This Content Is Only For Subscribers

Venture capital (VC) is one of those terms that shows up constantly in headlines but often feels like an insider’s game. You’ll read that a startup “just raised a $50 million Series B” or that a new “unicorn” is worth over a billion dollars — but what does that really mean? And more importantly, why should everyday investors care?

The answer is that venture capital is one of the most powerful forces shaping innovation today. It’s the system that finances bold ideas, turns them into businesses, and, in some cases, builds companies that transform entire industries. But it’s also a world of risks, staggering failure rates, and structures that can seem opaque to outsiders.

In this article, we’ll take a deep dive into venture capital: how it works, how it started, why it matters, and how it continues to influence the global economy. We’ll explore not just the mechanics — fund structures, stages of investment, and returns — but also the cultural and economic impact of VC. Think of this as a comprehensive guide for novice investors who want to understand not only what venture capital is but why it plays such a pivotal role in innovation.

A Brief History of Venture Capital

Before we get to the mechanics, it’s worth looking at how venture capital came to be.

- Early days: Although wealthy families and individuals have funded risky ventures for centuries (think whaling expeditions or industrial-age inventions), modern venture capital really took shape in the United States after World War II.

- The first VC firm: In 1946, Georges Doriot, a Harvard Business School professor, co-founded American Research and Development Corporation (ARD). ARD is widely considered the first modern VC firm. Its most famous investment was in Digital Equipment Corporation (DEC), which turned a $70,000 investment in 1957 into $355 million at the time of its IPO in 1968. This one deal established the model for how a single “home run” could make an entire fund successful.

- Silicon Valley’s rise: In the 1950s and 1960s, the area around Stanford University became a hub for technology startups. Fairchild Semiconductor, a company that spun out of Shockley Semiconductor Laboratory, became a training ground for future entrepreneurs and investors. The “Fairchildren,” as they were called, went on to found companies like Intel — and many became venture capitalists themselves.

- The 1980s and 1990s boom: As personal computing and the internet took off, venture capital became synonymous with Silicon Valley. Firms like Sequoia Capital, Kleiner Perkins, and Benchmark Capital backed companies that would go on to dominate the global economy — Apple, Amazon, Google, and more.

- Dot-com bust and recovery: The late 1990s saw an explosion of internet startups funded by VC money, followed by a crash in 2000–2001. Many funds lost money, but the survivors — both companies and VC firms — laid the groundwork for the modern internet economy.

- Today: Venture capital is now a global industry. While Silicon Valley remains its symbolic center, China, India, Europe, Latin America, and Africa all have thriving venture ecosystems.

The lesson from history is simple: venture capital is about concentrated bets on innovation, and sometimes one winner changes everything.

The Basics: What Exactly Is Venture Capital?

At its core, venture capital is a form of private equity investment focused on high-growth, early-stage companies. Unlike mutual funds or ETFs that invest in publicly traded stocks and bonds, VC deals are private.

Here’s the basic model:

- A VC firm raises money from institutional investors — pension funds, endowments, insurance companies, sovereign wealth funds, and wealthy individuals. These investors are called limited partners (LPs).

- The VC firm itself, run by professional investors known as general partners (GPs), manages the fund. The GPs decide which startups to invest in.

- The money is pooled into a fund with a fixed lifespan (usually 10–12 years).

- The fund invests in startups over the first few years, supports them as they grow, and aims to exit those investments via IPOs, acquisitions, or secondary sales.

The goal is to generate high returns for the LPs, while also earning fees and a share of the profits for the GPs.

The High-Risk, High-Reward Equation

Venture capital is often described as a high-risk, high-reward asset class. That’s not just a catchphrase — it’s a reflection of the brutal math of startup investing.

- Failure rates: Estimates vary, but research from Harvard Business School and others suggests that around three-quarters of venture-backed startups may never return cash to investors. Some fail outright, while others limp along without generating meaningful returns. Exact percentages differ depending on definitions, but the bottom line is clear: most startups don’t make it.

