This Content Is Only For Subscribers

Hedge funds are private by design, but they aren’t a black box. Over the last decade, investor safeguards and transparency practices have matured a lot. If you’re new to the space, the trick is knowing what protections exist, what good transparency looks like, and which questions uncover it fast. This guide keeps it practical and plain-English.

The foundation: duties, disclosures, and exams

Fiduciary duty. Hedge fund advisers owe clients a duty of care (act in investors’ best interests) and a duty of loyalty (identify, disclose, and manage conflicts). That duty sits underneath everything—how trades are allocated, how valuations are set, how fees and expenses are charged, and how performance is presented.

Anti-fraud and marketing rules. Managers must tell the truth, avoid misleading omissions, and substantiate what they say—especially in pitch decks and performance charts. Testimonials, endorsements, third-party ratings, and hypothetical results can appear, but only with guardrails and documentation. If a statistic or claim is in the deck, the manager should be able to show you the work behind it.

Regulatory examinations. Registered advisers are examined periodically. Examiners review policies, emails, trading records, valuation memos, performance backups, and expense allocations. Most exams end with a deficiency letter (fix-it list). How a manager responds—quickly and thoroughly, or defensively and slowly—tells you a lot about culture.

The plumbing that protects you

Independent administration. A strong administrator calculates NAV, processes subscriptions and redemptions, maintains the investor register, and checks fees and performance allocations. Independence is key—administrators are the day-to-day control that keeps numbers honest.

Audited financials. Many funds deliver annual audited financial statements, prepared under recognized accounting standards and signed by a reputable audit firm. Audit timing and the auditor’s hedge-fund experience are both worth asking about.

Custody safeguards. When an adviser or affiliate can access fund assets, rules typically require protections such as qualified custodians and either an annual audit delivered to investors or a surprise exam. These are designed to prevent misuse of assets.

Books and records. If it happened, it should be documented: trades, valuations, marketing claims, expense allocations, emails. Robust records make it harder for errors (or worse) to linger and easier for you to verify what you’re told.

Where transparency really lives

Form ADV. This public brochure explains the adviser’s business, strategies, fees, conflicts, disciplinary history, and key personnel. It isn’t glossy marketing; it’s baseline disclosure in plain English. Read it before you read the deck.

Offering documents. The private placement memorandum (PPM) and partnership/LLC agreement are the rulebook: fees, liquidity, valuation, conflicts, and investor eligibility. If a term matters to you—gates, lockups, side pockets—it should appear here clearly.

Investor communications. Expect a cadence—monthly statements, quarterly letters with commentary and risk/exposure summaries, and annual audited financials. Quality matters: look for attribution (what worked, what didn’t), discussion of risk, and clarity on portfolio positioning.

Valuation governance. For hard-to-price assets, strong programs have documented methodologies, independent price sources when available, valuation committee minutes, and back-testing of exits versus prior marks. If fees are tied to NAV, valuation rigor is investor protection.

Fees and expenses. Beyond management and performance fees, know what the fund pays versus what the adviser pays—research, data, travel, compliance, legal, broken-deal costs. Good managers run to a “no surprises” principle and can show you how allocations are determined and reviewed.

Conflicts management. Conflicts are inevitable—multiple funds, affiliates, cross-trades, principal transactions. The standard isn’t “no conflicts ever,” it’s identify, disclose, monitor, and mitigate. Ask for concrete examples and how they’re handled.

Liquidity alignment. Redemption terms should match the strategy’s asset liquidity. Lockups, notice periods, gates, and side pockets are legitimate tools if disclosed and used fairly. Misalignment here is where operational stress becomes investor pain.

Side letters, MFN, and fairness

Large investors sometimes negotiate side letters: lower fees, extra reporting, or capacity rights. Well-run funds manage this with a most-favored-nation (MFN) process that lets similarly situated investors elect comparable terms. Ask whether side letters exist, what categories of terms they cover, and whether an MFN process applies to your share class and size.

