In What Is a Real Estate Fund? we laid out the foundation of how these investment vehicles work and why investors turn to them. But if you’re thinking long term, one question quickly rises to the surface: Can I hold a real estate fund inside my retirement account?

For many investors, IRAs—Individual Retirement Accounts—are the cornerstone of their retirement planning. These vehicles allow your investments to grow tax-deferred (traditional IRA) or tax-free (Roth IRA), making them powerful wealth-building tools. But not every investment is IRA-friendly, and real estate funds can occupy a gray area.

So what makes a real estate fund IRA-compatible? Let’s unpack the rules, benefits, and challenges so you know what to expect before taking the leap.

The Basics: Real Estate in an IRA

At a high level, IRAs allow you to hold a wide range of assets: stocks, bonds, mutual funds, ETFs, and, in many cases, alternative assets like real estate. But there’s a catch: traditional brokerage IRAs often restrict investments to publicly traded securities. If you want to hold private real estate funds, you’ll usually need a self-directed IRA (SDIRA)—a specialized account that opens the door to nontraditional investments.

Types of Real Estate Funds You Can Hold

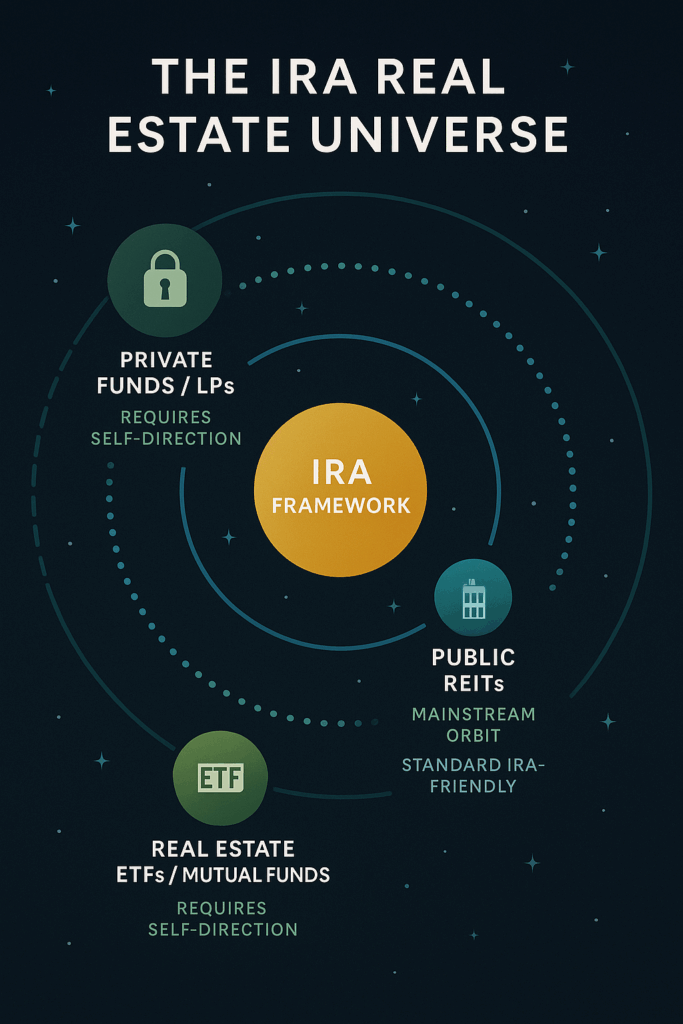

- Publicly Traded REITs

These are the easiest fit. Because they trade like stocks, most brokerage IRAs already allow them. Buying shares of a public REIT inside your IRA is as simple as buying Apple or Microsoft. - Private Real Estate Funds (LPs, Syndications)

These require a self-directed IRA. You can use an SDIRA to invest in private placements, limited partnerships, and even syndications. The account custodian facilitates the transaction, and the investment is held inside your IRA. - Real Estate Mutual Funds and ETFs

Many traditional IRA custodians offer real estate–focused mutual funds or ETFs. While not direct property ownership, they give you diversified exposure to the sector without leaving the IRA’s standard menu.

Benefits of Using an IRA for Real Estate Funds

- Tax Advantages

The biggest draw is the tax treatment. With a traditional IRA, income and gains from real estate funds grow tax-deferred. With a Roth IRA, qualified withdrawals can be entirely tax-free. That means dividends, rental distributions, and appreciation can compound without the IRS taking a bite each year. - Diversification

Real estate often behaves differently from stocks and bonds, providing balance in a retirement portfolio. Including funds in an IRA can reduce overall volatility. - Long-Term Growth

Real estate is generally a long-horizon investment, which pairs well with the long-term nature of retirement accounts. Locking up capital for several years in a private fund makes sense inside a vehicle you’re not touching until retirement anyway.

