This Content Is Only For Subscribers

When people think of venture capital, they often imagine billion-dollar exits, overnight fortunes, and stories of investors who turned a small bet into generational wealth. But the truth about venture capital returns is more complicated. They are shaped by cycles of booms and busts, a handful of extraordinary wins, and long stretches of underperformance.

To understand the risk-return profile of VC today, it helps to look at its history. Over the decades, venture capital has delivered spectacular results for a small group of investors while also disappointing many others.

Early Days: From DEC to Apple

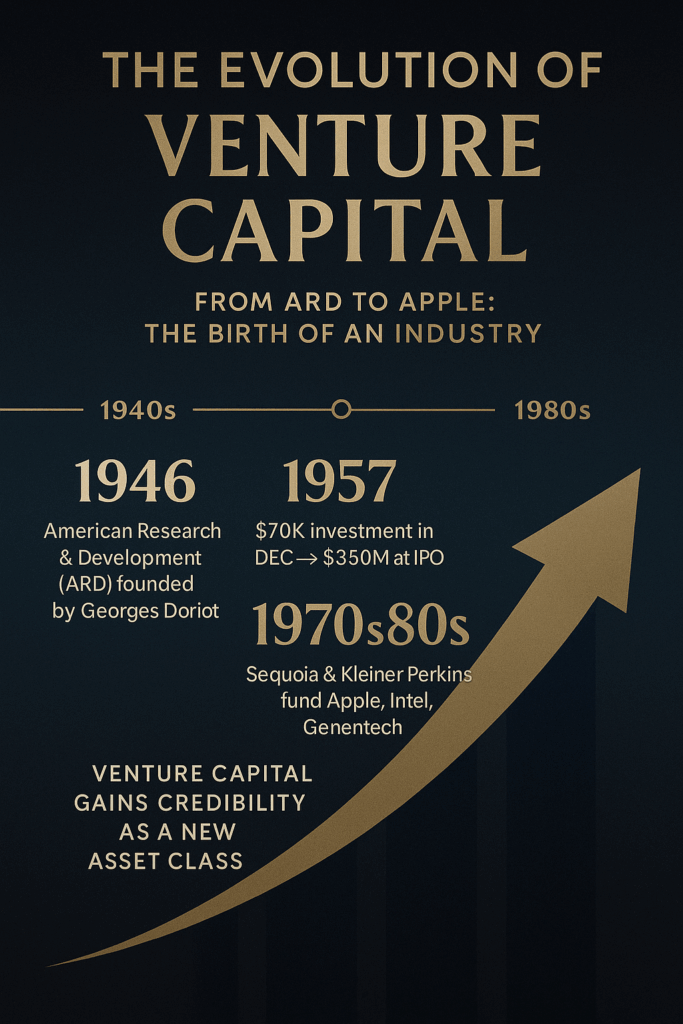

The venture capital story began in the mid-20th century. In 1946, Georges Doriot launched American Research and Development Corporation (ARD), one of the first VC firms. ARD’s famous success was Digital Equipment Corporation (DEC). A $70,000 investment in 1957 turned into more than $350 million at IPO in 1968. This single win proved that backing young companies could create fortunes.

In the 1970s and 80s, early venture firms like Sequoia Capital and Kleiner Perkins funded Apple, Intel, and Genentech. Returns from these deals were massive—Apple’s IPO in 1980 alone minted dozens of millionaires. These stories cemented venture capital as a credible investment strategy.

The Dot-Com Era: Boom and Bust

The 1990s internet boom marked the first time VC entered mainstream headlines.

- Wins: Firms that backed Amazon, eBay, and Google saw returns in the hundreds of times their initial investment. Google’s 2004 IPO remains one of the greatest VC home runs of all time.

- Losses: But the dot-com crash of 2000–2001 wiped out billions. Startups like Pets.com and Webvan raised huge sums, only to collapse when business models failed.

For investors, this era showed both extremes: life-changing gains for those who picked winners, and painful losses for those caught in hype. The net result was uneven—top-tier VC funds outperformed public markets, but the median fund barely broke even.

The Social Media and Mobile Wave

The mid-2000s to early 2010s brought the rise of social media, smartphones, and cloud computing.

- Facebook: Accel Partners invested $12.7 million in 2005. By the time of Facebook’s IPO in 2012, that stake was worth billions—a return of more than 100x.

- Airbnb & Uber: Early investors in these platforms reaped 1,000x-type returns. Benchmark’s $12 million bet on Uber turned into billions.

- Google’s YouTube acquisition (2006): Sequoia Capital invested $11.5 million in YouTube, later selling to Google for $1.65 billion—an exit that returned its fund multiple times over.

During this wave, venture returns soared for firms with access to the best deals. But again, performance was skewed—a few funds captured extraordinary outcomes, while many lagged.

