This Content Is Only For Subscribers

One of the biggest advantages of a Roth IRA is the ability to grow your money tax-free and eventually withdraw it tax-free. But there’s a catch: you need to follow the five-year rule.

The rule isn’t complicated once you break it down, but it has caused a lot of confusion because there are actually two versions of the five-year rule—one for earnings and one for conversions. If you misunderstand it, you could face taxes or penalties you didn’t expect. Let’s unpack how it works and how you can make it work for you.

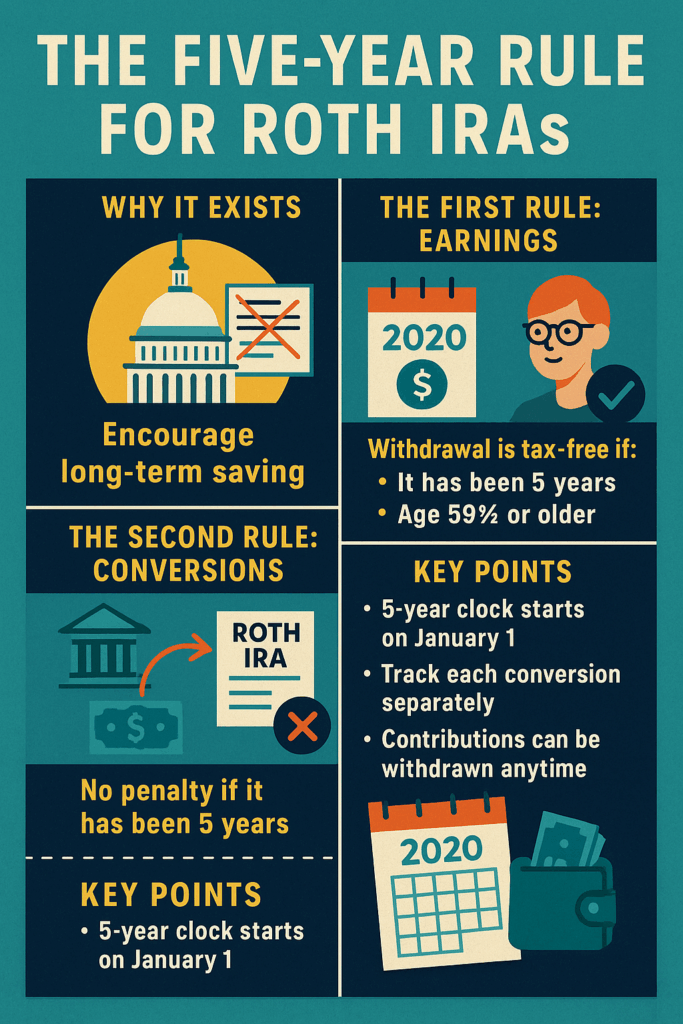

Why the Five-Year Rule Exists

When Congress created the Roth IRA in 1997, the idea was to encourage long-term retirement saving, not short-term tax shelters. To prevent people from simply putting money into a Roth, growing it quickly, and pulling it out tax-free, lawmakers added a waiting period before certain withdrawals are qualified.

The result: you must hold Roth contributions or conversions for at least five tax years before you can access the earnings without taxes or penalties.

The First Five-Year Rule: Earnings

The most commonly discussed five-year rule applies to investment earnings. To withdraw earnings tax-free, you must meet two conditions:

- Be age 59½ or older.

- Have had any Roth IRA open for at least five tax years.

