This Content Is Only For Subscribers

Real estate’s tax efficiency comes from how properties earn cash, how costs are recognized, and how funds are structured. Here’s a concise, plain-English tour of the biggest benefits—now tightened with precise IRS language—plus what to ask managers before you wire. (Educational only, not tax advice.)

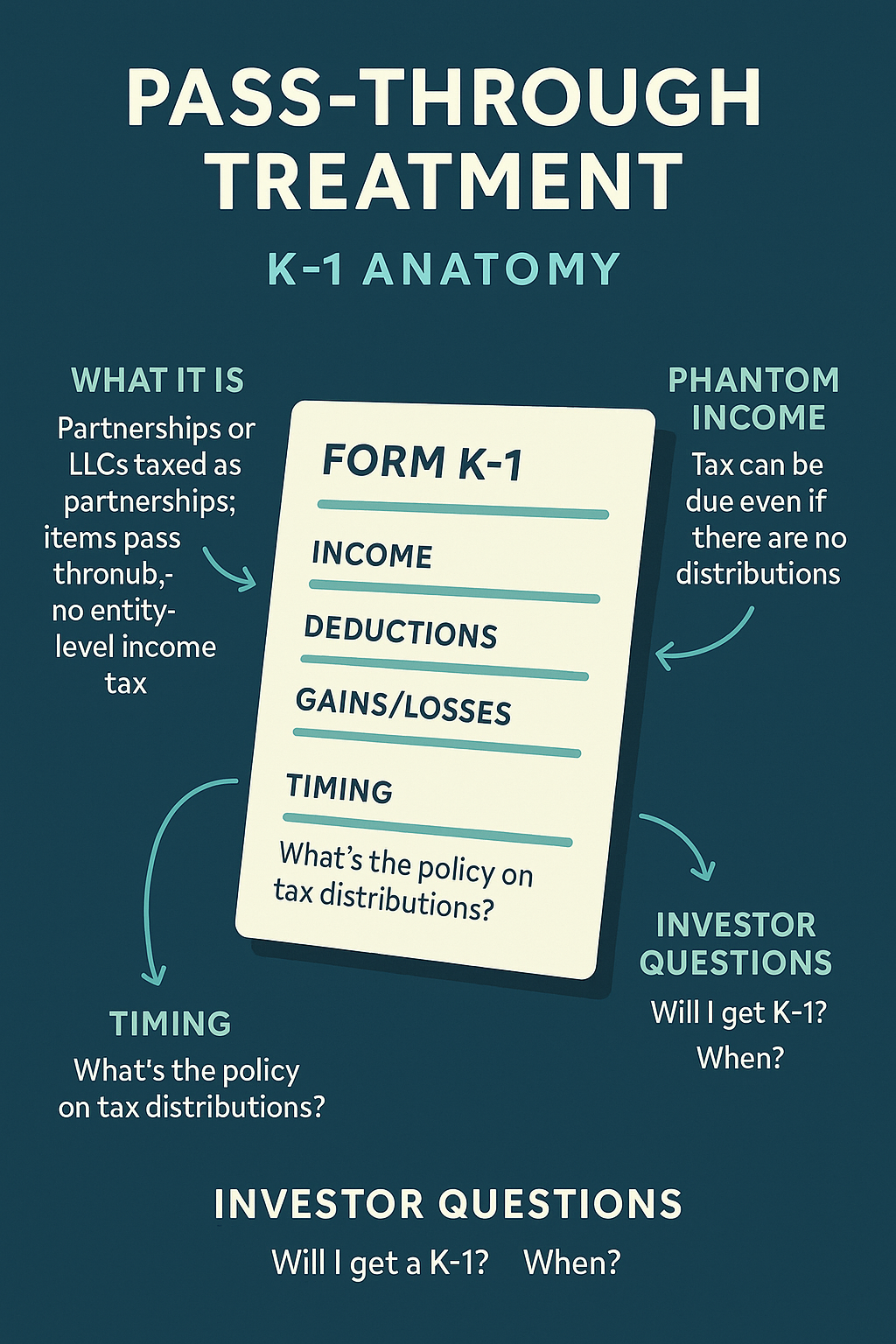

1) Pass-through treatment (no “second tax”)

Most private funds are partnerships (or LLCs taxed as partnerships). Partnerships generally don’t pay an entity-level income tax; items of income, deduction, gain, and loss pass through to partners, who report them on Schedule K-1. Because partners must report their distributive share whether or not cash is distributed, you can face tax without a concurrent payout (often called “phantom income”).

