This Content Is Only For Subscribers

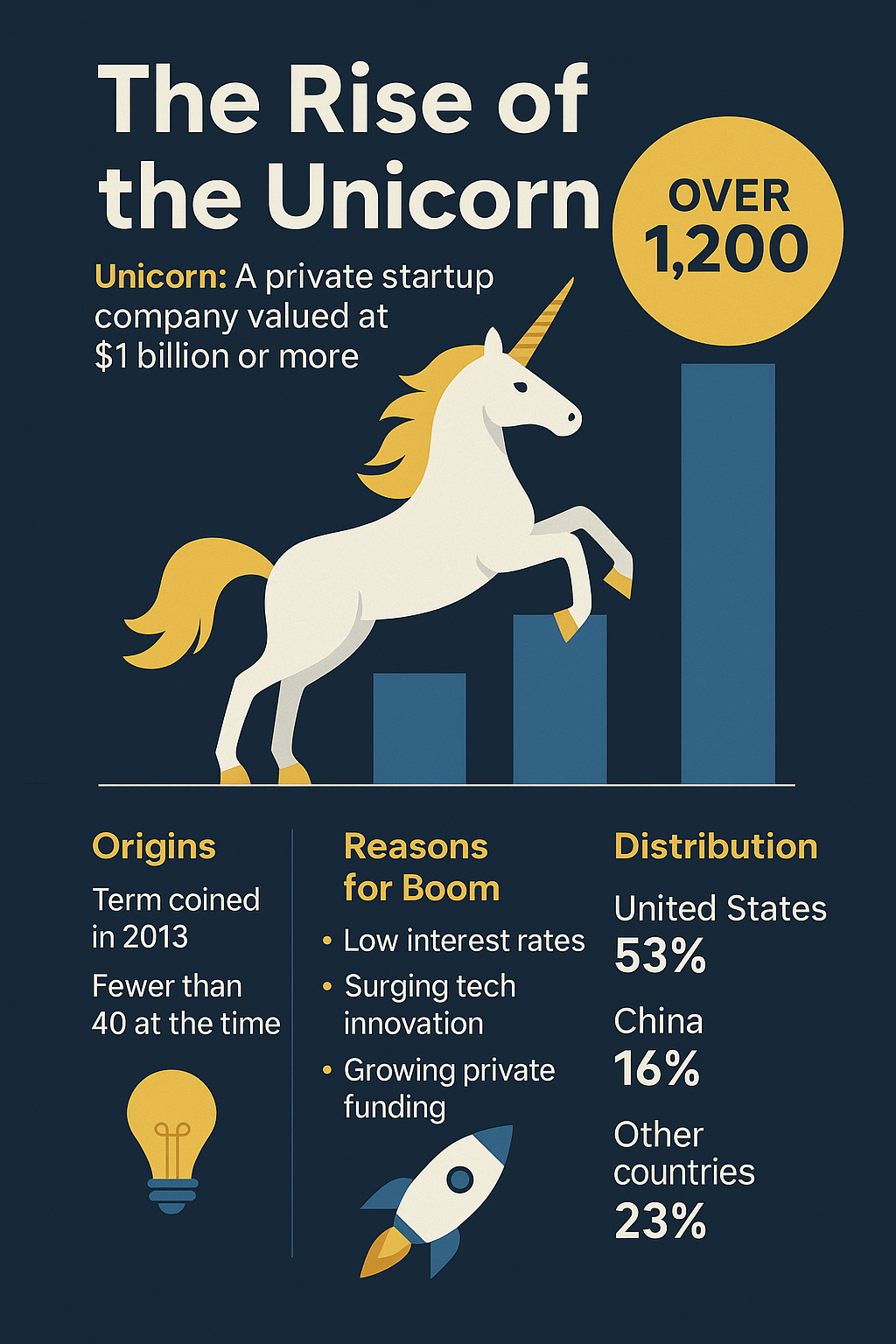

In 2013, venture capitalist Aileen Lee coined a new term: “unicorn.” She used it to describe startups valued at over $1 billion, comparing them to rare mythical creatures. At the time, there were fewer than 40 unicorns in the world. A decade later, there are hundreds.

Unicorns have become the symbol of venture capital’s outsized potential. They are the rare companies that can deliver such extraordinary returns that they define an entire fund’s success. But they also raise questions: Are unicorn valuations always real? Do they distort investor expectations? And what happens when they stumble?

