This Content Is Only For Subscribers

Venture capital deals look casual—coffee meetings, term sheets, wire instructions—but they sit on top of real securities law. If you’re new to VC, understanding the few core rules will help you read documents faster, spot red flags, and ask better questions. Here’s a plain-English tour of what actually governs fundraising, fund structure, and secondary sales.

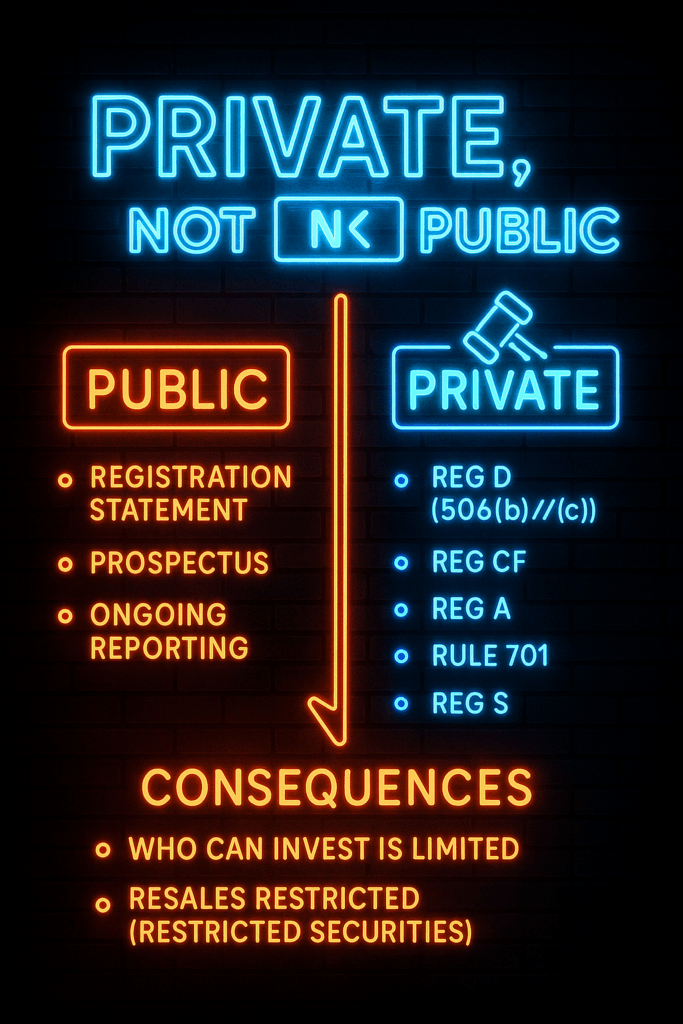

The big picture: private, not public

Venture financings and VC funds almost always sell unregistered securities using private-offering exemptions. That’s the whole game: avoid the cost and delay of a public registration while still protecting investors with disclosure and eligibility rules. Two consequences flow from this:

- Who can invest is limited. Many offerings are open only to accredited investors (and, for some funds, qualified purchasers).

- Resales are restricted. Private shares are generally restricted securities—you can’t flip them freely.

Keep that in mind as you evaluate any deal or fund.

The workhorse exemptions for startups

Regulation D (Rules 506(b) and 506(c)).

These are the bread and butter for priced rounds, SAFEs, and convertible notes.

- 506(b): No general solicitation. Issuers rely on pre-existing relationships; investors usually self-certifyaccredited status.

- 506(c): Issuers may publicly market (websites, podcasts, demo days), but must take reasonable steps to verifyaccreditation—documents or third-party letters, not just a checked box.

Regulation Crowdfunding (Reg CF).

Allows anyone to invest within annual limits through a registered portal. Good for community-driven raises and early traction signals, but offerings are small and disclosures vary.

Regulation A.

A mini-public route with caps and tiered disclosure. Occasionally shows up for growth-stage companies building a consumer base, but it’s not classic VC.

Rule 701 (employee equity).

The go-to exemption for option grants and restricted stock. As the company scales, enhanced disclosures kick in. Sloppy 701 compliance becomes a headache in diligence—worth asking founders whether they track limits and provide required materials.

Regulation S (offshore sales).

