When you read headlines about venture capital firms pouring millions into startups, it’s easy to picture a group of investors writing giant checks out of personal wealth. In reality, venture capital (VC) operates on a clear structure that governs how money is raised, deployed, and returned.

For investors considering exposure to VC, understanding the roles of limited partners (LPs), general partners (GPs), and the mechanics of term sheets is essential. These aren’t just industry buzzwords—they’re the backbone of how venture capital works and what determines whether investors ultimately see returns.

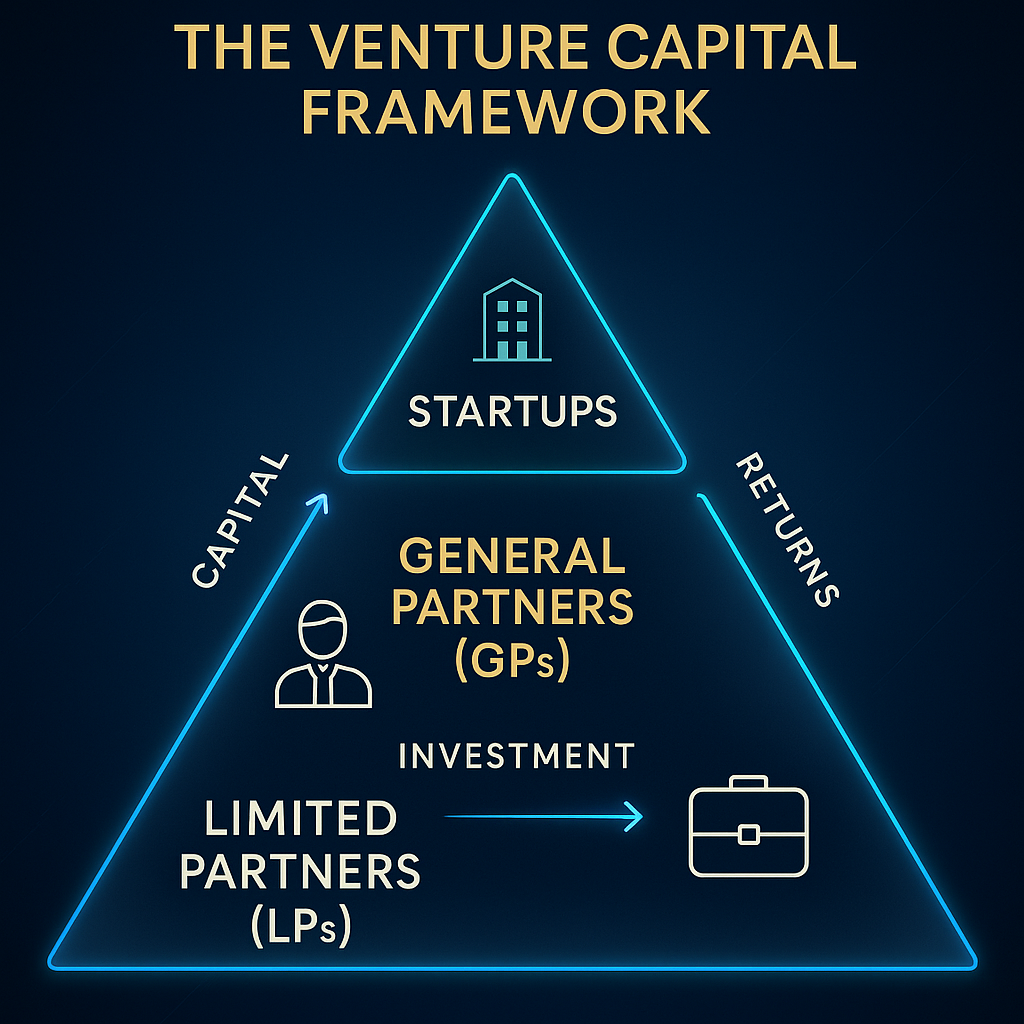

The Players: LPs and GPs

At the heart of every VC fund are two groups: limited partners (LPs) and general partners (GPs).

Limited Partners (LPs):

LPs provide most of the capital. They are usually large institutional investors—pension funds, endowments, sovereign wealth funds, family offices—or wealthy individuals. LPs commit money to a fund with the understanding it will be invested over 10 years or so, and they’ll receive a share of the profits if things go well.

