This Content Is Only For Subscribers

Venture capital doesn’t grow in a vacuum. In most markets, governments and quasi-public agencies help prime the pump—lowering early-stage risk, attracting talent, and building the pipes that capital and ideas flow through. If you’re new to VC, here’s a clear, practical tour of what those programs look like, why they matter, and how to factor them into investment decisions.

Why governments care

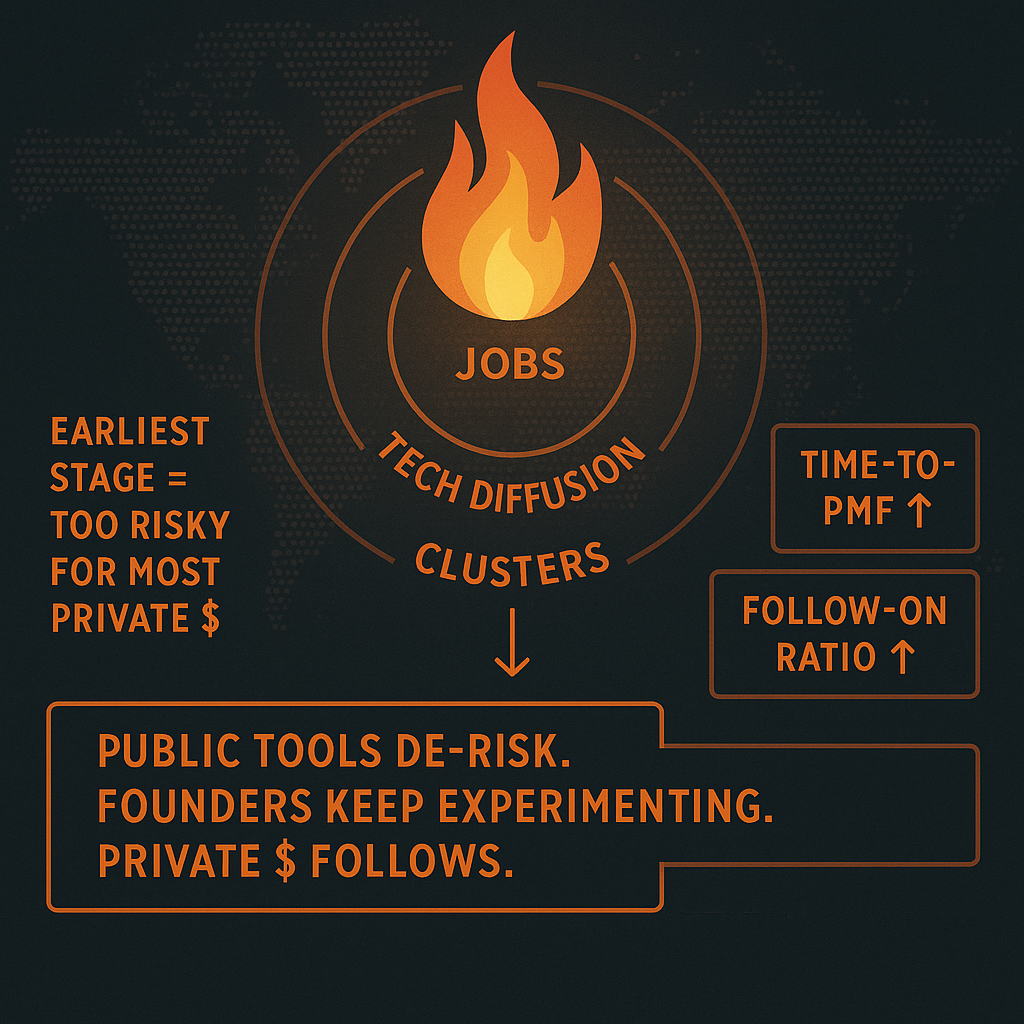

Startups create outsized job growth, push new technologies into the real economy, and can anchor entire industry clusters. The catch is that the earliest stages are too risky for most private money. Public programs step in to de-riskthat gap—so founders keep experimenting and private investors feel confident following with bigger checks.