Why Unicorns Matter

Most startups fail, and most venture funds rely on just a handful of big winners to generate returns. Unicorns are those winners.

- Return drivers: A single unicorn can make an entire fund. For example, Sequoia’s early investment in WhatsApp turned $60M into $3B when Facebook acquired it.

- Fund math: If a VC fund invests in 30 startups, and 20 fail, 7 muddle along, and 3 become unicorns, those 3 likely drive 90% of the profits.

- Reputation builders: Unicorns make firms famous. Kleiner Perkins became a household name after backing Google and Amazon; Benchmark cemented its reputation with Uber.

Types of Unicorns

Not all unicorns are alike.

Consumer Disruptors

- Examples: Uber, Airbnb, DoorDash

- They target everyday users and scale quickly with network effects.

Enterprise Builders

- Examples: Stripe, Databricks, Snowflake

- Less visible to consumers, but crucial in powering business infrastructure.

Regional Champions

- Examples: Flipkart (India), Grab (Southeast Asia), Klarna (Europe)

- Dominate in specific geographies with local expertise.

Frontier Innovators

- Examples: SpaceX, Moderna

- Push the boundaries of science and technology, often capital-intensive.

The Benefits of Unicorns in Portfolios

- Massive Upside: A unicorn exit can return 10x–100x the original investment.

- Brand Value: Being associated with a unicorn enhances a VC firm’s reputation, helping it raise future funds.

- Ecosystem Effects: Unicorns often spin off new startups, creating fertile ground for future investments.

Risks and Criticisms

Unicorns aren’t always the fairy tales they appear to be.

- Overvaluation: Some unicorns are “paper unicorns,” valued at $1B+ on private rounds but never exiting at that level. WeWork peaked at $47B before collapsing.

- Down rounds: If growth stalls, later investors may demand lower valuations, hurting morale and founder equity.

- Profitability gaps: Many unicorns focus on growth, not profits. When public markets demand sustainable business models, valuations can tumble.

- Concentration risk: Over-reliance on unicorns means a fund’s performance is tied to a few unpredictable outcomes.

Case Studies

Sequoia invested $60M in WhatsApp. When Facebook acquired it for $19B in 2014, Sequoia’s gain exceeded $3B. One investment paid for multiple funds.

WeWork

Backed heavily by SoftBank, WeWork reached a $47B valuation before its failed IPO in 2019. By 2023, it filed for bankruptcy. For some backers, it was a painful reminder that valuation ≠ value.

Stripe

Founded in 2010, Stripe grew into one of the most valuable private companies globally. Its payments infrastructure underpins millions of businesses. While it has yet to go public, Stripe illustrates how a unicorn can anchor expectations for years.

The Unicorn Effect on the Industry

The chase for unicorns has reshaped venture capital:

- Bigger funds: VC firms raise multi-billion-dollar funds to support unicorn-scale bets.

- Mega-rounds: $100M+ rounds, once rare, are now common.

- SoftBank and the Vision Fund: With $100B in capital, SoftBank accelerated the unicorn boom, sometimes pushing valuations beyond fundamentals.

But this also created fragility. In downturns, paper valuations collapse, and many unicorns struggle to justify their hype.

Lessons for Novice Investors

Even if you’ll never invest in a unicorn directly, the phenomenon offers insights:

- A few winners drive most returns. Whether in startups or stocks, a small group often accounts for the majority of gains.

- Beware of hype. Unicorn valuations can collapse if built on shaky foundations.

- Diversification matters. Don’t pin your hopes on a single “next big thing.”

- Timing is critical. Getting in early makes unicorns profitable for VCs; late-stage investors often overpay.

- Value vs. valuation. A billion-dollar sticker price doesn’t guarantee lasting worth.

Final Thoughts

Unicorns are both the promise and the peril of venture capital. They represent the dream of extraordinary success—proof that bold bets can pay off spectacularly. But they also remind us of the dangers of inflated expectations.

For novice investors, unicorns illustrate a timeless truth: big winners can define portfolios, but chasing hype without discipline is dangerous. In VC and in personal investing, the goal isn’t just to find unicorns—it’s to build a strategy resilient enough to survive whether they appear or not.

{kind=link}