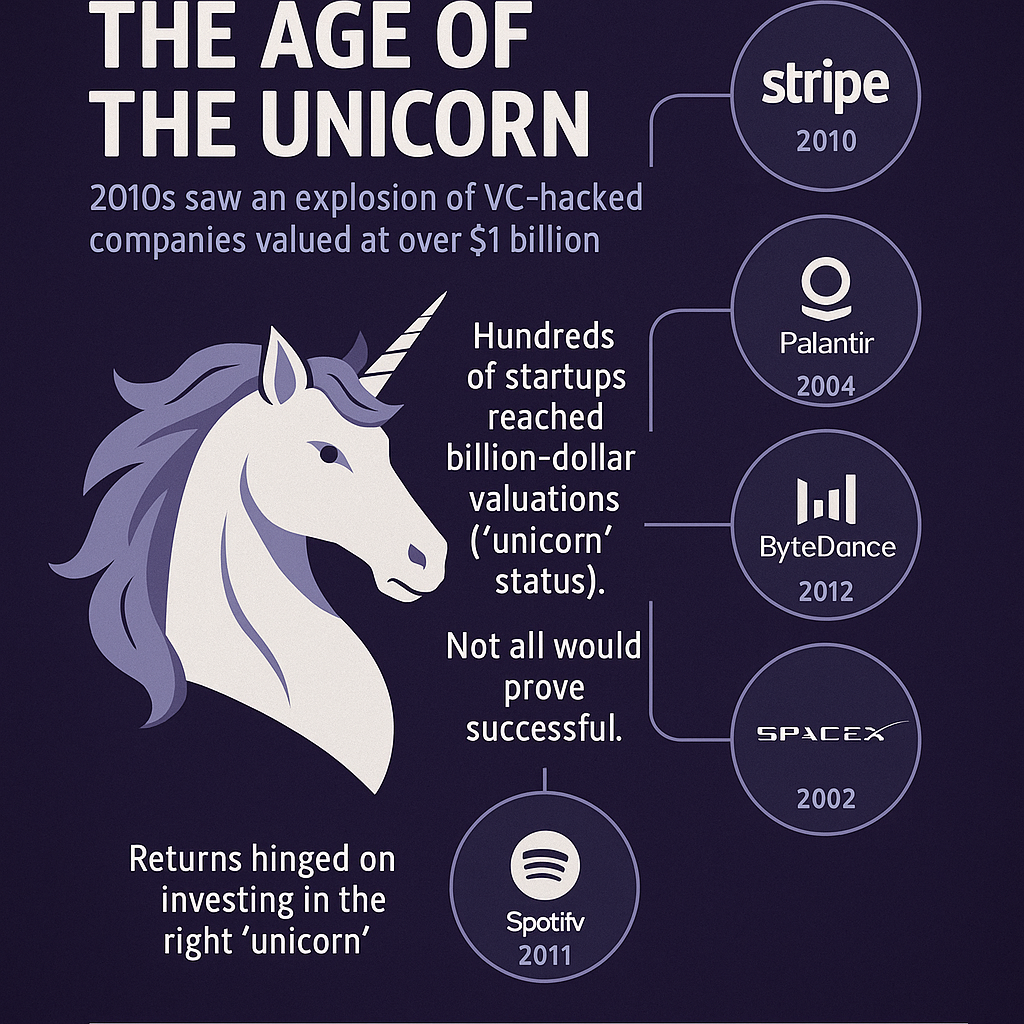

The 2010s: The Age of the Unicorn

By the 2010s, “unicorns”—startups valued at over $1 billion—became the defining feature of VC portfolios.

- Stripe, Palantir, ByteDance, and SpaceX reached valuations in the tens of billions.

- Zoom’s IPO in 2019 delivered one of Sequoia’s best returns ever.

- Spotify (2018 IPO) validated European VC, with investors like Creandum profiting massively.

But not all unicorns became successes. WeWork was valued at $47 billion before collapsing ahead of its IPO. Other unicorns, like Juicero and Theranos, became cautionary tales.

Returns in this era highlighted the importance of selectivity. Funds with stakes in the right unicorns made fortunes; others with exposure to “paper unicorns” that never exited realized far less.

Cycles and Corrections

One constant in VC history is its cyclicality.

- 2000–2001: Dot-com crash erased billions.

- 2008–2009: Global financial crisis tightened capital, hurting exits.

- 2020–2021: Ultra-low interest rates fueled record fundraising and sky-high valuations.

- 2022–2023: Rising rates triggered a correction, IPO windows slammed shut, and valuations fell sharply.

Returns depend not only on company success but also on macro conditions. Even the best startups may wait years for a favorable IPO market.

The Dispersion of Returns

Perhaps the most striking feature of venture capital is the spread between winners and losers.

- Top quartile funds (the best 25%) historically deliver 20–30% annualized returns over a decade.

- Median funds often underperform the S&P 500.

- Bottom quartile funds can lose money outright.

This means that venture capital, as an asset class, looks attractive only if you can access the top firms. Yale University’s endowment famously outperformed peers by allocating heavily to VC—but most institutions without access struggled.

Why the Past Matters

Looking at history, several themes emerge:

- Concentration of returns. A handful of deals—Google, Facebook, Uber, Airbnb—generated a disproportionate share of VC’s wealth creation.

- Boom-and-bust cycles. Every wave of optimism has been followed by painful corrections.

- Fund selection is everything. The difference between top-quartile and average funds is dramatic.

- Innovation drives returns. The best VC wins come from backing technologies that reshape the economy, from semiconductors to social media to AI.

Lessons for Novice Investors

You may not be writing $10 million checks into startups, but the history of VC returns carries important lessons:

- Diversification matters. Just as VCs invest in 20–40 startups knowing most will fail, individuals should diversify across stocks, funds, or asset classes.

- Don’t be fooled by hype. Every cycle has its Pets.coms and Theranoses. Focus on fundamentals.

- Time horizons are long. The biggest VC wins often take a decade. Similarly, personal investing works best when you think in decades, not days.

- Manager selection matters. In VC, the difference between the top 25% and everyone else is huge. For individuals, this translates to choosing high-quality funds or managers carefully.

Final Thoughts

The history of venture capital returns is a story of extremes—spectacular wins, dramatic failures, and cycles of boom and bust. For investors, it is a reminder that risk and reward are inseparable. The biggest fortunes often require patience, courage, and tolerance for failure along the way.

For novices, the lesson is less about chasing unicorns and more about embracing the principles that make venture capital work: diversification, discipline, and long-term vision.

{kind=link}