When it comes to saving for retirement through an Individual Retirement Account (IRA), one of the first questions new investors often ask is: How much can I contribute each year? The answer is set by the IRS, and the numbers can change from year to year as they adjust for inflation. For 2025, the limits are clear — but they come with a few important rules and exceptions that every saver should understand.

If you’ve read our complete guide on IRAs, you already know these accounts come in different forms, most commonly the Traditional IRA and the Roth IRA. Contribution limits apply to both types combined, meaning your total annual contributions across all IRAs can’t exceed the IRS maximum. Let’s break it down in plain language.

The 2025 IRA Contribution Limit

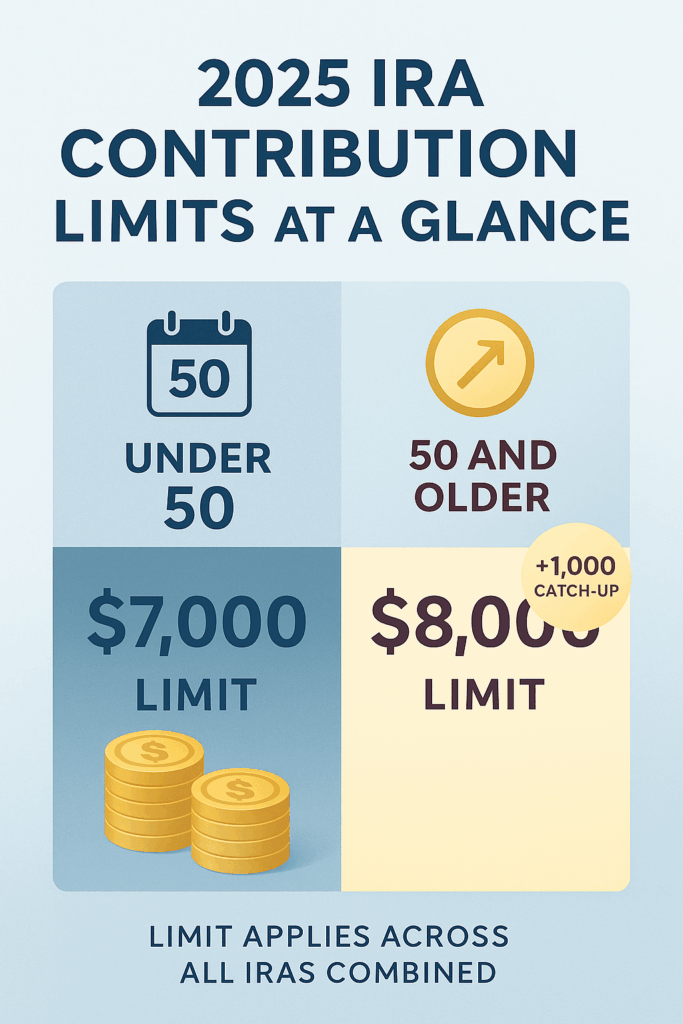

For 2025, the standard annual contribution limit is $7,000. If you’re age 50 or older, you’re allowed to contribute an additional $1,000 catch-up contribution, bringing your total to $8,000 if eligible.

This limit applies to the total amount you put into all of your IRAs combined — Traditional and Roth. For example:

- If you contribute $4,000 to a Traditional IRA in 2025, you can contribute up to $3,000 to a Roth IRA that same year (for a total of $7,000).

- If you’re 52 and put $6,000 into a Roth, you could still add $2,000 to a Traditional IRA, reaching your $8,000 cap.

It’s not $7,000 or $8,000 per account — it’s per person.

Who Can Contribute?

To make contributions to an IRA, you need to have earned income (like wages, salaries, or self-employment income). Investment income, rental income, or pension payments don’t count. For married couples, there’s a special rule: if one spouse doesn’t earn income, they may still be able to contribute through what’s called a spousal IRA, as long as the working spouse has enough earned income to cover both contributions.

Traditional IRA Deduction Limits

While anyone with earned income can contribute to a Traditional IRA, the ability to deduct those contributions on your tax return depends on whether you or your spouse are covered by a retirement plan at work, as well as your income (measured by modified adjusted gross income, or MAGI).

For 2025, here are the deduction phase-out ranges:

- Single filers covered by a workplace plan: Deduction phases out between $79,000 and $89,000 MAGI.

- Married couples filing jointly (contributor covered by a plan): Deduction phases out between $126,000 and $146,000.

- Married couples filing jointly (contributor not covered by a plan, but spouse is): Deduction phases out between $236,000 and $246,000.

- Married filing separately: Deduction phases out between $0 and $10,000 — meaning deductions disappear almost immediately at higher incomes.

If your income is below these ranges, your contribution is fully deductible. If it’s within the range, it’s partially deductible. And if it’s above, you can still contribute, but it won’t reduce your taxable income.

Roth IRA Income Limits

Roth IRAs work differently. Contributions are always made with after-tax dollars, but your ability to contribute directly depends on your MAGI.

For 2025:

- Single filers: Contribution limit phases out between $150,000 and $165,000 MAGI.

- Married filing jointly: Phases out between $236,000 and $246,000.

- Married filing separately: Phase-out range is $0 to $10,000.

If your income is below the range, you can contribute the full $7,000 (or $8,000 if you’re 50+). If you’re in the phase-out range, your contribution limit is reduced. And if your income is above the range, you can’t contribute directly to a Roth IRA — though some investors use a legal workaround called a backdoor Roth IRA (which requires careful tax reporting).