Challenges and Considerations

- Liquidity

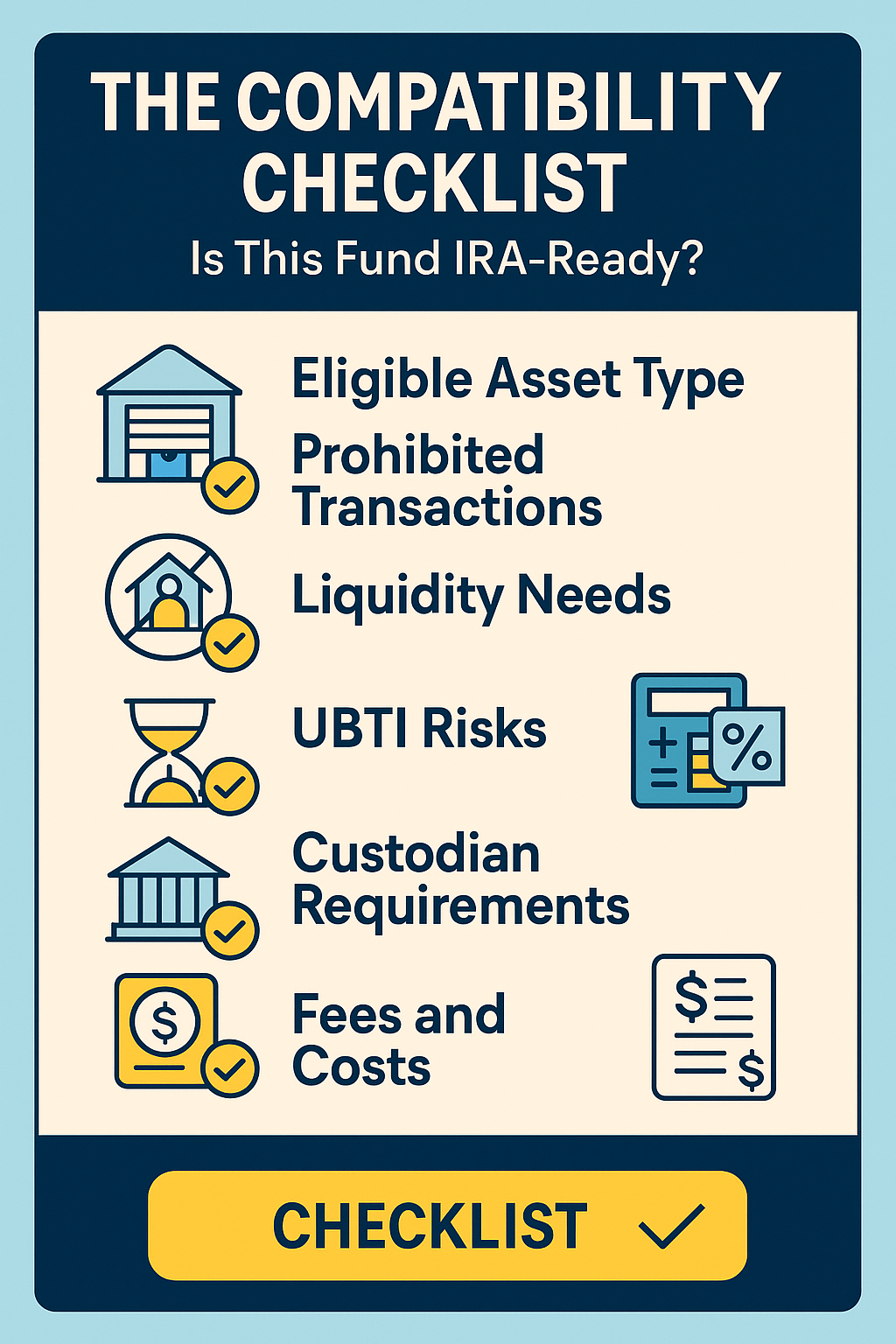

IRA funds are intended for retirement, but required minimum distributions (RMDs) kick in at age 73 (for traditional IRAs). If your IRA is heavily invested in illiquid real estate funds, generating cash for those distributions can get tricky. - Prohibited Transactions

The IRS sets strict rules on what you can and cannot do with IRA assets. For example, you can’t live in or personally benefit from a property your IRA invests in. Likewise, you can’t lend money to or transact with “disqualified persons” such as close family members. Violating these rules can disqualify the entire IRA. - Unrelated Business Taxable Income (UBTI)

Some private real estate funds use leverage (borrowed money) to boost returns. While leverage is common, it can trigger something called UBTI, which means your IRA might owe taxes even though it’s normally tax-deferred. Not all funds generate UBTI, but it’s a key detail to check before investing. - Custodian and Fees

Setting up a self-directed IRA requires working with a custodian who specializes in alternative assets. These accounts often come with higher fees and more paperwork than traditional brokerage IRAs.

Is It Worth It?

So should you hold real estate funds inside your IRA? The answer depends on your strategy:

- If you want simple exposure and easy management, publicly traded REITs inside a standard IRA may be enough. They provide liquidity, dividends, and sector exposure without complexity.

- If you want to diversify into private funds or syndications, an SDIRA opens the door—but be prepared for more due diligence, possible UBTI tax issues, and limited liquidity.

Either way, pairing retirement tax advantages with real estate’s income and appreciation potential can be a smart move—if done carefully.

The Bottom Line

What makes a real estate fund IRA-compatible comes down to structure and rules. Public REITs slide easily into retirement accounts. Private funds can fit too, but only through a self-directed IRA and with extra attention to tax and regulatory details.

For investors, the appeal is obvious: using tax-advantaged accounts to harness real estate’s wealth-building power. But as with all retirement planning, the devil is in the details. Make sure you consult with your IRA custodian, financial advisor, or tax professional before committing.

In the end, as What Is a Real Estate Fund? showed us, the structure shapes your experience. Pairing the right type of fund with the right type of account could be the difference between a solid retirement strategy and an expensive misstep.

{kind=link}