This Content Is Only For Subscribers

Private equity (PE) fundraising isn’t just roadshows and slide decks. It’s a carefully choreographed process shaped by securities laws, marketing rules, investor-eligibility tests, and cross-border distribution regimes. If you’re newer to the space, think of regulation as the “guardrails” that keep fundraising fair, accurate, and targeted to the right audience. Here’s a plain-English tour of how those guardrails work—and how they affect what you see, sign, and receive as an investor.

Who you can market to (and how)

Private placements, not public offerings.

Most PE funds raise capital through private placements. In practice, that means two common pathways:

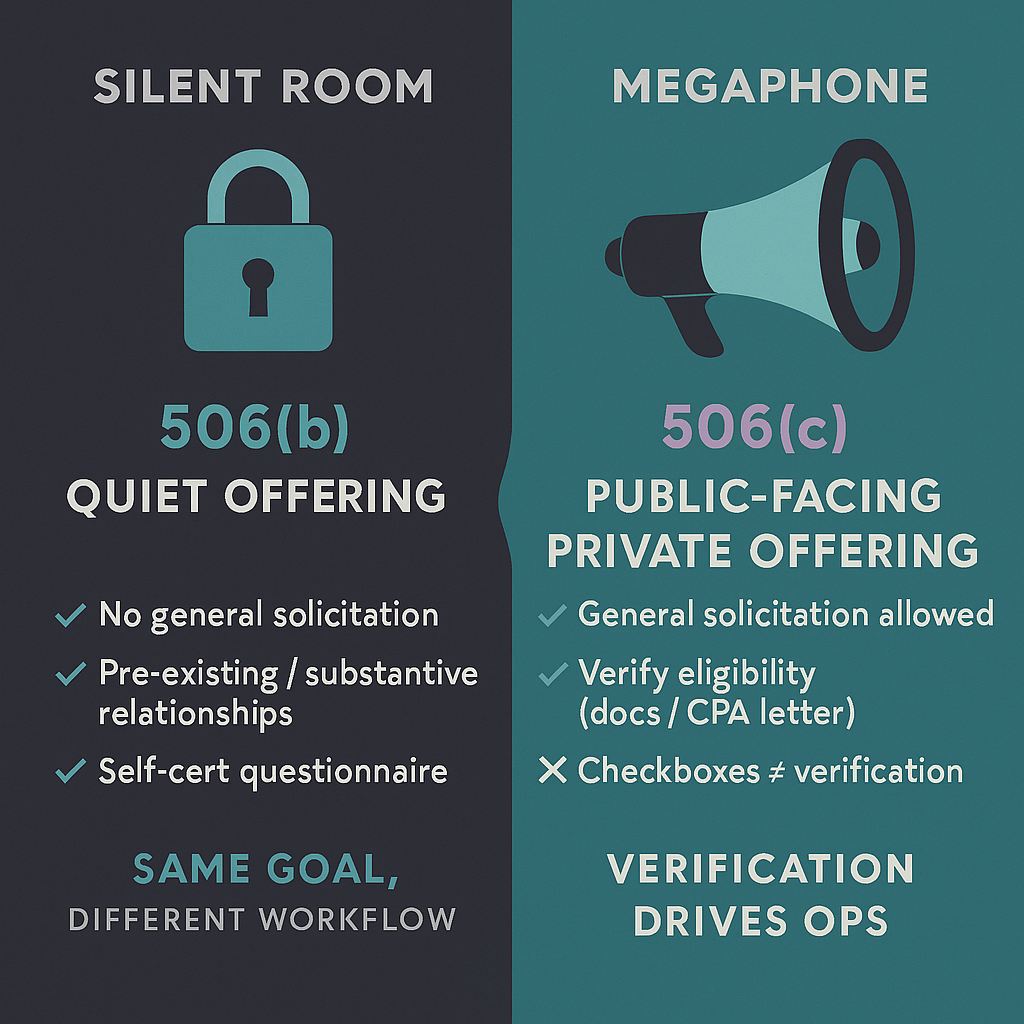

- Quiet offering (often called 506(b)): No general solicitation. Managers rely on pre-existing, substantive relationships with investors. You’ll typically self-certify eligibility in a questionnaire, and the offering will feel “invite only.”

- Public-facing private offering (often called 506(c)): General solicitation is allowed (webinars, websites, conferences), but the manager must take reasonable steps to verify you meet the required investor thresholds. That usually means document checks (W-2s, K-1s, statements) or a verification letter from a CPA/attorney—checkboxes alone don’t cut it.

Eligibility standards.

You’ll encounter different gates depending on the fund’s structure:

- Accredited investor: Income/net worth–based standards, plus certain professional licenses and entity tests.

- Qualified purchaser: A higher bar based on the amount of “investments”—often applies when funds use specific exclusions under the Investment Company Act.

Some funds accept only one category; others accept multiple via different feeder vehicles or share classes. Always check the term sheet before you spend diligence time.

What can be said (and proven)

Marketing rule basics.

Modern advertising rules allow testimonials, endorsements, and third-party ratings—but with conditions and disclosures. If a deck or website shows performance, it must be fair and balanced, and the manager must be able to substantiate every material claim (think: “top quartile,” “alpha,” win rates, hypothetical/model results). Behind the scenes, strong managers keep workpapers, calculation files, and policy memos to back up what you read.

No bait-and-switch.