Allows sales outside the U.S. to non-U.S. persons, with conditions. You’ll see Reg S when multinationals or global angels come into a round.

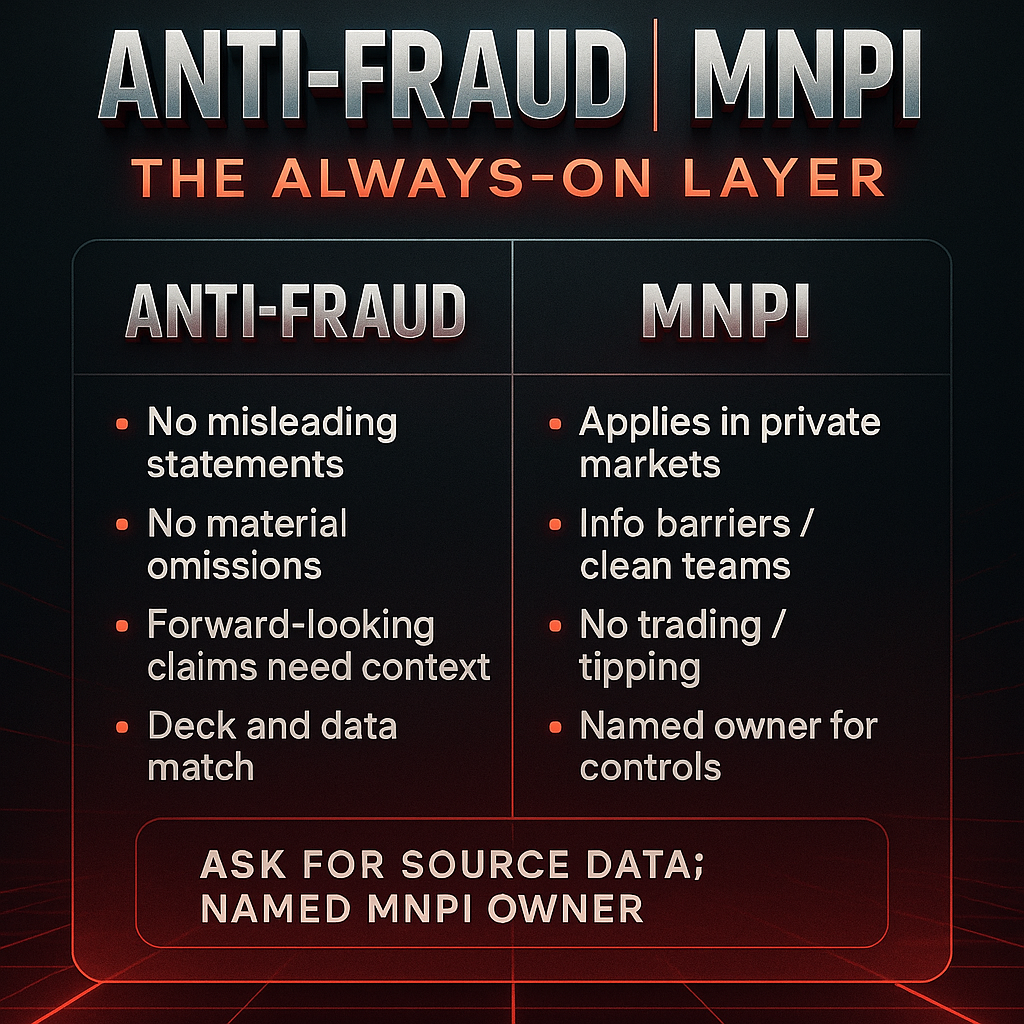

Anti-fraud is the north star

Regardless of the exemption, the anti-fraud rules always apply. No misleading statements, no material omissions. In practice, this means decks and data rooms must match reality; forward-looking claims need context; and if the company knows about a landmine (a big churn event, a key customer at risk), it should disclose it. As an investor, ask for source data behind big charts and a clear explanation of risks.

VC funds: why they’re “private funds,” not mutual funds

Funds side-step mutual-fund regulation by relying on Investment Company Act exclusions:

- 3(c)(1): Limits the number of beneficial owners (with a higher cap for certain qualifying VC funds) and forbids public offerings.