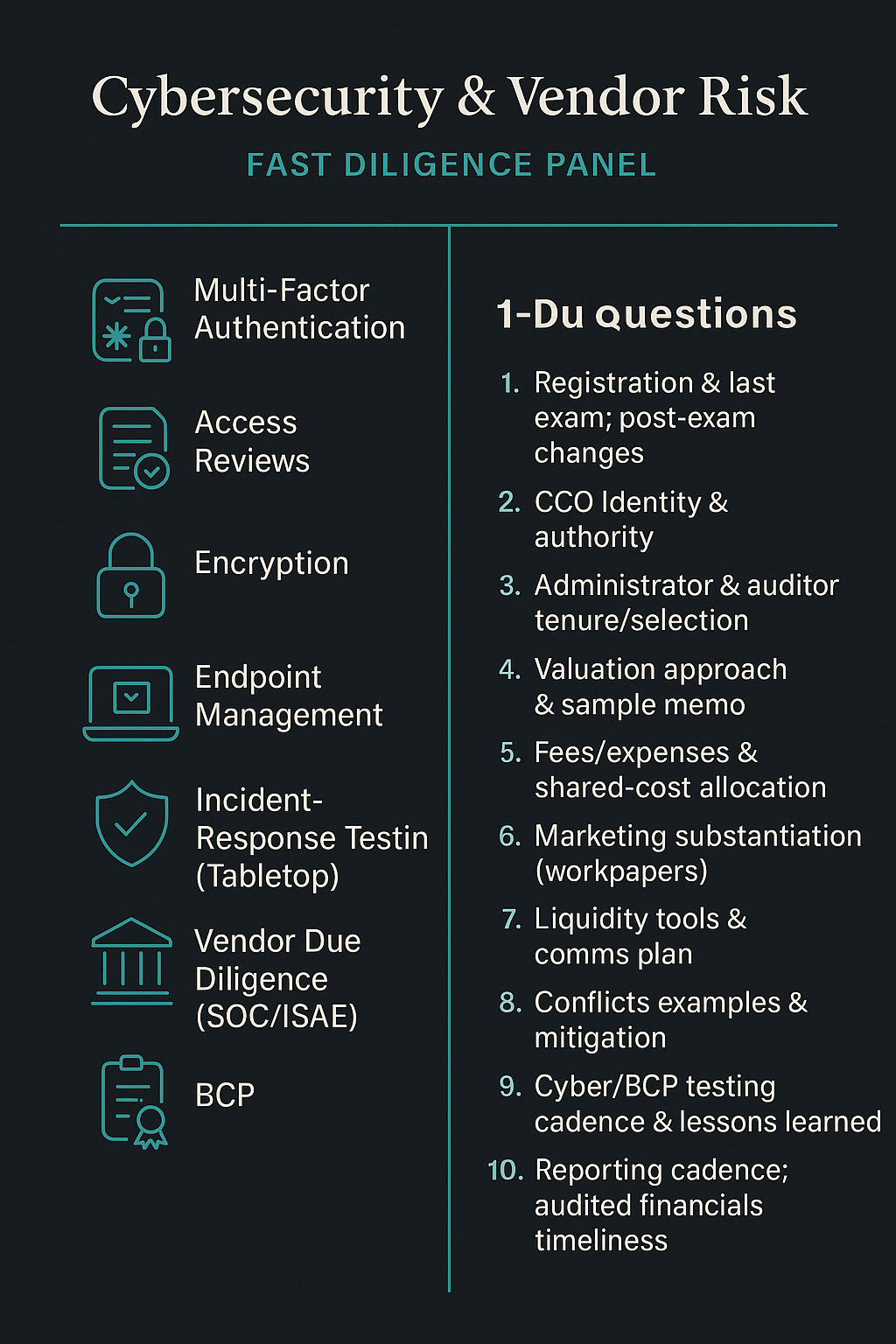

Cybersecurity and vendor risk

Hedge funds rely on administrators, prime brokers, cloud providers, and data vendors. Protection today includes multi-factor authentication, access reviews, encryption, incident-response testing, and due diligence on vendors (including their control reports). A quick way to test seriousness: ask when the last tabletop exercise happened and what changed afterward.

A fast due-diligence script (10 questions)

- Registration & oversight: Are you SEC-registered, state-registered, or an exempt reporting adviser? When was your last exam? What did you change afterward?

- CCO & resources: Who is your chief compliance officer? Do they have authority and direct access to leadership?

- Administrator & auditor: Who are they? How long have you worked with them? What drove the selection?

- Valuation: How are illiquid positions priced? Who sits on the valuation committee? Show me a sample memo.

- Fees/expenses: Beyond management and performance fees, what expenses hit the fund? How are shared costs allocated?

- Marketing substantiation: For any performance or statistic you present, can you show me the supporting workpapers?

- Liquidity alignment: Under what scenarios would you use gates, suspend redemptions, or create side pockets? How would you communicate that?

- Conflicts: Give examples of conflicts you face and how you mitigate them (cross-trades, affiliates, allocation of scarce deals).

- Cyber & business continuity: When was your last incident-response test? What did you learn and change?

- Investor reporting: What’s the cadence and content of letters? Do you deliver audited financials on time each year?

You’re listening for fluency, specificity, and documents that back up the talk.

Red flags that deserve a pause

- Fuzzy answers on valuation, fees, or conflicts.

- “Trust us” responses when you request performance backups or policy documents.

- Unengaged service providers (administrator/auditor turnover without a clear reason).

- Liquidity promises that seem generous for the strategy’s underlying assets.

- Weak governance (directors who rarely meet or never challenge the manager).

- Slow or defensive remediation after an exam.

Any one of these merits deeper digging; two or more should push you to reconsider.

How to be a better client (and protect yourself)

- Read Form ADV first, then the deck. It sets expectations and reveals conflicts.

- Right-size your allocation. Private funds are illiquid; size your ticket within a broader portfolio plan.

- Ask for a walkthrough. Have the manager take you through a sample valuation memo, expense allocation, and performance calculation.

- Document your understanding. Email follow-ups that restate key points create a shared record and flush out misunderstandings early.

- Start with a smaller ticket or a class with tighter liquidity terms while you build conviction.

Bottom line

Investor protection in hedge funds isn’t one silver bullet—it’s a stack of safeguards: fiduciary duty, truthful marketing, exams, independent administration, audited financials, custody controls, strong records, and clear rules for valuation, fees, conflicts, and liquidity. Transparency isn’t about daily NAVs; it’s about decision-useful information delivered consistently and backed by evidence. Ask targeted questions, insist on documentation, and watch how managers respond when pressed. The best ones treat transparency as part of their edge—and that’s exactly who you want managing your capital.

{kind=link}