This Content Is Only For Subscribers

Venture capital is gated by design. Early-stage companies are risky and illiquid, and U.S. securities law limits who can invest in most private offerings. Here’s a plain-English, tighter guide to what “accredited” means, how offerings work, and practical ways to participate.

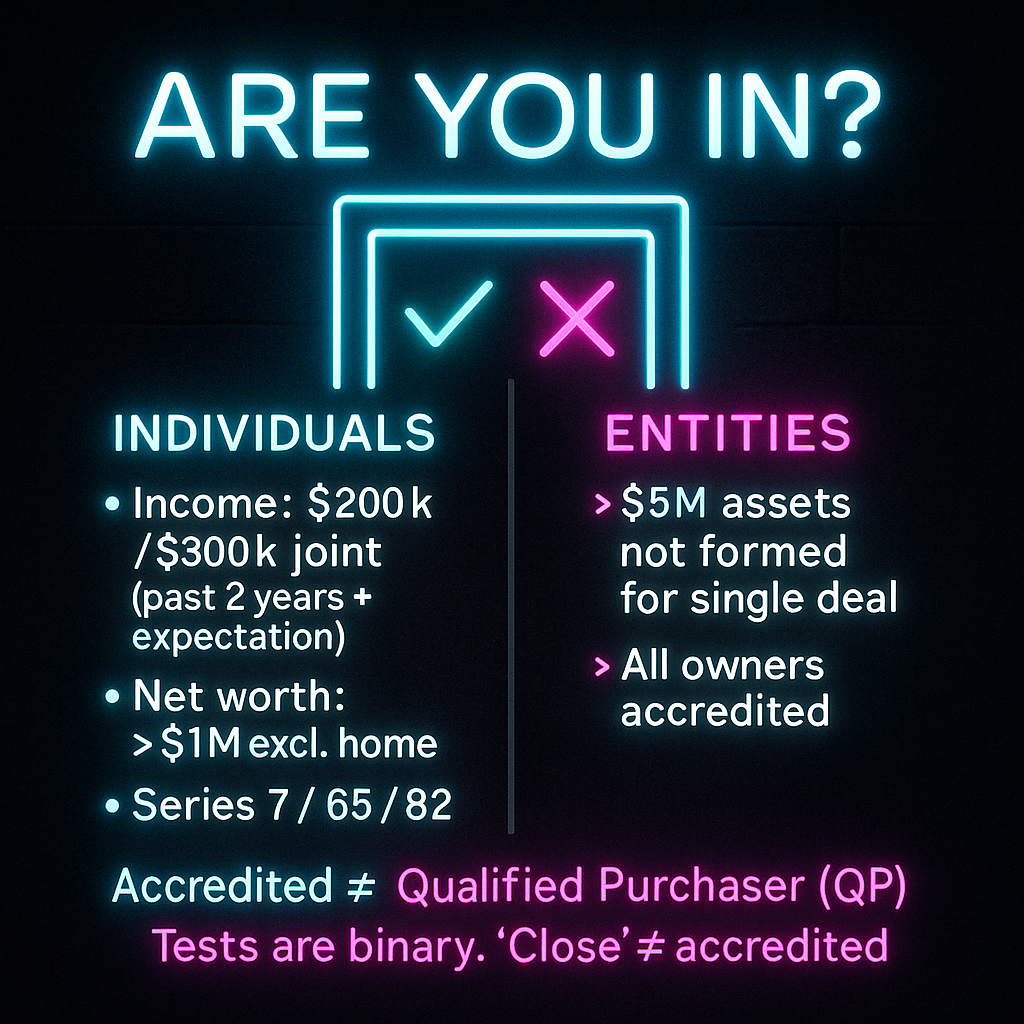

What “accredited investor” means

For individuals, you generally qualify by:

- Income: $200,000 in each of the past two years (or $300,000 with a spouse/partner) and a reasonable expectation of the same this year.

- Net worth: Over $1 million excluding your primary residence.

- Professional certifications: Certain licenses (e.g., Series 7, 65, 82).