- Power law returns: Despite these odds, VC funds are structured around the idea that one or two big wins can make up for dozens of failures. This is called the power law distribution of returns. In a portfolio of 20 companies, maybe 15 will fail, a few will return 2–3 times the investment, and one could return 50 or 100 times. That one “home run” drives the fund’s overall performance.

- Unicorns: The term “unicorn” refers to a private company valued at $1 billion or more. While rare in theory, the number of unicorns has exploded in the past decade, thanks to large late-stage funding rounds. Still, only a tiny fraction of startups ever reach this level.

For investors, the message is sobering: VC is not about batting averages, it’s about hitting home runs.

How a Venture Capital Fund Works

To understand VC, you need to know how the funds themselves are structured.

Fund Size and Structure

Fund sizes vary widely. Some institutional funds manage billions, while others focus on smaller, niche strategies with funds under $100 million. Median and average fund sizes change over time and by strategy. For example, in the U.S., the average VC fund size has grown significantly in the last decade as institutional investors have poured more money into the asset class.

The Lifecycle of a Fund

- Years 1–3: Investment period. The fund actively invests in startups, writing checks across different stages.

- Years 4–7: Value creation. The focus shifts to helping portfolio companies grow — hiring executives, refining business models, expanding internationally.

- Years 5–10: Exits. Successful companies go public, get acquired, or provide liquidity through secondary share sales.

- Years 10–12: Extensions. Funds often seek one or two extensions to wrap up remaining investments.

Capital Calls

Unlike mutual funds, where investors commit money upfront, VC funds use a system of capital calls. LPs commit, say, $100 million to a fund, but they don’t send all the money at once. Instead, the VC calls portions of that capital as needed to make investments.

Fees and Incentives

The VC firm makes money in two ways:

- Management fees: Typically around 2% of assets annually, used to pay salaries and overhead.

- Carried interest (“carry”): Usually 20% of the profits above a certain threshold. This aligns the GPs with the LPs — the VCs only make real money if the startups succeed.

Stages of VC Investment

Startups don’t raise all their money at once. Instead, they go through funding stages:

- Seed Stage: Small amounts of money to prove the concept, build a prototype, or test the market. Often $250,000–$2 million, though this varies by geography.

- Series A: The first significant round of institutional VC, often $5–$15 million. Focus is on building a real business model and scaling the team.

- Series B, C, and beyond: Larger rounds that can run into the tens or hundreds of millions, funding expansion into new markets or acquisitions.

- Late Stage / Pre-IPO: Huge rounds designed to help companies dominate their markets before going public.

Each stage carries different risks and potential returns. Seed-stage deals are riskier but can deliver massive returns. Late-stage deals are safer but have less upside.

Case Studies: Venture Capital in Action

Google (1999)

When Google raised its $25 million Series A from Sequoia Capital and Kleiner Perkins, it already had a promising search engine. The funding allowed it to scale servers, hire engineers, and eventually dominate the search market. Today, Alphabet (Google’s parent) is one of the most valuable companies in the world.

Airbnb (2009)

Airbnb’s seed funding from Sequoia helped it move beyond an oddball idea (air mattresses in living rooms) to a global travel platform. Without VC money, Airbnb might have remained a quirky side hustle.

Moderna (2010s)

Biotech companies often require years of research before revenue. Moderna raised billions in venture capital before its IPO, funding its mRNA research. When COVID-19 hit, that groundwork allowed it to develop a vaccine in record time.

Stripe (2010s–2020s)

Stripe’s series of VC rounds from firms like Sequoia and Andreessen Horowitz fueled its rise into one of the world’s most valuable private companies, powering payments for millions of businesses worldwide.

