This Content Is Only For Subscribers

The past decade has seen the rise of Bitcoin, Ethereum, and thousands of other digital assets. But while private innovators built cryptocurrencies and stablecoins, governments have been watching closely. Now, many central banks are exploring their own answer: Central Bank Digital Currencies (CBDCs).

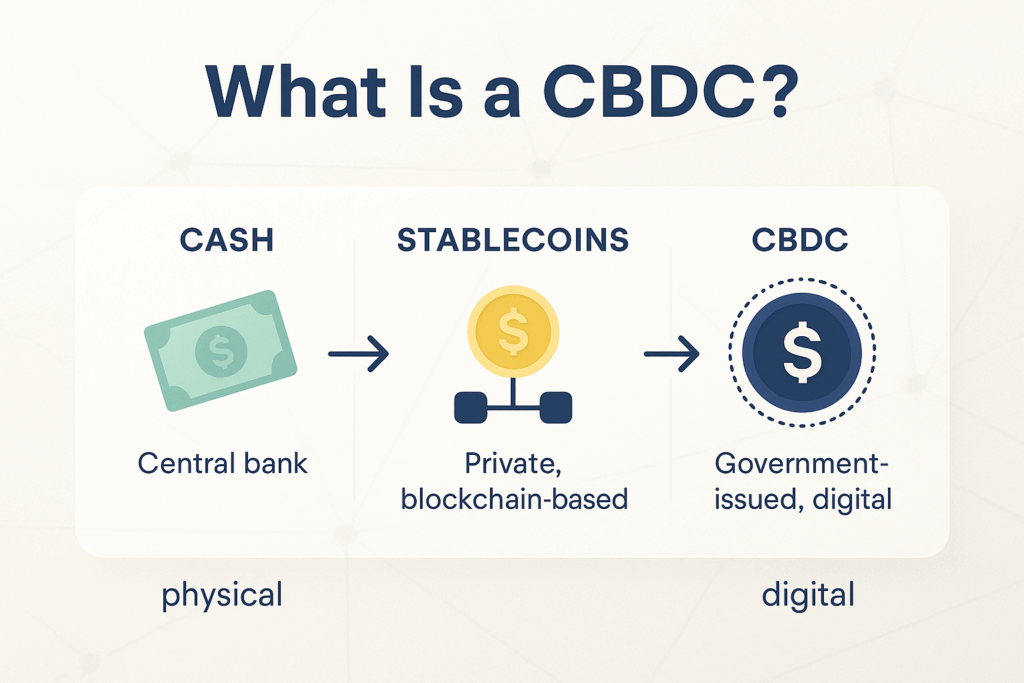

A CBDC is essentially a digital version of a country’s official currency, issued and backed by the central bank. If Bitcoin is “digital gold” and USDC is a private digital dollar, then a CBDC is the state’s direct entry into the digital money arena.

But what would CBDCs mean for traditional banking, for DeFi, and for everyday users?

What Is a CBDC?

A CBDC is a digital form of fiat currency. Unlike Bitcoin, it isn’t decentralized or mined by computers. Instead, it’s issued and managed by a nation’s central bank.

- Retail CBDC: Designed for the general public, functioning like cash in digital form.

- Wholesale CBDC: Used by financial institutions for interbank payments and settlement.

Think of a retail CBDC as “digital cash” you could hold in a wallet app on your phone, issued directly by your central bank.

Why Are Governments Interested?

Modernizing Payments

- CBDCs could make domestic and cross-border transactions faster and cheaper.

Financial Inclusion

- A CBDC wallet might give unbanked people access to digital payments without needing a traditional bank account.

Maintaining Monetary Control

- Stablecoins like USDT and USDC already act like digital dollars. CBDCs give governments their own alternative, ensuring monetary policy remains effective.

Combating Illicit Activity

- With programmable features, CBDCs could include stronger oversight of transactions.

Responding to Private Innovation

- The popularity of stablecoins and China’s rapid rollout of its digital yuan (e-CNY) have spurred other central banks to act.

Global Experiments

- China (e-CNY): The most advanced major CBDC project, with millions of users testing digital yuan payments across retail stores and apps.

- Bahamas (Sand Dollar): Launched in 2020, the Sand Dollar was one of the first fully deployed CBDCs.

- Sweden (e-krona): Pilots ongoing, exploring how to modernize payments in an increasingly cashless society.

- European Central Bank (Digital Euro): Research and testing underway, with potential issuance later this decade.

- United States (Digital Dollar): The Federal Reserve is studying CBDCs but has taken a slower, more cautious approach.