Entities can qualify too—e.g., trusts or LLCs with over $5 million in assets (not formed just for one deal), or entities where every owner is accredited.

Keep two distinctions straight:

- Accredited investor ≠ qualified purchaser (QP). Some funds—especially larger ones—admit only QPs, a higher bar based on the amount of “investments” you already hold.

- The tests are binary. “Close” doesn’t count; managers must follow the line.

Why it matters for VC

Most venture funds and startup financings rely on private placement rules:

- Relationship-based offerings (Rule 506(b)). No public advertising; investors typically self-certify accredited status in a subscription questionnaire.

- Public-facing private offerings (Rule 506(c)). General solicitation is allowed, but issuers must take reasonable steps to verify accredited status—documents (W-2s, K-1s, statements) or a verification letter from a CPA/attorney/third party. A checkbox alone isn’t enough.

In practice, 506(b) is quieter with less paperwork; 506(c) is more visible and requires verification but can broaden access.

Paths into venture: funds, syndicates, rolling funds, direct checks

VC funds. You commit a fixed amount to a partnership; the fund calls capital over years and returns cash at exits. Pros: diversification and professional process. Cons: illiquidity and minimums.

Syndicates & SPVs. Pools for a single deal with lower minimums. Read the fee stack carefully (admin fees + carry can sit on top of the lead’s economics). Governance and information rights vary.

Rolling funds. Quarterly vehicles (often 506(c)) for recurring smaller checks. Ask how pro-rata and follow-ons work across cohorts.

Direct angel checks. You invest straight into a round. Confirm your accredited status, then focus on information rights, pro-rata, and transfer restrictions. Highest control, highest DIY.

If you’re not accredited (yet)

- Reg CF (equity crowdfunding): Anyone can invest within annual limits; disclosures vary and deals are very early.

- Reg A: Public-style offerings with caps and tiered disclosure—less “classic VC,” sometimes seen at growth stages.

- Public proxies: Listed vehicles (e.g., BDCs) or funds with late-stage exposure provide liquid, indirect access.

Regardless of path, mind illiquidity, concentration, and fees.

The verification experience (so you’re ready)

For 506(c) raises, expect:

- Document review: W-2s/tax returns for income; brokerage/credit report for net worth (with redactions).

- Third-party letter: A CPA/attorney confirms you qualify—often the easiest route.

- Platform verification: Some portals let you reuse a fresh letter across offerings.

Create a minimal redacted packet now to move quickly when you like an opportunity.

Practical risks—and how to manage them

- Illiquidity: Venture positions can take 7–12 years—and many never return capital. Size positions accordingly.

- Concentration: Funds diversify; SPVs don’t. Build a plan (how many SPVs or what fund % of net worth).

- Fees & carry: Get the all-in number. For SPVs, fees can quietly erode returns.

- Signal & access: Great deals are oversubscribed. Don’t chase logos—ask about sourcing, selection, and post-investment value add.

- Documentation: Read the memo and subscription. Confirm conflicts policy, follow-on approach, and reporting cadence.