The main toolkits (plain English version)

1) Non-dilutive funding (grants and contracts).

Cash without equity. Think competitive R&D grants, innovation vouchers, or government procurement pilots. For founders, this stretches runway. For investors, it’s a signal: someone outside the cap table vetted the work. Watch for milestone gates and reporting obligations that can slow teams down.

2) Tax incentives for investors and founders.

Two common styles:

- Investor reliefs (e.g., income-tax relief or capital-gains reductions for investing in young companies). These make seed checks cheaper after tax and can pull new angels into the market.

- Company credits (e.g., R&D tax credits, payroll tax offsets). These act like a rebate for building product and hiring engineers.

3) Co-investment funds and fund-of-funds.

Public money that invests alongside private VCs or into VC funds directly—usually with a “no worse than pari passu” rule to keep alignment. Good programs crowd in more private capital and avoid picking winners; weak ones distort pricing or come with red tape.

4) University and lab tech transfer.

Grants for translational research, proof-of-concept funds, and simpler IP licenses help deep-tech companies get from paper to prototype. As an investor, focus on license terms (field of use, sublicensing, royalties) and assignment rights in a future sale.

5) Talent and visas.

Fast-track founder visas, STEM graduate pathways, and relocation grants help teams assemble in one place. This matters when you’re backing global founders who need to be near customers or capital.

6) Incubators, accelerators, and hubs.

Publicly backed incubators provide subsidized labs, mentors, and procurement intros. Value varies wildly; the best are integrated into local industries (health systems, ports, utilities) that can be first customers.