Fund documents—the private placement memorandum (PPM) and the limited partnership agreement (LPA/LLC agreement)—are the rulebook. If a slide deck promises fee offsets or specific reporting and the PPM/LPA is silent (or different), the documents win. Regulators and diligent LPs look for consistency across the deck, PPM, LPA, side letters, and Form ADV.

Fees, expenses, and the fine print

Regulators focus heavily on what investors were told versus what actually happens. During fundraising, that translates into clearer descriptions of:

- Management fees (rates, step-downs, fee holidays).

- Carried interest (preferred return, catch-up, clawback mechanics).

- Portfolio-company fees (monitoring, transaction) and offsets against management fees—key for your net cost.

- Broken-deal costs and how they’re allocated across funds and co-investments.

- Organizational expenses (who pays the lawyers, auditors, and placement agents, and caps if any).

If a manager can’t walk you through a real, numeric example—preferably from a prior fund—slow down.

Side letters, MFN, and fairness

Large investors often negotiate side letters for reporting, fee breaks, or capacity. Well-run funds offer a most-favored-nation (MFN) process so similarly situated investors can elect comparable negotiated terms. During fundraising, ask:

- What categories of side-letter terms exist?

- Will my commitment size/class be covered by MFN?

- How are side-letter obligations tracked and enforced?

MFN logistics matter; they reduce the risk that two investors in the same class live under two different rulebooks.

Placement agents, “pay-to-play,” and conflicts

If a fund uses a placement agent, you should know who pays them (the fund, the GP, or both), how much, and whether fees are offset against management fees. Public-plan investors and certain jurisdictions have strict pay-to-play and lobbying rules that affect who can solicit whom and on what terms. Quality managers surface these constraints proactively and mirror the rules in their compliance calendar.

ERISA and “plan asset” considerations

If public pensions or other ERISA plans are in the LP base, the fund will manage plan-asset risk—typically by keeping benefit-plan participation below thresholds or by qualifying for exceptions (like VCOC for operating-company investors). You’ll see ERISA addenda in the subscription documents and sometimes bespoke reporting in side letters. For you, the takeaway is simple: ERISA-savvy funds design the structure at formation, not after first close.

Cross-border fundraising: same melody, different lyrics

Europe (AIFMD) and the UK.

In the EU, managers are regulated under the AIFMD framework; non-EU managers often market through national private placement regimes (NPPR) to professional investors country by country. Expect local filings, specific disclosures, and periodic reporting. The UK runs a separate, AIFMD-style regime with its own notices and investor-classification rules.

Asia-Pacific and the Middle East.

Most markets use professional/institutional investor categories and require local notices or licenses for marketing. In some places, “pre-marketing” is itself regulated. A global raise often staggers closes by region to align with filing calendars and document localization.

Common thread: distribution is local. A good counsel team will produce a jurisdiction matrix listing who you can contact, what you can send, and when you can accept commitments.

AML/KYC, sanctions, and tax reporting

Every serious fund bakes in AML/KYC screening (identity, source of funds), sanctions checks, and tax documentation (W-8/W-9 for U.S. purposes). Offshore feeders and many administrators also handle FATCA/CRS information reporting. It’s routine, but investors must keep forms current. Delays here can hold up closings even when investment committees are ready to wire.

Digital fundraising and data discipline

Online platforms and virtual data rooms are common—even for institutional raises. The compliance bar doesn’t drop just because the medium changes:

- Public web pages used in a 506(c) raise require verification processes.

- Any performance shared must be supported and consistent with governing documents.

- Access controls, clean-team protocols, and data-privacy filters still apply—especially when marketing across borders.

Timelines that actually work

A realistic fundraising calendar builds in:

- Pre-flight checks (policies, performance backup, fee examples, conflicts log).

- Document alignment across deck, PPM, LPA, ADV, and side-letter templates.

- Eligibility and verification workflows (self-cert vs. third-party verification).

- Jurisdictional sequencing for EU/UK/Asia notices and NPPR filings.

- Ops readiness for AML/KYC, sanctions, and tax forms at scale.

- Investor reporting preview—sample quarterly letter, fee/expense template, and audit timeline.

Managers who can’t show this scaffolding often slip schedules at first close.

A quick diligence checklist (as an LP)

- Offering path: Quiet (relationship-based) or general solicitation? What’s the eligibility test and verification method?

- Documents: Do the deck, PPM, LPA, and ADV tell the same story on strategy, fees, and risks?

- Performance support: Can the manager show the work behind net returns, benchmarks, and any “top-quartile” claims?

- Fees & offsets: Numeric example, including portfolio-company fees and offset mechanics.

- Side letters/MFN: Am I covered, and how are terms administered?

- Placement agent: Who pays and how much? Any offsets? Any pay-to-play implications?

- ERISA plan-asset plan: Threshold management or VCOC/REOC approach?

- Cross-border plan: Where can they market? Which filings are complete or pending?

- AML/KYC & tax docs: Who collects, how long, and what happens if there’s a hit on sanctions screening?

- Reporting rhythm: Sample quarterly letter, fee/expense breakout, audit delivery timeline.

Bottom line

Regulation doesn’t make fundraising harder; it makes it clearer. Guardrails around who can be solicited, what can be said, how fees/expenses are disclosed, and where a fund can market create a more predictable process for everyone. As an investor, use those guardrails as a lens. Ask for document consistency, performance backup, explicit fee math, and a jurisdictional plan. Funds that meet that standard aren’t just safer—they’re usually better run, which is exactly what you want when you’re locking up capital for years.

{kind=link}