings in major cities have lost tenants. A developer wants to convert one property into apartments. A private credit fund provides a $40 million bridge loan, betting on strong housing demand.

New Angle: ESG and Real Estate Credit

An emerging theme is green real estate lending. Funds are increasingly financing projects that meet energy efficiency standards, from solar-powered warehouses to LEED-certified office towers. Investors gain exposure to sustainability while supporting transition goals.

Risks: Real estate is cyclical. Rising rates, falling demand, or regulatory issues can impair collateral values.

3. Asset-Backed and Specialty Finance

This category involves loans secured by specific cash flows or niche assets. It’s one of the most creative parts of private credit.

Examples:

- Consumer loans: Pools of auto, credit card, or student loans.

- Equipment finance: Loans secured by planes, trucks, or medical machines.

- Royalty finance: Advances against future royalties from drugs, patents, or music.

- Litigation finance: Capital to fund lawsuits in exchange for a share of outcomes.

Case Example: Auto Loan Portfolio

A specialty finance fund buys $200 million in auto loans originated by a fintech lender. Investors earn yield from consumer repayments, with cars as collateral.

Case Example: Biotech Royalties

A biotech firm with an FDA-approved drug sells $100 million in royalty rights to a fund to finance new research. Investors receive cash flows tied to future drug sales.

New Angle: Technology’s Role

Fintech platforms are revolutionizing specialty finance. Online lenders originate small business or personal loans, then package them for private credit funds. This creates new opportunities—but also raises questions about underwriting quality.

Risks: Collateral can be illiquid and uncertain. Defaults, obsolescence, or failed lawsuits can result in losses.

4. Opportunistic, Distressed, and Special Situations Credit

The most complex—and often highest yielding—part of private credit involves lending into challenging or unusual circumstances.

Types:

- Distressed debt: Buying debt of companies near bankruptcy at steep discounts.

- Special situations: Financing restructurings, spin-offs, or recapitalizations.

- Opportunistic credit: Taking advantage of temporary market dislocations.

Case Example: Energy Restructuring

An oilfield services company struggles with debt as energy prices collapse. A distressed fund buys its bonds at 40 cents on the dollar, later profiting when oil rebounds.

Case Example: COVID Liquidity Crunch

In March 2020, travel firms faced sudden cash shortages. Opportunistic funds offered loans at high interest rates, providing a lifeline while capturing attractive yields.

New Angle: Where This Fits for Investors

Distressed and opportunistic credit can be highly profitable but are best suited for institutional investors or sophisticated individuals. These strategies require patience, deep expertise, and the ability to withstand volatility.

Risks: If recoveries don’t materialize, losses can be significant.

How Private Credit Funds Are Structured

Investors access private credit through several vehicles:

- Closed-End Funds: Capital committed for 5–10 years; typical for institutions.

- Business Development Companies (BDCs): Publicly traded, accessible to retail investors.

- Interval Funds: Semi-liquid, allowing quarterly redemptions.

- Evergreen Funds: Open-ended structures gaining popularity.

Funds earn money from management fees (often ~1%) and incentive fees tied to performance.

New Angle: Transparency Challenges

One ongoing debate is how private credit funds report performance. Unlike public bonds, which trade daily and have visible prices, private loans are valued infrequently. This can smooth out volatility but may give a misleading sense of stability.

Who Invests in Private Credit?

Historically, private credit was dominated by:

- Pension funds needing predictable income.

- Insurance companies matching long-term liabilities.

- Endowments and foundations seeking diversification.

Now, it’s opening to:

- Family offices and high-net-worth individuals via feeder funds.

- Retail investors through BDCs, interval funds, and ETFs.

New Angle: Democratization

Retail access is a double-edged sword. On one hand, it opens income-generating strategies to more people. On the other, it raises concerns about whether everyday investors understand the risks of illiquidity and credit defaults.

Risks and Considerations

Private credit is not risk-free. Key risks include:

- Illiquidity: Capital often locked up for years.

- Credit risk: Borrowers can default.

- Market cycles: Recessions increase default rates.

- Complexity: Specialty or distressed strategies require expertise.

Mitigants include collateral, diversification, and careful underwriting.

New Angle: Macro Risks

One overlooked issue is how private credit will behave in a prolonged downturn. Because the industry grew after 2008, it has not been tested through a deep credit cycle. Investors should temper return expectations with caution.

Global Growth of Private Credit

While the U.S. leads the market, Europe and Asia are catching up. European banks face similar lending restrictions, and Asian economies are exploring private credit as a growth tool. Global funds are expanding rapidly, offering investors geographic diversification.

Case Example: India’s Infrastructure Credit

Private credit funds are financing renewable energy and logistics projects in India, where traditional banks face constraints. This highlights the role private credit can play in supporting economic development.

The Future of Private Credit

Looking ahead, several trends stand out:

- Higher Interest Rates: Benefit floating-rate loans but pressure borrowers.

- Retail Access: New products for individual investors will expand the market.

- Technology: Fintech platforms streamline origination and monitoring.

- Regulation: Authorities are watching growth closely, balancing innovation and risk.

- ESG Integration: Expect more funds to tie lending practices to sustainability metrics.

Conclusion

Private credit has grown from a niche afterthought into a mainstream asset class. By offering direct lending to companies, financing real estate projects, backing unique assets, or diving into distressed opportunities, it provides investors with a wide toolkit to generate income and diversify portfolios.

For novice investors, the lesson is simple: private credit isn’t one-size-fits-all. Each strategy carries its own balance of risk and reward. Understanding those differences is the key to seeing where private credit might fit in your broader financial journey.

{kind=link}