- 3(c)(7): Allows an unlimited number of qualified purchasers (a higher wealth threshold), still private.

The fund’s offering typically uses Reg D (often 506(b) or 506(c)), while its status under the Investment Company Act rests on 3(c)(1) or 3(c)(7). That’s why you’ll see two sets of eligibility questions in the subscription packet.

Who polices the managers: the Advisers Act

The investment adviser (the management company behind the GP) is the regulated actor. Many pure VC firms rely on the venture capital adviser exemption and file as Exempt Reporting Advisers (ERAs); others register fully as investment advisers.

Common threads either way:

- Fiduciary duty. Act in clients’ best interests, disclose and manage conflicts, and don’t mislead.

- Marketing discipline. Modern rules permit testimonials/endorsements and third-party ratings with conditions; any performance shown must be fair, balanced, and backed by records.

- Books and records. If it’s in the deck, there should be workpapers to prove it.

- Custody safeguards. Many managers deliver annual audits to investors and use independent admins as a control.

For LPs, a quick test is document consistency: do the PPM, LPA, and Form ADV tell the same story as the pitch?

State “blue sky” still matters

Even with federal preemption for common private-offering routes, most issuers must file state notices and pay fees where investors reside. It’s administrative, but it’s part of a clean raise. If you’re an angel, expect a line in the doc authorizing the issuer to make those filings using your info.

Secondary sales: the rules don’t disappear

As companies mature, employees and early investors look to sell. Remember:

- Shares remain restricted. Transfer often requires company consent, right-of-first-refusal waivers, and representations about buyer eligibility.

- Information rights matter. Buyers need current information—without it, sellers risk claims of selective disclosure.

- Tender offers (multiple holders selling within a set window) trigger special notice and timing rules.

- For institutions, Rule 144 and 144A may come up, but for most private-company stock the gating items are company consent and eligibility.

If you’re buying in a secondary, ask who has control of the process, how insider information is handled, and what representations the company will make.

MNPI and insider trading—yes, in private markets

Material non-public information (MNPI) isn’t just a public-markets concept. In private rounds, you may see forecasts, pipeline details, or pending partnership docs. Trading (or tipping others) while holding MNPI—even in private company shares—can create liability. Quality managers run information barriers, clean-team protocols, and written MNPI controls across their funds and co-investors.

What to look for in documents (fast checklist)

For startup rounds

- Exemption route: 506(b) or 506(c)? Any Reg S participants?

- Use of proceeds: Clear and realistic?

- Disclosure set: Financials, key risks, customer concentration, churn or regulatory exposure.

- Employee equity/Rule 701: On top of limits and enhanced disclosures?

For VC funds

- Investment Company Act path: 3(c)(1) or 3(c)(7) (and which eligibility test applies to you).

- Adviser status: ERA or RIA? Who’s the CCO?

- Marketing claims: Net vs. gross performance, vintage/benchmark definition, and proof on request.

- Controls: Auditor, independent admin, valuation committee, audit delivery cadence.

Practical red flags (and green lights)

Red flags

- Vague exemption language (“raising privately” with no specifics).

- Performance slides without footnotes or a clear net-of-fee view.

- Casual handling of MNPI in a competitive process.

- Employee equity that ignores Rule 701 limits or disclosures.

- Secondary sales with unclear consent, legends, or information rights.

Green lights

- A one-page offering map (exemption, eligibility, blue-sky plan).

- Clean, consistent PPM/LPA/ADV set with tracked changes since last exam.

- A sample workpaper pack backing performance and any “top-quartile” claims.

- Clear MNPI controls and a named person accountable for them.

- Straight answers on state notices, transfer restrictions, and audit timing.

Bottom line

Venture capital thrives in the private markets, but “private” doesn’t mean “anything goes.” A small set of rules—Reg D, Rule 701, anti-fraud principles, Investment Company Act exclusions, and the Advisers Act—do most of the heavy lifting. Learn how those pieces fit and you’ll read term sheets and fund decks with sharper eyes, avoid avoidable mistakes, and spend your energy where it belongs: assessing the team, the market, and the plan.

{kind=link}