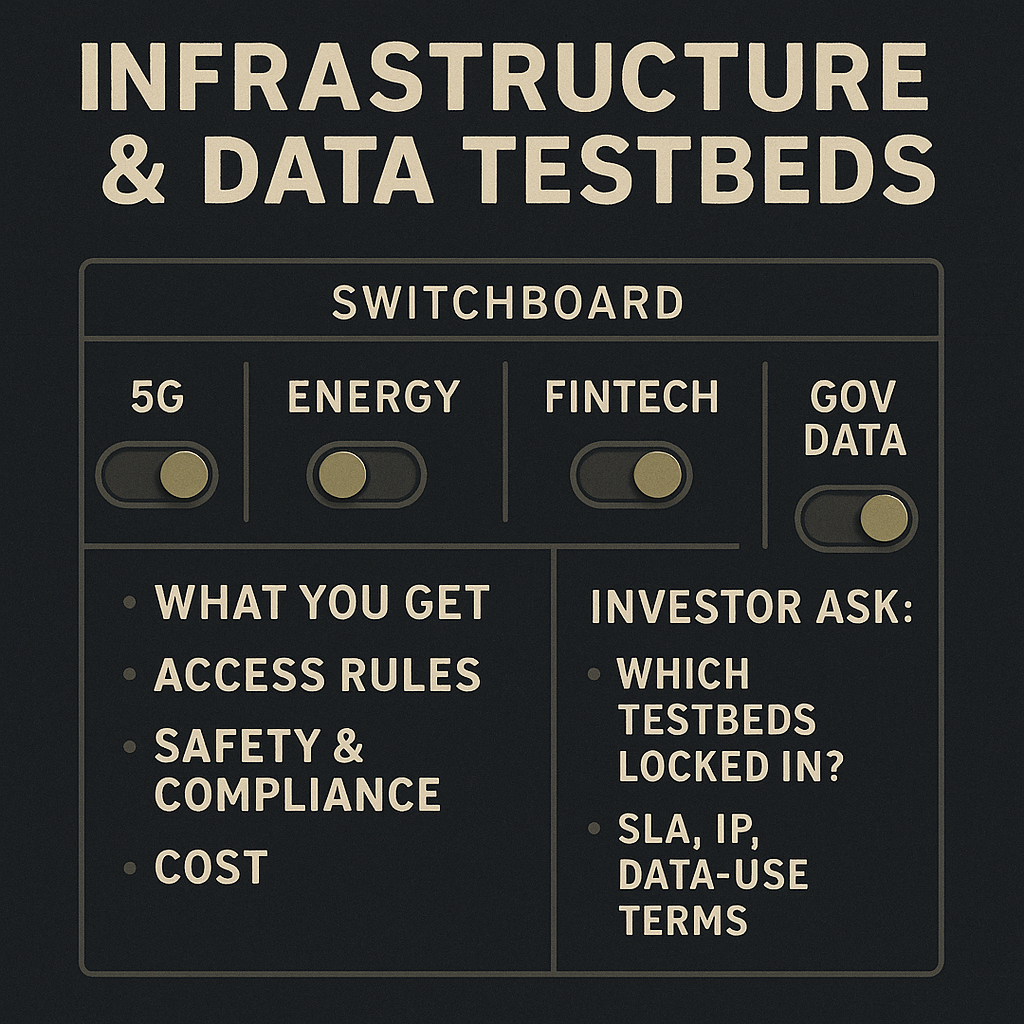

7) Infrastructure and data.

Open testbeds (5G, energy grids, fintech sandboxes), shared labs, and datasets reduce startup costs and time to insight. These are invisible advantages that compound over a portfolio.

How investors should use (and not misuse) these programs

Treat public money like a milestone, not a business model.

A grant proves technical merit; it doesn’t prove go-to-market. Ask how the team converts non-dilutive dollars into customer traction.

Check the strings.

Location requirements, matching-fund rules, reporting loads, export controls, and IP clauses can affect speed and optionality. Make sure management understands compliance; missed filings can trigger clawbacks.

Watch for timeline risk.

Government evaluations and reimbursements run on their own calendars. Ask for a cash-flow plan that assumes delays.

Model the stack.

Founders often layer multiple benefits (grant + tax credit + state match). Confirm what can be stacked, what must be sequenced, and what becomes ineligible once a company scales or pivots.

Follow-on capital still decides the outcome.

Programs can start the fire; private customers and investors keep it burning. Validate the pipeline of non-public funding and the market pull.

Snapshot examples (how this shows up in the wild)

- Non-dilutive R&D: Competitive programs fund feasibility, prototypes, and commercialization steps—especially in deep-tech fields like climate, biotech, and advanced manufacturing.

- Investor tax reliefs: Some countries offer generous upfront income-tax relief or gains exemptions for qualifying angel/seed investments—powerful for first-time investors building a portfolio.

- R&D tax credits: Common in North America and Europe; early companies can receive cash refunds or payroll offsets even pre-profit.

- Public co-investment: National or regional vehicles match private term sheets for local companies or allocate into VC funds to expand the manager base.

- Sovereign/strategic funds: In emerging hubs, state-backed LPs anchor new funds and bring patient capital to sectors of national interest.

You’ll also see targeted programs—climate transition, semiconductors, defense tech, life sciences—where national priorities and venture incentives overlap.

Practical diligence questions (copy/paste)

- What’s the non-dilutive mix? Amount awarded, milestones remaining, and conversion path to customers.

- Any location or eligibility cliffs? What happens if the company hires abroad or opens a second HQ?

- Compliance burden: Reporting frequency, audit risk, and who owns the calendar.

- IP posture: If university-originated, are royalties and sublicensing terms exit-friendly? Any march-in rights?

- Stacking map: Which credits/grants can be combined? Are there caps, time windows, or mutual exclusions?

- Co-investment terms: Truly pari passu with private money? Any vetoes that could slow a sale?

- Follow-on plan: Which private investors are likely to lead the next round if grants stop?

Bottom line

Government programs don’t replace venture capital—they amplify it. The best ecosystems use public tools to lower the cost of experimentation, crowd in private money, and build the connective tissue (talent, labs, data, early customers) that turns research into revenue. As an investor, treat grants, credits, and co-investment as inputs to your thesis, not the thesis itself. If the team can translate policy tailwinds into customer adoption and scalable unit economics, you get the upside: faster learning, less dilution, and a portfolio that compounds on more than luck.

{kind=link}