This Content Is Only For Subscribers

When hedge funds make headlines, it’s often because of spectacular success—record profits, bold bets, and legendary investors. But some of the most important lessons come from the other side of the story: when things fall apart.

The collapse of Archegos Capital Management in 2021 was one of the most dramatic financial implosions in recent memory. Though technically a family office rather than a hedge fund, Archegos’s downfall echoed earlier hedge fund disasters like Long-Term Capital Management in the 1990s. Both showed how leverage, secrecy, and overconfidence can turn billions into rubble almost overnight.

For everyday investors, these cautionary tales are worth studying. They show how quickly risk can compound, and how even sophisticated players aren’t immune to the same traps that trip up individuals.

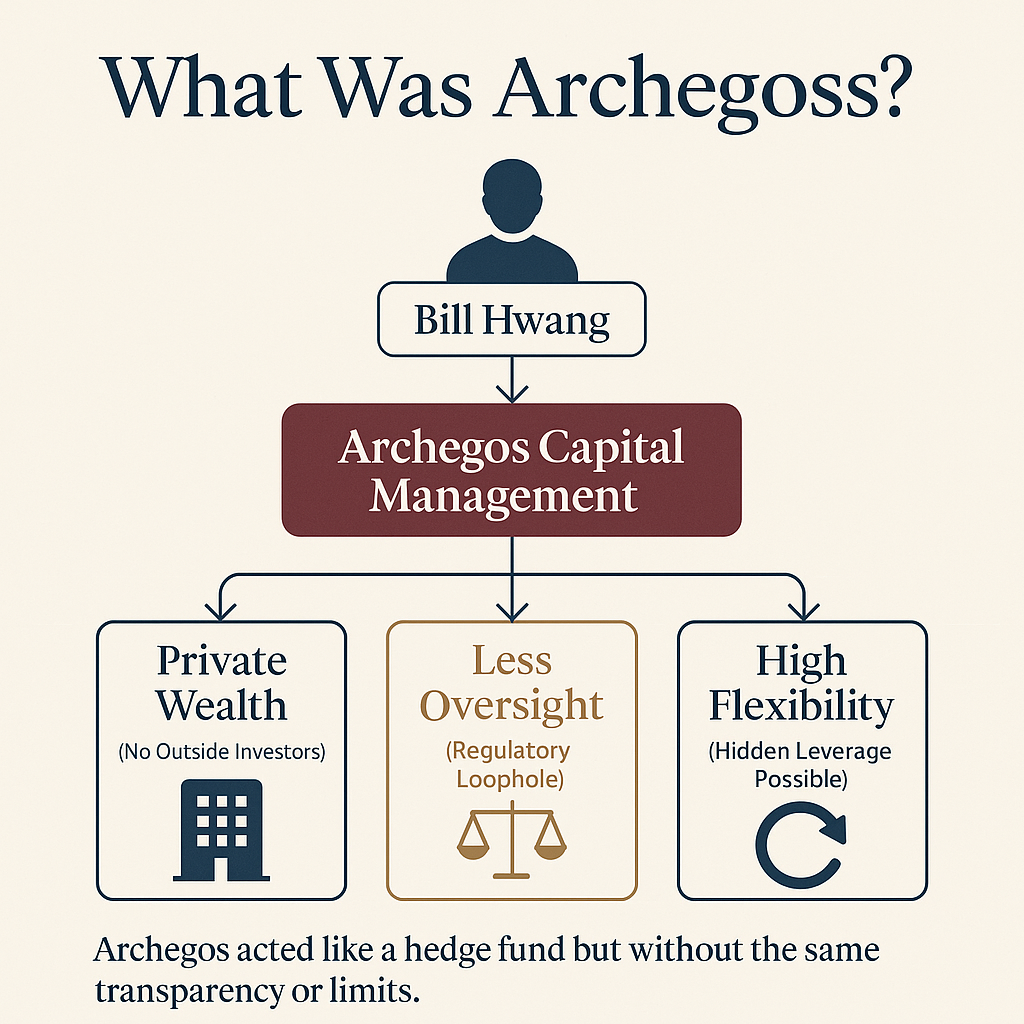

What Was Archegos?

Archegos Capital Management was founded by Bill Hwang, a former hedge fund manager who had previously run Tiger Asia, one of the so-called “Tiger Cubs” trained under Julian Robertson. After regulatory issues led Tiger Asia to shut down, Hwang pivoted to managing his own fortune through Archegos, a family office.

Because family offices manage private wealth rather than outside investors’ money, they face less regulatory oversight than hedge funds. That gave Archegos more flexibility—but also meant its risks were less visible to outsiders.

