This Content Is Only For Subscribers

At first glance, a Roth IRA and a Roth 401(k) look almost identical. Both let you contribute after-tax money, watch it grow tax-free, and take tax-free withdrawals in retirement. But while their tax treatment is the same, their rules, limits, and flexibility differ in important ways.

For anyone building a retirement plan, knowing the differences between a Roth IRA and a Roth 401(k) can help you decide which account—or which combination—best fits your situation.

Shared Features

Both Roth IRAs and Roth 401(k)s share the same basic tax advantages:

- After-tax contributions. You don’t get a tax deduction upfront.

- Tax-free growth. Investment gains, dividends, and interest grow without annual taxation.

- Qualified withdrawals are tax-free. After age 59½ and five years since your first Roth contribution, your withdrawals are tax-free.

These similarities make both accounts powerful tools for long-term planning.

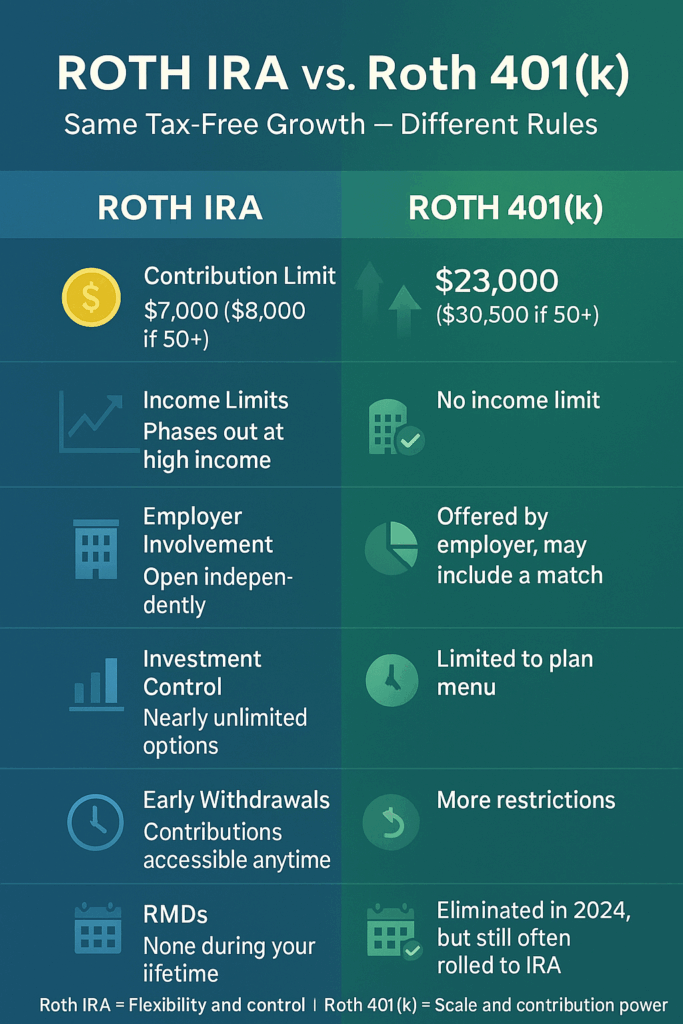

Contribution Limits

This is where Roth 401(k)s blow Roth IRAs out of the water.

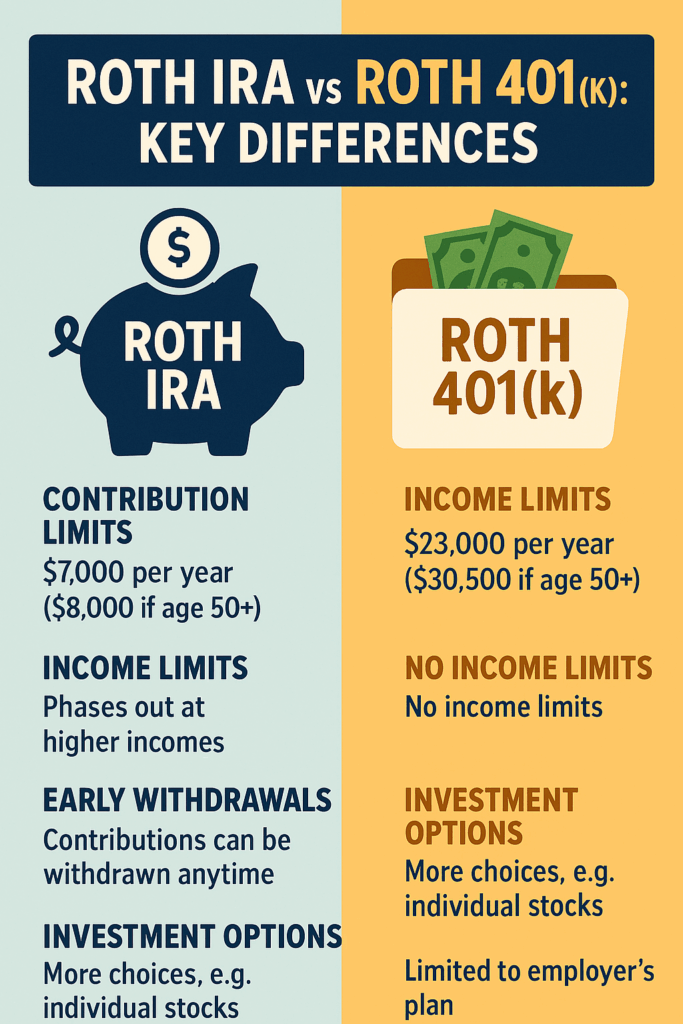

- Roth IRA (2024): $7,000 per year ($8,000 if age 50+).