LPs are “limited” because their liability is capped at the amount they invest. They don’t manage the fund day to day. Instead, they trust the general partners to deploy capital wisely.

General Partners (GPs):

The GPs are the fund managers. They decide which startups to back, negotiate deal terms, and actively support portfolio companies. They also have fiduciary responsibility to act in LPs’ best interest.

To show commitment, GPs typically invest some of their own money—often 1% to 5% of the fund. This “skin in the game” aligns their incentives with LPs. If the portfolio succeeds, GPs profit alongside their investors.

How VC Funds Make Money

The standard compensation model in venture capital is the “2 and 20” rule:

- 2% Management Fee: Paid annually on assets under management, covering salaries and operating costs.

- 20% Carried Interest (Carry): A share of profits GPs keep once returns exceed a threshold, often called the hurdle rate.

For example, if a $100 million VC fund doubles to $200 million, GPs might keep around $20 million as carry. LPs get the rest.

This system rewards GPs for generating real returns, not just raising large funds.

The Fund Lifecycle

VC funds typically follow a 10-year cycle:

- Fundraising (Years 0–1): GPs pitch the fund to LPs, raising commitments.

- Investment Period (Years 1–5): Capital is called from LPs and deployed into startups.

- Growth and Monitoring (Years 3–8): GPs work with portfolio companies to scale, expand, and prepare for exits.

- Exits and Returns (Years 5–10): The fund realizes gains through IPOs, acquisitions, or secondary sales. Profits are distributed back to LPs, with GPs receiving carry.

For LPs, this means capital is locked up for years. Liquidity is limited, which is why only investors who can afford patience typically participate.

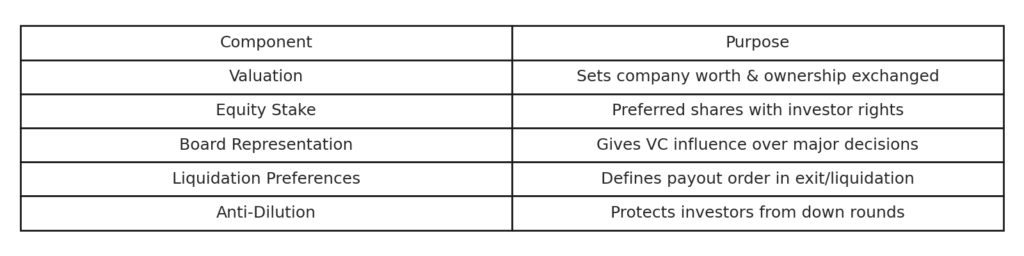

The Importance of Term Sheets

While LPs and GPs set the stage for VC funds, term sheets are where the rubber meets the road in startup deals. A term sheet is a non-binding agreement outlining key terms of an investment.

Some of the most important components include:

- Valuation: Determines company worth and ownership exchanged.

- Equity Stake: Usually preferred shares, giving investors rights beyond common stock.

- Board Representation: Many VCs negotiate for a seat to influence major decisions.

- Liquidation Preferences: Define who gets paid first if the company sells or liquidates.

- Anti-Dilution Provisions: Protect investors if future rounds are at lower valuations.

Though non-binding, term sheets set the tone for negotiations and are usually followed by binding contracts.

Why Structure Matters to Investors

For investors considering VC, understanding fund structure is critical:

- Alignment of Interests: Knowing how GPs get paid helps assess whether incentives align with performance.

- Risk Management: Liquidation preferences and anti-dilution clauses protect downside risks.

- Return Potential: Fee structures directly impact net returns to LPs.

- Governance: Board seats and voting rights influence company direction.

The mechanics behind the scenes often matter as much as the startups themselves.

Final Thoughts

Venture capital may look glamorous from the outside, but its inner workings rely on careful structuring. LPs supply capital, GPs manage it, and term sheets define deals. Without this framework, the high-risk, high-reward world of startup investing would collapse into chaos.

For investors considering venture capital exposure, understanding these dynamics is the first step. It demystifies where money flows, how incentives align, and what protections are in place. As highlighted in What Is Venture Capital? A Deep Dive into Startup Investing, knowing the structure behind the headlines is essential for anyone serious about this asset class.

{kind=link}