How the Blow-Up Happened

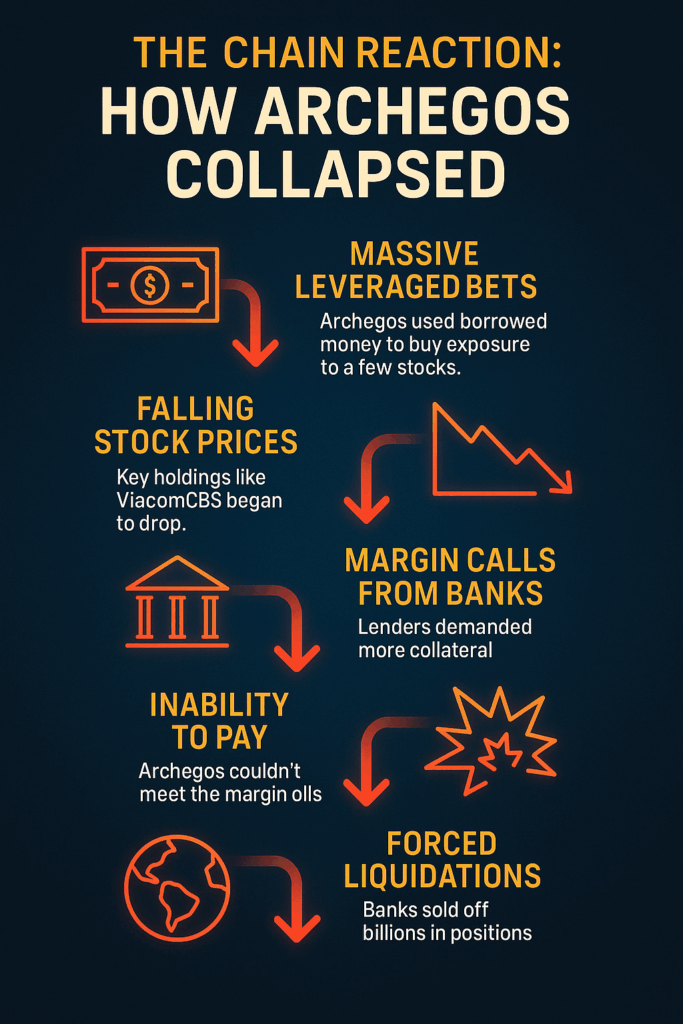

Archegos quietly built massive, concentrated positions in a handful of stocks, including ViacomCBS and several Chinese tech companies. But it didn’t simply buy shares outright. Instead, it used complex derivatives called total return swaps, which allowed it to gain exposure to stocks without publicly disclosing its stakes.

This meant Archegos could build enormous positions without the market realizing how much risk it was taking. The fund’s leverage—essentially, borrowed money—amplified these bets even further.

When some of Archegos’s stocks fell in early 2021, the firm’s lenders (big banks like Credit Suisse and Nomura) issued margin calls—demands for more collateral. Archegos couldn’t pay. Within days, banks raced to liquidate its positions, sending billions of dollars in stock flooding into the market. The result was a rapid, catastrophic collapse that left some banks with losses exceeding $5 billion each.

Lessons from Archegos

Archegos’s downfall offers several clear takeaways for investors:

- Hidden leverage is dangerous.

Borrowing to invest can magnify gains—but it magnifies losses just as quickly. Archegos was undone by the sheer size of its borrowed bets. - Concentration equals fragility.

Putting too much money into a few positions, no matter how confident you are, leaves little room for error. A diversified portfolio is far more resilient. - Transparency matters.

Archegos’s use of swaps kept its true exposures hidden until it was too late. For individuals, this translates into a simple rule: never invest in something you don’t understand.

A Familiar Pattern: LTCM in 1998

Archegos wasn’t the first high-profile hedge fund collapse. In 1998, Long-Term Capital Management (LTCM) nearly brought down the global financial system.

LTCM was run by some of the brightest minds in finance, including two Nobel Prize-winning economists. Using complex mathematical models, they placed huge, leveraged bets on bond markets. At first, the strategy produced stellar returns.

But when the Russian government defaulted on its debt in 1998, markets behaved in ways LTCM’s models hadn’t anticipated. The fund lost billions, and its enormous borrowings threatened to destabilize the financial system. The Federal Reserve intervened to organize a rescue by major banks.

The parallels with Archegos are striking: both relied heavily on leverage, both made concentrated bets, and both collapsed when markets moved against them.

Why Blow-Ups Keep Happening

You might wonder: if the risks are so obvious, why do these disasters keep repeating? The answer lies in human nature.

- Greed tempts managers to push for higher returns.

- Overconfidence convinces them they’ve found a “can’t miss” strategy.

- Short-term success breeds complacency.

As long as money managers are human, the cycle of bold bets, big wins, and sudden collapses is likely to continue.

What Novice Investors Can Learn

For someone just starting their investing journey, stories like Archegos and LTCM might seem distant. But the principles apply directly:

- Avoid over-leverage. Don’t borrow heavily to invest, especially early on. The risks often outweigh the rewards.

- Diversify your portfolio. Spread investments across sectors, asset classes, and geographies. Don’t let one idea dominate.

- Respect risk. Even smart investors get it wrong. Build guardrails that protect you from worst-case scenarios.

- Don’t chase complexity. If you don’t fully understand a product or strategy, steer clear. Simplicity is safer.

The Ripple Effects

Hedge fund blow-ups don’t just hurt the managers involved. They can ripple through financial markets, hurting banks, pension funds, and ordinary investors. Credit Suisse’s $5.5 billion loss from Archegos, for example, led to major leadership changes and damaged the bank’s reputation.

These events remind us that risk isn’t contained—it spreads. That’s why regulators, banks, and investors alike pay close attention when a fund grows too big or too opaque.

Final Thoughts

The story of Archegos is not just about one man or one fund. It’s part of a recurring theme in financial history: the danger of unchecked risk.

For everyday investors, the best response isn’t to avoid investing altogether. It’s to build a strategy that acknowledges uncertainty, manages risk, and avoids the pitfalls of overconfidence.

Remember: success in investing isn’t about swinging for the fences. It’s about staying in the game. Archegos and LTCM show what happens when that lesson is ignored.

{kind=link}