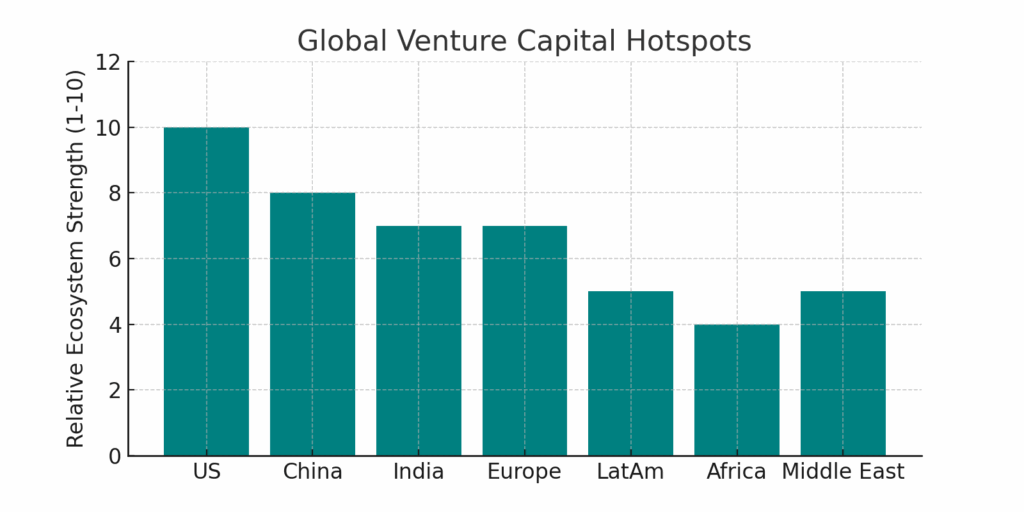

Geographic Hotspots

Venture capital is now global. Here’s a quick tour:

- United States: Still the largest market, with Silicon Valley, New York, Boston, and Austin as key hubs.

- China: Home to giants like Alibaba, Tencent, and ByteDance. Despite regulatory crackdowns, VC remains active.

- India: A booming ecosystem with startups like Flipkart, Paytm, and Byju’s attracting billions.

- Europe: London, Berlin, Paris, and Stockholm are major hubs, especially in fintech and gaming.

- Latin America: Brazil and Mexico lead, with companies like Nubank and Rappi drawing global capital.

- Africa: Nairobi, Lagos, and Cape Town are hotspots, with fintechs like Flutterwave and Chipper Cash raising major rounds.

- Middle East: Dubai and Tel Aviv stand out, with strong government support and thriving tech sectors.

Trends Shaping Venture Capital

- Mega-funds: Firms like SoftBank have launched funds with tens of billions, reshaping late-stage investing.

- Corporate VC: Companies like Google, Intel, and Salesforce run their own venture arms.

- Climate tech and sustainability: Investors are pouring money into clean energy, electric vehicles, and climate solutions.

- Artificial intelligence: Startups in AI are attracting massive rounds, with investors betting on transformative change.

- Diversity and inclusion: VC is under pressure to back more diverse founders and expand access beyond traditional networks.

- Globalization: New hubs are emerging worldwide, and capital is more mobile than ever.

Criticisms and Challenges

- Concentration of Wealth: VC funding tends to flow to a narrow set of founders, often those with elite educations and networks.

- “Grow at All Costs” Culture: Some startups, under pressure to scale quickly, take unsustainable risks — think WeWork’s implosion.

- Valuation Bubbles: Critics argue that too much money chasing too few deals has inflated valuations.

- Liquidity and Access: VC is illiquid and usually limited to accredited investors or institutions, making it inaccessible to most individuals.

How Novice Investors Can Engage

For everyday investors, direct participation in VC is usually out of reach. But there are ways to get exposure:

- Funds of funds: Some vehicles pool capital to invest in VC funds.

- Public companies with VC arms: Investing in tech giants that also act as VCs.

- Venture-backed IPOs: Buying shares when VC-backed companies go public.

- Crowdfunding platforms: In some countries, regulations now allow retail investors to back startups directly, though risks remain high.

The Bigger Picture

Venture capital is not perfect. It’s risky, exclusive, and often criticized for fueling bubbles or inequity. But it is also one of the most important engines of innovation in the modern economy. From search engines to life-saving vaccines, many of the technologies we take for granted today wouldn’t exist — at least not in their current form — without VC backing.

For novice investors, the key takeaway is not to rush into venture deals, but to understand how innovation gets financed. Knowing how venture capital works gives you a window into the future — because somewhere out there, in a garage or a lab, a founder with VC backing is building the next company that could change the world.

{kind=link}