How CBDCs Differ from Stablecoins

| Feature | CBDC | Stablecoin (USDC, USDT, DAI) |

| Issuer | Central bank | Private company or decentralized protocol |

| Backing | Sovereign guarantee | Fiat reserves, crypto collateral, or algorithms |

| Trust Source | Government authority | Company transparency or protocol design |

| Regulation | Fully regulated | Partially regulated, evolving |

| Potential Features | Programmability, direct stimulus | Incentives, DeFi integration |

In short: stablecoins are market-driven substitutes for dollars and euros, while CBDCs are government-issued replacements for cash and bank deposits.

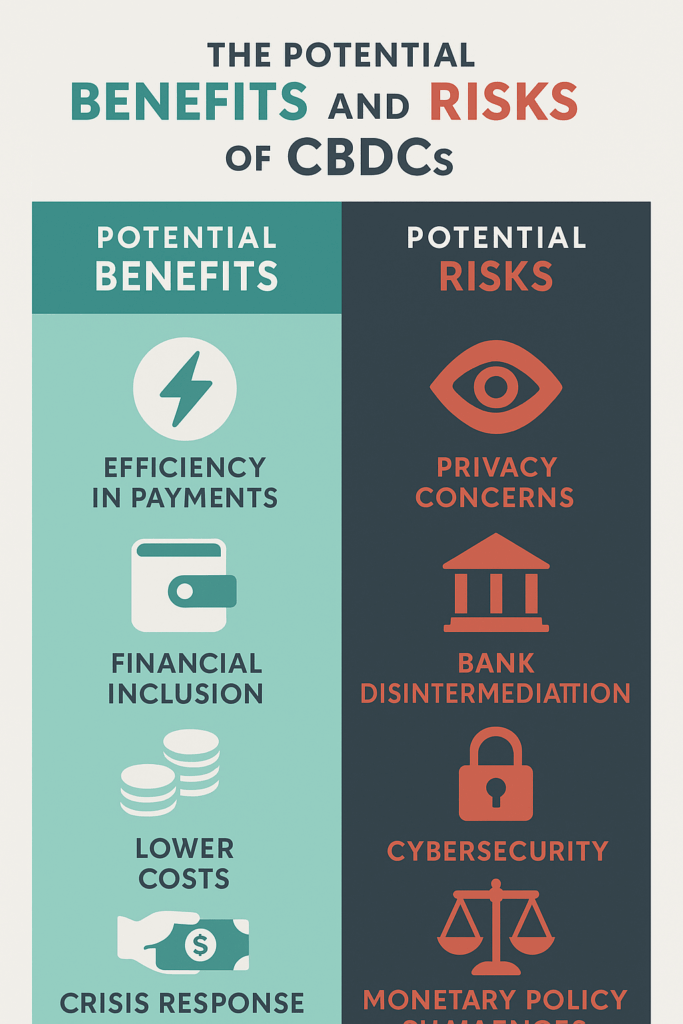

Potential Benefits

- Efficiency in Payments– Faster settlement of domestic and cross-border transactions.

- Financial Inclusion– Digital wallets could reach people without access to traditional banking.

- Lower Costs– Potentially cheaper than credit card networks or remittance providers.

- Crisis Response– Central banks could deliver stimulus payments instantly to citizens’ wallets.

Potential Risks

- Privacy Concerns– CBDCs could enable governments to monitor individual transactions closely.

- Bank Disintermediation– If people hold CBDCs directly with the central bank, they may withdraw funds from commercial banks, weakening bank balance sheets.

- Cybersecurity– A CBDC system would be a critical national target for hackers.

- Monetary Policy Challenges– The ease of moving funds could amplify volatility in banking systems during crises.

CBDCs and DeFi

For DeFi, CBDCs could be both a threat and an opportunity.

- Threat: If CBDCs gain dominance, governments might restrict the use of decentralized stablecoins.

- Opportunity: CBDCs could plug directly into DeFi protocols, creating safer, more stable liquidity pools.

Imagine borrowing against tokenized assets using a CBDC as collateral—it would bring state-backed money directly into the decentralized ecosystem.

Lessons for Novice Investors

Even if you never interact with a CBDC directly, they offer lessons about the future of money:

- Digital assets are here to stay. Even governments are adapting.

- Innovation sparks response. Stablecoins pressured central banks into action.

- Trust matters. While stablecoins rely on transparency, CBDCs rely on sovereign backing.

- Expect trade-offs. CBDCs may boost efficiency but reduce privacy.

- Watch policy. The rollout of CBDCs could reshape both crypto and traditional finance.

Final Thoughts

CBDCs are still experimental, but they represent a major shift in the way money could work. Just as DeFi aims to replace banks with smart contracts, CBDCs aim to update government money for the digital age.

Whether CBDCs become widely adopted, coexist with stablecoins, or face resistance from privacy advocates, they mark a new chapter in the story of digital assets. For novice investors, the key is awareness: the future of money is being written now—and it won’t look exactly like the past.

{kind=link}