Ask: Will I get a K-1? When? What’s the policy on tax distributions?

2) Depreciation & cost segregation

Depreciation is a non-cash deduction that can shelter rental income. Many managers use cost segregation to identify shorter-lived components (e.g., certain fixtures and site improvements) that depreciate faster, front-loading deductions. You may see cash yield exceed taxable income in early years; at exit, some benefits can be recaptured and taxed differently.

Ask: Do you run cost-seg studies? Roughly what share of cash yield do you expect to shelter annually?

3) Losses (and their limits)

Partnership losses may offset your other passive income, but passive-activity, at-risk, and basis limitations can defer usage until future years or until disposition. If you plan to use losses, confirm how they’re allocated and whether they’re likely to be suspended.

Ask: How are losses allocated? Do you expect suspended losses that free up on sale?

4) Business-interest deduction (section 163(j))

Real estate strategies often use leverage, and interest is generally deductible. Many funds elect the real property trade or business exception under §163(j) to avoid interest-limitation caps. Important: this election is irrevocable and requires using ADS (Alternative Depreciation System) for nonresidential real property, residential rental property, and qualified improvement property—i.e., longer depreciation lives in exchange for fuller interest deductibility.

Ask: Will you make the §163(j) real-property election? How does ADS change depreciation timelines and expected taxable income?

5) REIT wrappers

If you invest through a REIT vehicle (public, non-traded, or private), the tax profile differs:

- REITs must distribute at least 90% of REIT taxable income, which supports steady dividends.

- Individuals may take the up-to-20% §199A deduction on qualified REIT dividends (as reported on 1099-DIV box 5), subject to a holding-period requirement and other rules.

- A REIT dividend can include ordinary income, capital-gains distributions, and return of capital. Return of capital isn’t taxed when paid but reduces your basis, affecting gain on sale.

Ask: What was last year’s dividend mix (ordinary/cap gains/return of capital)? Are payouts generally §199A-eligible?

6) Deferral tools

- Refinances: Cash from new borrowing is typically loan proceeds, not income, so funds can distribute refinance proceeds without immediate tax. Caveats: tax can arise if debt is forgiven later, or if a partnership distribution exceeds your basis.

- Like-kind exchanges (1031): Post-TCJA, 1031 defers gain on real property exchanges at the property-owner level. In commingled funds this is complex; when acquiring from property owners, some managers use UPREIT/OP-unit structures that can facilitate tax deferral when properly structured.

Ask: Will you return capital via refis? Do documents contemplate 1031s or OP-unit deals—and who benefits?

7) Tax-exempt & non-U.S. investors

- Tax-exempt investors (foundations, endowments, IRAs) can incur UBTI (notably from debt-financed income under §514). Many invest through a blocker corporation to prevent UBTI from passing through—accepting some corporate-level tax drag.

- Non-U.S. investors often focus on withholding and ECI exposure; partnerships with ECI must withhold under §1446. Funds may use REITs or blockers and rely on treaties to manage outcomes.

- Multi-state portfolios can trigger state filings.

Ask: Will I face UBTI/ECI? Is there a blocker and what’s the expected drag? What federal/state forms and withholdings should I expect?

