This Content Is Free After You Enter Your Email

When it comes to retirement planning, one of the biggest advantages of a Traditional IRA is the potential for tax-deductible contributions. Understanding how these deductions work—and who qualifies—can help you maximize your retirement savings and reduce your current-year tax burden. This guide breaks it down in clear, approachable terms.

What Does “Tax Deductible” Mean?

A tax deduction reduces your taxable income for the year. If you earn $60,000 and contribute $6,000 to a Traditional IRA, your taxable income may drop to $54,000—assuming you meet the rules for deductibility. The result? You pay less in federal income taxes for that year, leaving more money in your pocket to invest for the future.

Who Can Deduct Contributions?

The rules for deducting Traditional IRA contributions depend on three main factors:

- Your filing status

- Your income level

- Whether you or your spouse participate in a workplace retirement plan

Here’s how these factors interact:

1. Single Filers

If you do not participate in a workplace retirement plan, you can deduct the full contribution regardless of income.

If you do participate in a workplace plan (like a 401(k)), the deduction is limited based on your modified adjusted gross income (MAGI):

- Full deduction: MAGI ≤ $79,000

- Partial deduction: $79,001 – $89,000

- No deduction: MAGI ≥ $89,000

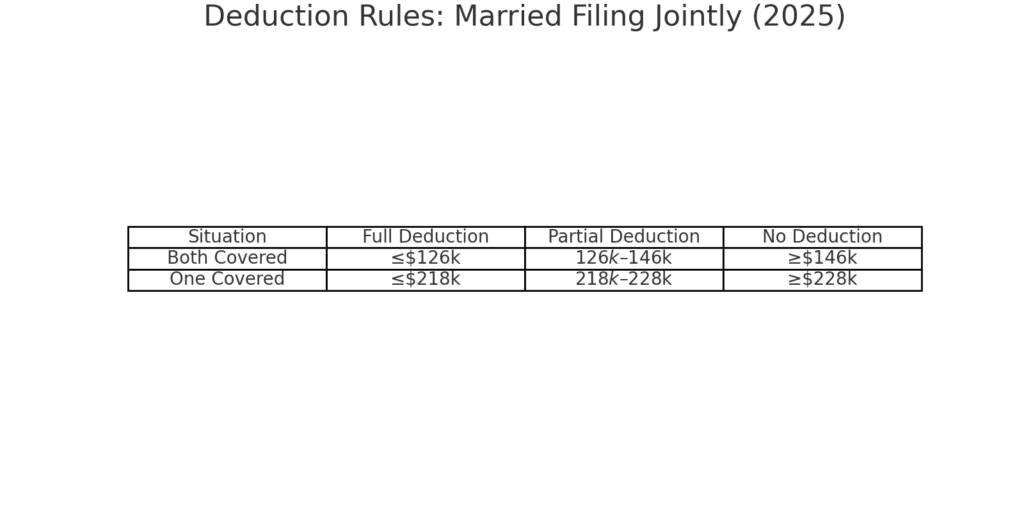

2. Married Filing Jointly

The rules change slightly if you’re married and filing jointly:

- Both spouses covered by a workplace plan:

- Full deduction: MAGI ≤ $126,000

- Partial deduction: $126,001 – $146,000

- No deduction: MAGI ≥ $146,000

- Only one spouse covered by a workplace plan:

- Non-covered spouse can deduct contributions fully if household MAGI ≤ $218,000

- Partial deduction: $218,001 – $228,000

- No deduction: MAGI ≥ $228,000

3. Married Filing Separately

For those who are married filing separately and lived with their spouse at any point during the year, the deduction phases out very quickly between $0 and $10,000. This is a situation where tax planning becomes more important.

Non-Deductible Contributions

Even if you exceed the income limits, you can still contribute to a Traditional IRA—though the contribution will be non-deductible.

- Non-deductible contributions still grow tax-deferred, meaning you won’t pay taxes on investment gains until you withdraw the money in retirement.

- It’s important to file IRS Form 8606 to track non-deductible contributions. Failing to do so can result in double taxation when you withdraw funds later.

Non-deductible contributions are often used in combination with a backdoor Roth IRA strategy, allowing high earners to enjoy tax-free growth despite income restrictions.

Contribution Limits and Deductibility

For 2025:

- Maximum contribution: $7,000 ($8,000 if age 50 or older)

- Contributions cannot exceed your earned income.

If you contribute the maximum and are eligible for the full deduction, the result is a double benefit: reducing current taxable income while investing for long-term growth.

Why Deductibility Matters

Deductibility is more than just a tax break—it’s a way to supercharge your retirement savings. Here’s why:

- Reducing taxable income allows you to invest more of your earned money.

- Tax-deferred growth accelerates compounding because dividends and interest aren’t taxed each year.

- Over decades, deductible contributions can grow significantly larger than the same contributions in a taxable account.

Example:

- Alex contributes $6,000 annually to a deductible Traditional IRA, earning an average of 7% over 30 years. He reduces his taxable income each year, saving roughly $1,200 annually in taxes. By retirement, his IRA balance could reach $610,000.

- Jordan contributes $6,000 to a taxable brokerage account instead, earning the same 7% annual return. After paying taxes annually on dividends and capital gains, Jordan’s balance may only reach $510,000.

That extra $100,000 comes purely from tax advantages and compounding.

Strategies for Maximizing Deductible Contributions

- Check your eligibility before contributing: Use IRS guidelines or consult a financial advisor to confirm whether your contribution is fully deductible.

- Time contributions strategically: You can make contributions up until the tax-filing deadline (typically April 15 of the following year). This can help reduce your tax bill for the previous year.

- Combine with employer plans: If you have a 401(k) at work, you may still qualify for a partial deduction, depending on your income.

- Consider the backdoor Roth strategy: High-income earners can make non-deductible contributions to a Traditional IRA and then convert to a Roth IRA. This is legal but requires careful reporting.

Common Misconceptions

- “I can’t contribute if I have a 401(k).” False — you can contribute, but deductibility may be limited.

- “I can deduct any amount I contribute.” False — limits are set by both income and IRS contribution caps.

- “Non-deductible contributions aren’t useful.” False — they still grow tax-deferred and can be converted to a Roth IRA later.

Next Steps for Novice Investors

- Determine eligibility: Know your income and workplace retirement plan status.

- Decide contribution amount: Stay within IRS limits and consider catch-up contributions if over 50.

- Select investments wisely: Diversify between stocks, bonds, and funds to maximize growth potential.

- File Form 8606 for non-deductible contributions: Protect yourself from double taxation in the future.

By understanding who can deduct contributions and how to maximize the benefit, a Traditional IRA becomes more than just an account—it’s a tax-efficient tool to grow wealth over decades.

{kind=link}