Catch-Up Contributions

For savers age 50 and over, the IRS allows an additional $1,000 contribution each year. This is called a catch-up contribution, and it’s designed to help people who may have started saving later in life or who want to boost their retirement balances as they approach retirement.

One important point: unlike some other retirement accounts, the IRA catch-up contribution is a flat $1,000 and does not adjust for inflation.

Special Note on Contribution Deadlines

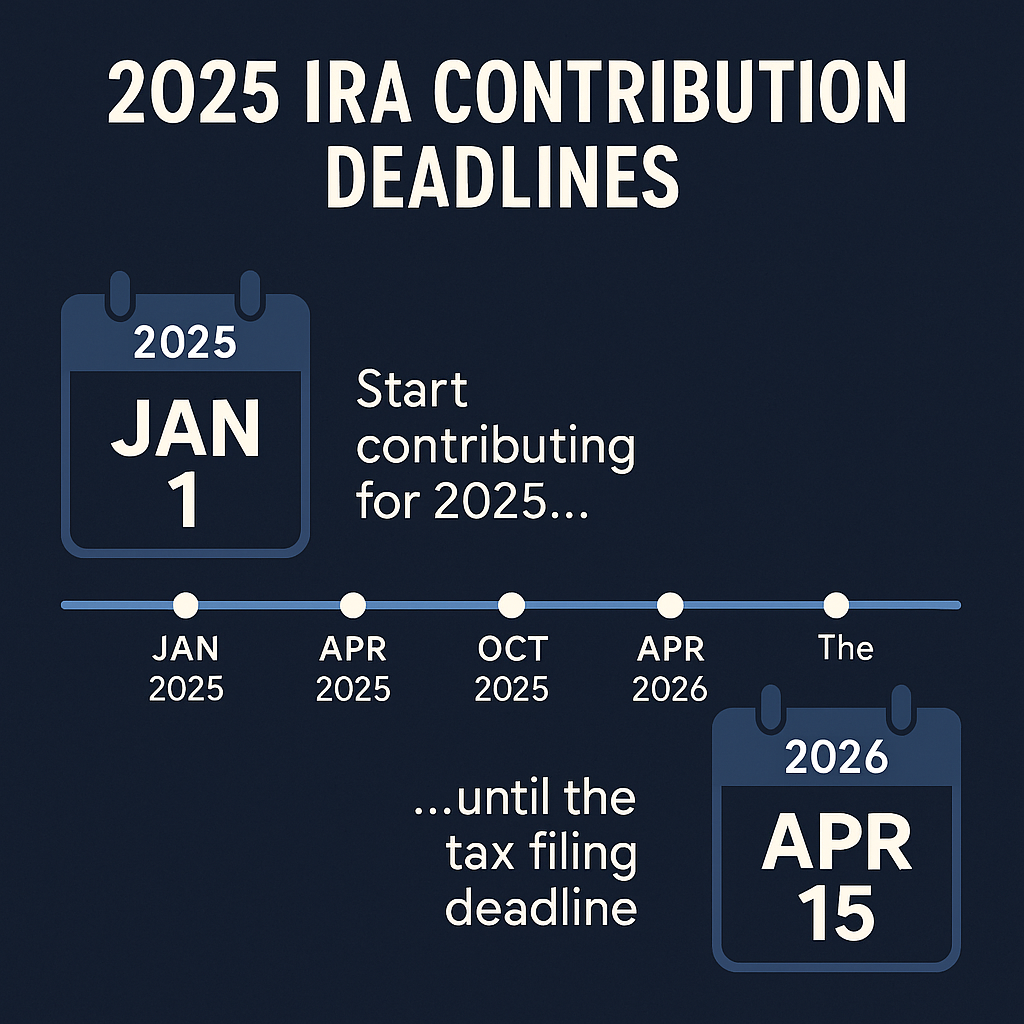

Another key detail: you don’t have to make your contribution by December 31. The deadline to contribute to an IRA for a given year is the tax filing deadline of the following year, usually April 15. For 2025 contributions, that means you have until April 15, 2026. This gives you extra time to evaluate your finances, consider your tax situation, and make the best choice.

Why Contribution Limits Matter

At first glance, $7,000 (or $8,000 if you’re 50+) may not sound like much, especially when thinking about the cost of retirement. But over time, consistent contributions can grow significantly thanks to compound growth.

For example:

- If you contribute $7,000 a year for 30 years and earn an average 7% return, you’d end up with over $710,000.

- If you start later and contribute $8,000 a year for 20 years with the same return, you’d have about $350,000.

The lesson? Start as early as you can, even if you can’t always max out the limit. Small contributions grow into big balances over time.

Key Takeaways

- The 2025 IRA contribution limit is $7,000 (or $8,000 if age 50 or older).

- Limits apply to the total of all your IRAs combined, not each account.

- Anyone with earned income can contribute to a Traditional IRA, but the ability to deduct contributions depends on MAGI and workplace plan coverage.

- Roth IRA contributions are income-limited, phasing out for higher earners.

- The deadline to make contributions for 2025 is April 15, 2026.

Final Thoughts

IRA contribution limits may not feel like the most exciting part of retirement planning, but they’re essential to understand. Knowing the rules helps you maximize your tax benefits, stay compliant with IRS regulations, and build wealth steadily over time. Whether you choose a Traditional IRA, a Roth IRA, or a mix of both, the most important step is to contribute consistently and take advantage of the tax benefits these accounts offer.

Retirement may seem far away, but every year’s contribution is a building block toward future financial freedom. And with the 2025 limits now set, there’s no better time to make a plan and put your money to work for tomorrow.

{kind=link}