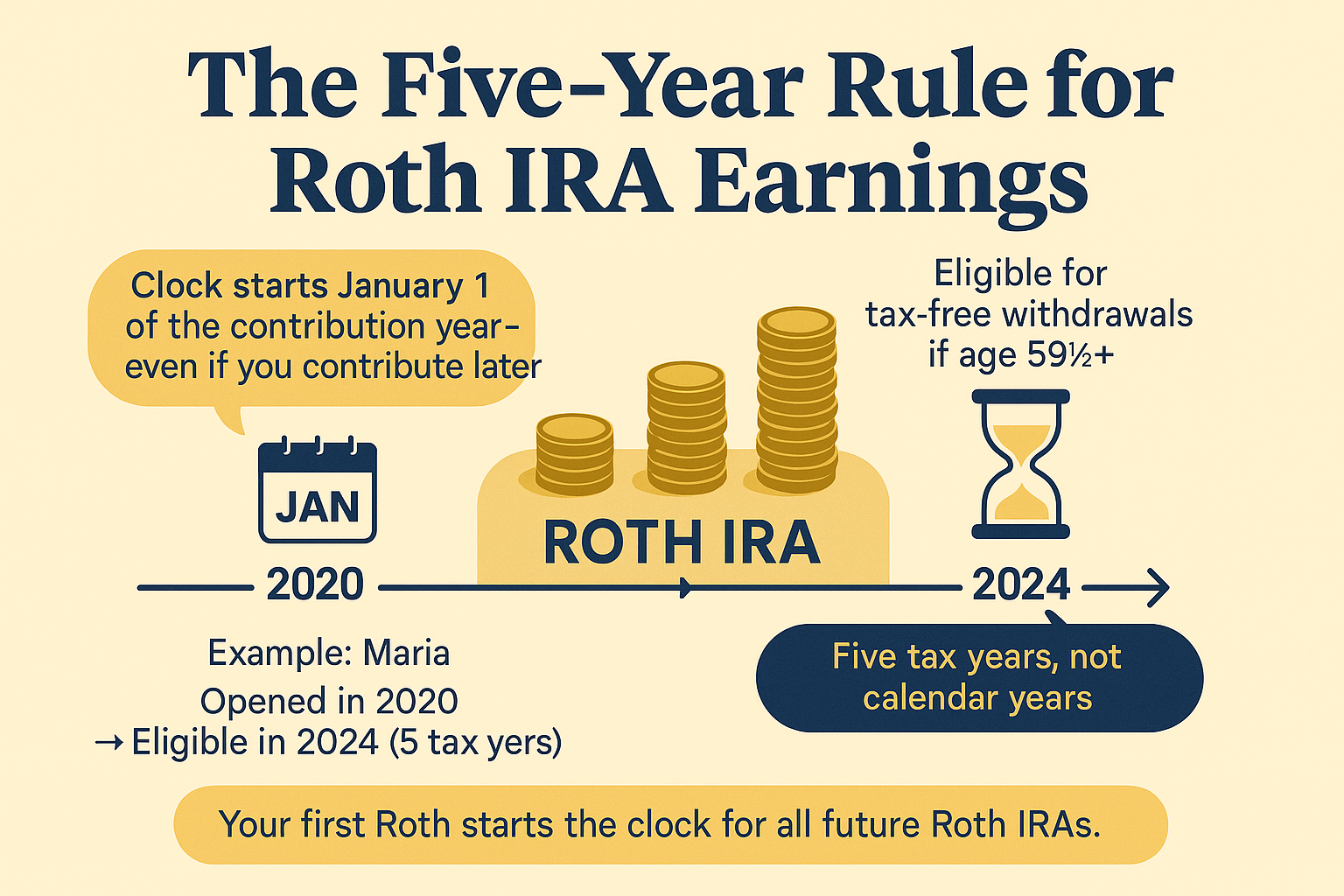

Example

- Maria opened her first Roth IRA in 2020 and contributed $5,000.

- In 2024, she turns 60.

- Because her Roth IRA has been open for five tax years (2020, 2021, 2022, 2023, 2024), she can now withdraw both her contributions and earnings tax-free.

Key point: The five-year clock starts on January 1 of the tax year of your first Roth contribution. So even if you contributed on December 31, 2020, your five-year clock started January 1, 2020.

The Second Five-Year Rule: Conversions

Conversions are different. Each conversion you make from a traditional IRA or 401(k) into a Roth IRA has its own five-year clock—but this one applies to the 10% early withdrawal penalty, not taxes.

- If you withdraw conversion dollars within five years and you’re under 59½, you may owe a 10% penalty.

- After five years (or once you’re 59½), converted amounts can be withdrawn penalty-free.

Example

- Jake converts $20,000 from a traditional IRA into a Roth in 2023 at age 45.

- If he withdraws that $20,000 before 2028 (and before age 59½), he’ll pay a 10% penalty.

- If he waits five tax years, or until he turns 59½, no penalty applies.

Contributions vs. Conversions vs. Earnings

It helps to remember the ordering rules the IRS applies when you take money out of a Roth IRA:

- Contributions (your deposits) come out first. Always tax- and penalty-free.

- Conversions come out next, oldest to newest. Subject to the five-year penalty clock if under 59½.

- Earnings come out last. Subject to both the five-year rule for earnings and the age 59½ rule.

This ordering protects you. Since contributions come out first, you can always tap those without worrying about penalties.

Practical Implications

- Start Early: Even a small Roth contribution today starts your five-year clock. That way, when you need the money in retirement, you’ve already cleared the hurdle.

- Track Conversions: If you’re using Roth conversions, keep good records of when each was made. Each has its own five-year penalty window.

- Don’t Panic Over Contributions: Because contributions are always accessible, many investors use Roths as a flexible backstop for emergencies.

- Early Retirees: Those planning to retire before 59½ often use a Roth conversion ladder, deliberately starting the five-year clocks on staggered conversions to create penalty-free withdrawals later.

Common Mistakes to Avoid

- Confusing the Rules: Remember, there are two five-year rules—one for earnings, one for conversions.

- Ignoring the Start Date: The clock starts January 1 of the contribution year, even if you contribute late in the year or before the April filing deadline.

- Pulling Earnings Too Early: Contributions are always safe to withdraw, but pulling out earnings before the five-year rule (and before age 59½) can trigger both taxes and penalties.

- Not Keeping Records: Custodians often track contributions and conversions, but it’s your responsibility to keep accurate records.

Special Exceptions

There are a few circumstances where the five-year rule doesn’t apply in the usual way:

- Inherited Roth IRAs: If you inherit a Roth, the original owner’s five-year clock applies. If they already satisfied it, you can take tax-free distributions right away (though distribution rules for beneficiaries apply).

- Disability or Death: The five-year rule doesn’t apply if you’re disabled or if distributions are made after death.

- First-Time Home Purchase: You can withdraw up to $10,000 of earnings for a first home purchase penalty-free, but the five-year rule still affects whether taxes apply.

Putting It All Together

The five-year rule is less intimidating once you see how it fits into the bigger picture:

- Contributions are always accessible.

- Conversions require careful tracking for the five-year penalty window.

- Earnings require both age 59½ and five years since your first Roth.

For most savers, the main lesson is simple: open a Roth IRA as early as possible, even with a small contribution, to start the clock. Then you’ll be ready when you need to tap your tax-free money in retirement.

Final Thoughts

The Roth IRA remains one of the most powerful tools for retirement planning, but the five-year rule is a critical detail. Understanding how it works can save you from costly mistakes and help you use your Roth with confidence.

Whether you’re making contributions, executing conversions, or planning for early retirement, keep the five-year rule in mind—it’s the key to unlocking the full tax-free benefits of your Roth IRA.

{kind=link}