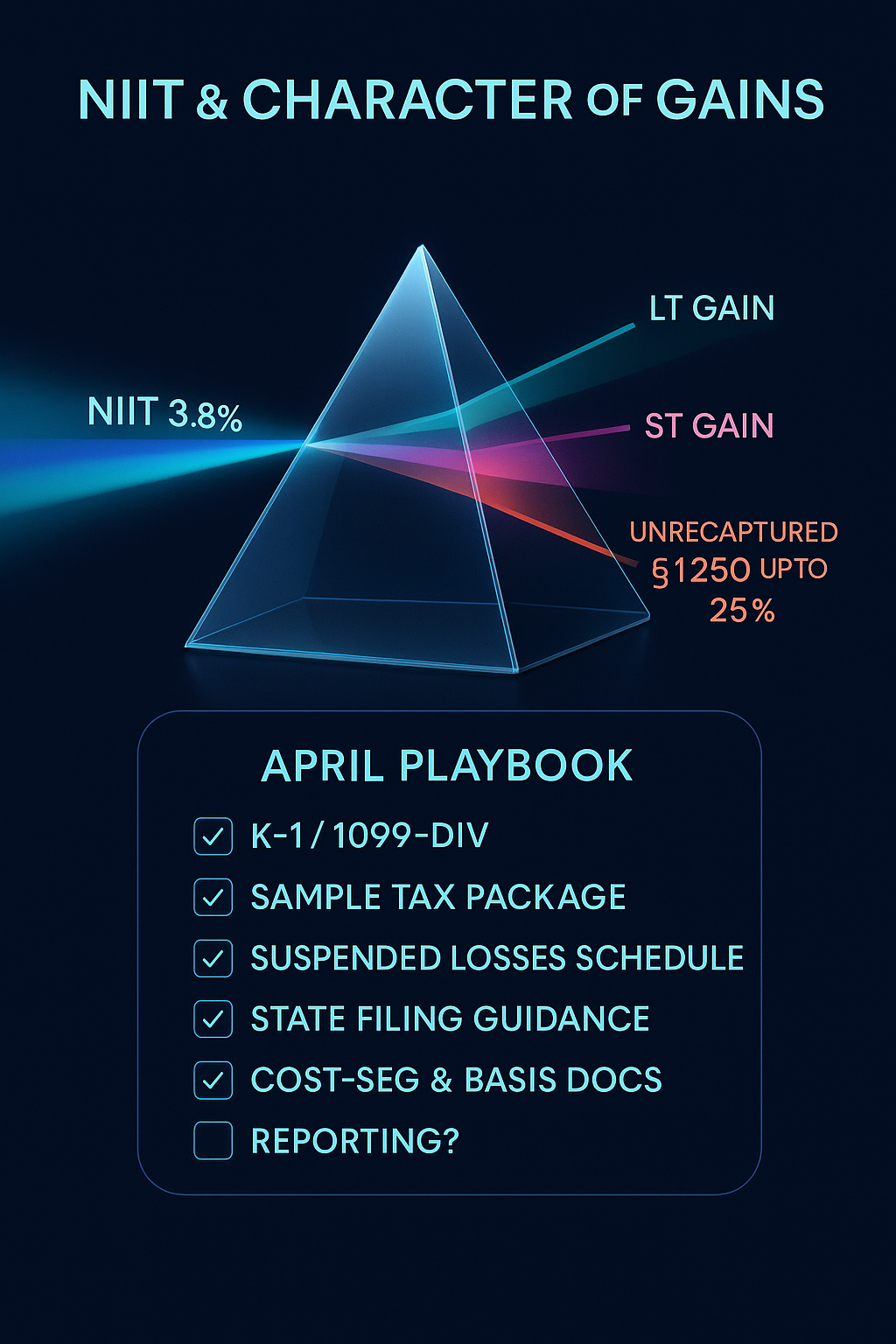

8) NIIT & character of gains

High-income individuals may owe the 3.8% Net Investment Income Tax (NIIT) on passive income and gains. Sales typically generate long-term capital gains if holding periods are met, but the portion attributable to prior depreciation may be unrecaptured §1250 gain (taxed at rates up to 25%). Your K-1 or 1099-DIV will break down these components.

Ask: How will gains be reported (LT/ST, unrecaptured §1250)? What mix do you expect across the fund’s life?

9) Reporting quality = smoother April

Two managers with similar assets can deliver very different tax seasons. The best provide:

- Timely, clean K-1s or 1099-DIVs with clear footnotes,

- State filing guidance for multi-state portfolios,

- Documentation for cost segregation and basis tracking, suspended losses, and gain allocations, and

- A sample tax package during diligence so you know what April looks like.

Ask: When do draft and final packs arrive? Can I see last year’s template (redacted)?

Quick checklist (copy/paste)

- Entity & forms: K-1 or 1099-DIV? Any feeder/blocker?

- Shelter: Expected depreciation and cost-seg vs. cash yield.

- Leverage: §163(j) election status; ADS impact.

- Distributions: Tax-distribution policy; refinance distribution policy and basis impacts.

- Exits: Any 1031/OP-unit usage; who benefits.

- Special investors: UBTI/ECI handling; withholdings; likely state filings.

- Reporting: K-1 timing history; state guidance; prior-year sample.

Bottom line

Real estate funds can be highly tax-efficient: pass-throughs avoid a second tax, depreciation and cost segregationshelter income, REITs support sizable payouts (often with a §199A benefit), and deferral tools reduce current taxes. The fine print decides your outcome. Ask managers to quantify the shelter, explain the §163(j) ADS trade-off, clarify refinance/basis effects, and show last year’s tax package. That’s how you turn a sound real-estate thesis into after-tax results that match your plan.

{kind=link}