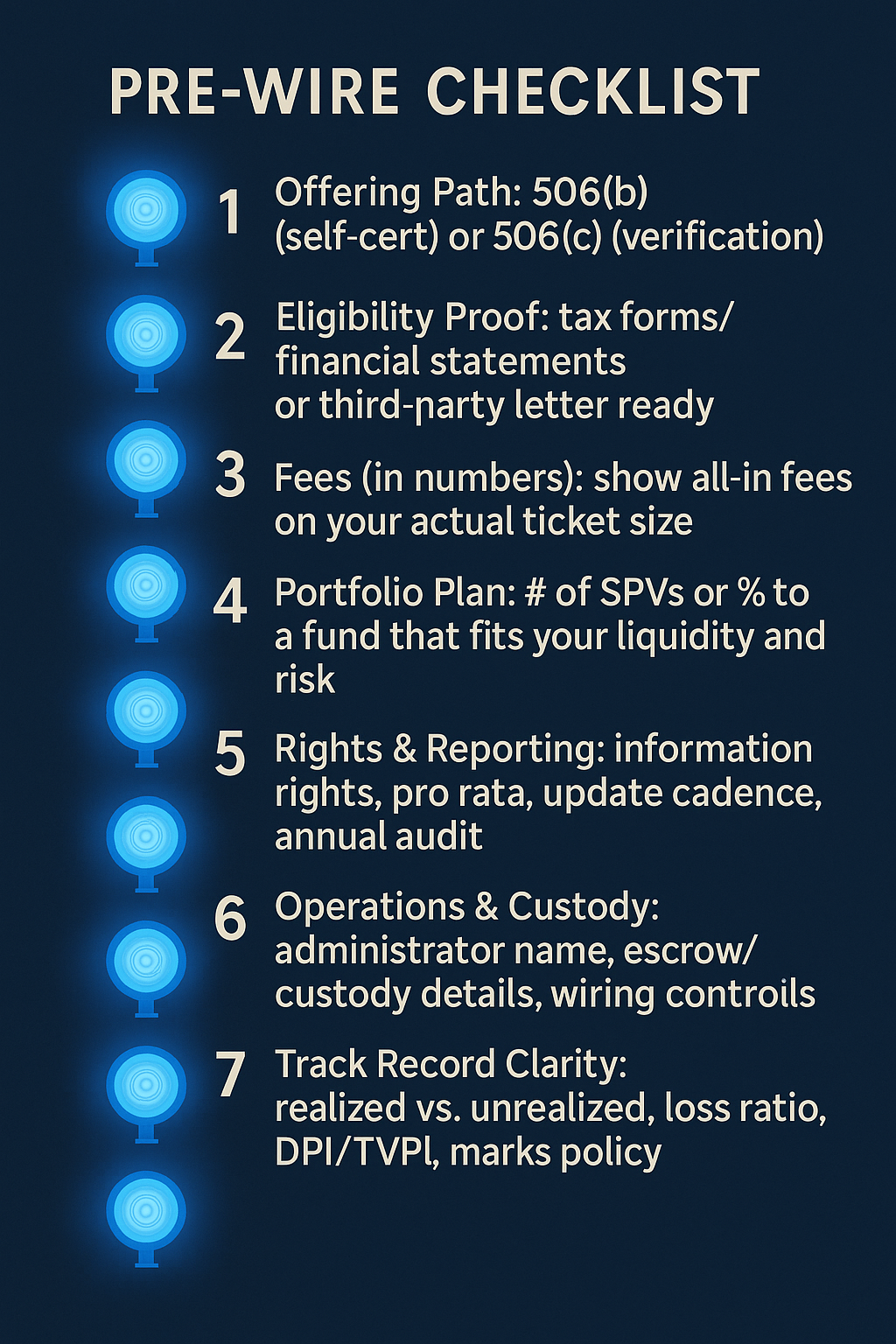

A quick pre-wire checklist

- Offering path: 506(b) (self-cert) or 506(c) (verification)?

- Eligibility proof: Tax forms, statements, or third-party letter ready?

- Fees (in numbers): Show the math on a ticket size you’d actually write.

- Portfolio plan: How many SPVs—or what % to a fund—fits your liquidity and risk?

- Rights & reporting: Information rights, pro-rata, update cadence, annual audit.

- Ops plumbing: Who’s the administrator? Where are funds held?

- Track record clarity: Realized vs. unrealized, loss ratio, DPI/TVPI, and how marks are set.

Bottom line

Accredited-investor rules aren’t just gatekeeping—they aim to match risk with wherewithal. If you qualify, you can enter through funds, syndicates/SPVs, rolling vehicles, or direct checks, each with tradeoffs in access, control, diversification, and cost. Move methodically: know how you qualify, understand the offering path, and insist on clear fee math and reporting. Do that, and the “accredited” label becomes a helpful filter for building a venture portfolio that fits your goals and risk tolerance.

{kind=link}