- Roth 401(k) (2024): $23,000 per year ($30,500 if age 50+).

That’s more than triple the annual contribution room, making Roth 401(k)s especially valuable for high earners or super-savers.

Example

If you max out a Roth IRA for 30 years at $7,000, earning 7%, you’ll have about $710,000.

If you max out a Roth 401(k) for 30 years at $23,000, you’ll have about $2.3 million.

Income Eligibility

- Roth IRA: Contributions are phased out at higher incomes. In 2024, singles phase out between $146,000–$161,000; married couples between $230,000–$240,000.

- Roth 401(k): No income limits. Even if you earn $500,000, you can still contribute.

Bottom line: If your income is too high for a Roth IRA, the Roth 401(k) is your easiest route into Roth savings.

Employer Involvement and Matches

- Roth IRA: You open and fund it yourself, usually at a brokerage. No employer involvement.

- Roth 401(k): Offered through an employer’s retirement plan. Employers often match contributions—but here’s the nuance:

- Historically, matches always went into a pre-tax 401(k) account.

- Since SECURE 2.0 (2022), employers may allow matches or nonelective contributions to be made as Roth (taxable to you in the year received).

That means you could end up with two accounts: a pre-tax 401(k) and a Roth 401(k).

Investment Options

- Roth IRA: Wide open. You can choose virtually any stock, bond, ETF, or mutual fund offered by your custodian.

- Roth 401(k): Limited to the investment menu chosen by your employer’s plan. Options are usually fewer, and sometimes fees are higher.

If you want ultimate control, the Roth IRA is the clear winner.

Required Minimum Distributions (RMDs)

Here’s where a big rule change matters.

- Roth IRA: No lifetime RMDs for the original owner. You can let it grow untouched as long as you live.

- Roth 401(k): Prior to 2024, Roth 401(k)s did require RMDs. But under the SECURE 2.0 Act, RMDs are eliminated starting in 2024.

Even so, many people still roll Roth 401(k)s into Roth IRAs at retirement for simplicity, to consolidate accounts, and to avoid dealing with multiple five-year clocks.

Early Withdrawals

Both Roth IRAs and Roth 401(k)s impose penalties if you tap earnings before age 59½ (unless you qualify for an exception). But there’s a key difference:

- Roth IRA: Contributions can be withdrawn anytime, tax- and penalty-free.

- Roth 401(k): Access is more restricted. You generally can’t withdraw contributions early without triggering penalties, unless your plan allows in-service withdrawals, loans, or hardship distributions.

This makes Roth IRAs far more flexible for emergencies or early retirement strategies.

The Five-Year Rule

Both accounts follow the five-year rule for tax-free withdrawals, but the clocks are separate.

- A Roth IRA’s five-year clock starts with your first-ever Roth IRA contribution, and applies across all IRAs you own.

- A Roth 401(k)’s five-year clock is plan-specific. If you have multiple Roth 401(k)s at different jobs, each one may have its own five-year period.

- When you roll a Roth 401(k) into a Roth IRA, the Roth IRA’s clock controls future withdrawals.

Fees and Control

- Roth IRA: You choose the brokerage, and typically pay minimal fees if you pick low-cost funds.

- Roth 401(k): Plan fees vary. Some are low-cost, others charge higher administrative or fund expenses.

Best Uses for Each

Roth IRA

- Ideal if you want investment flexibility.

- Great for early retirement because contributions are always accessible.

- Excellent estate-planning tool—no RMDs, flexible for heirs.

Roth 401(k)

- Best for high earners who want to contribute more than the IRA limit.

- Essential if your employer offers a match (especially now that some plans allow Roth matches).

- No income restrictions, making it universally available.

Should You Have Both?

For many people, the answer is yes.

- Contribute enough to your Roth 401(k) to get the employer match.

- Max out your Roth IRA if eligible for broader investment choices and withdrawal flexibility.

- If you still have more to save, go back and increase your Roth 401(k) contributions.

This “layered” approach lets you maximize tax-free growth while balancing flexibility and contribution power.

Final Thoughts

Roth IRAs and Roth 401(k)s share the same tax-free superpower, but they play different roles in a retirement plan. The Roth IRA gives you flexibility, control, and estate-planning advantages. The Roth 401(k) gives you scale, high contribution limits, and access regardless of income.

With SECURE 2.0 eliminating RMDs from Roth 401(k)s and allowing Roth employer contributions, the differences have narrowed—but each account still shines in its own way. Using them together can help you build a retirement strategy that balances tax efficiency, growth, and flexibility.

{kind=link}