This Content Is Only For Subscribers

Investing in real estate isn’t just about choosing properties—it’s also about deciding whether to invest through debt or equity structures. Understanding the difference between debt and equity real estate funds is essential for investors looking to balance risk, return, and portfolio diversification.

In this article, we’ll break down how debt and equity real estate funds work, the risks and rewards of each, and how to integrate them into a broader real estate strategy.

What Are Debt Real Estate Funds?

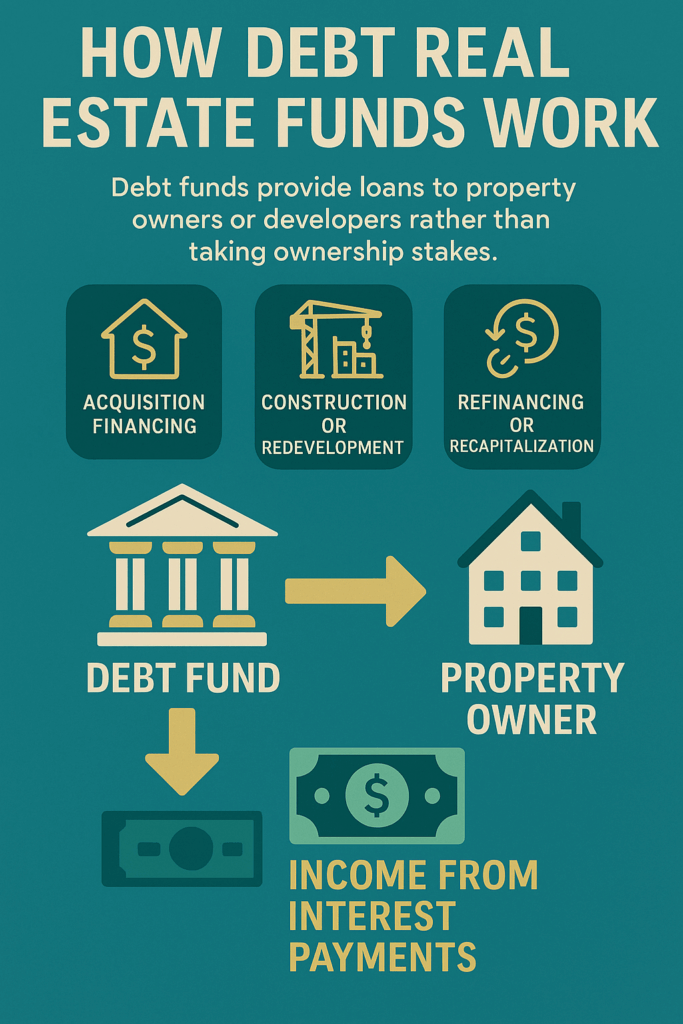

Debt real estate funds, sometimes called real estate credit funds, provide loans to property owners or developers rather than taking ownership stakes. These loans can be for:

- Acquisition financing

- Construction or redevelopment

- Refinancing or recapitalization

Investors in debt funds effectively act as lenders, earning income primarily through interest payments on the loans.

Key Characteristics of Debt Funds

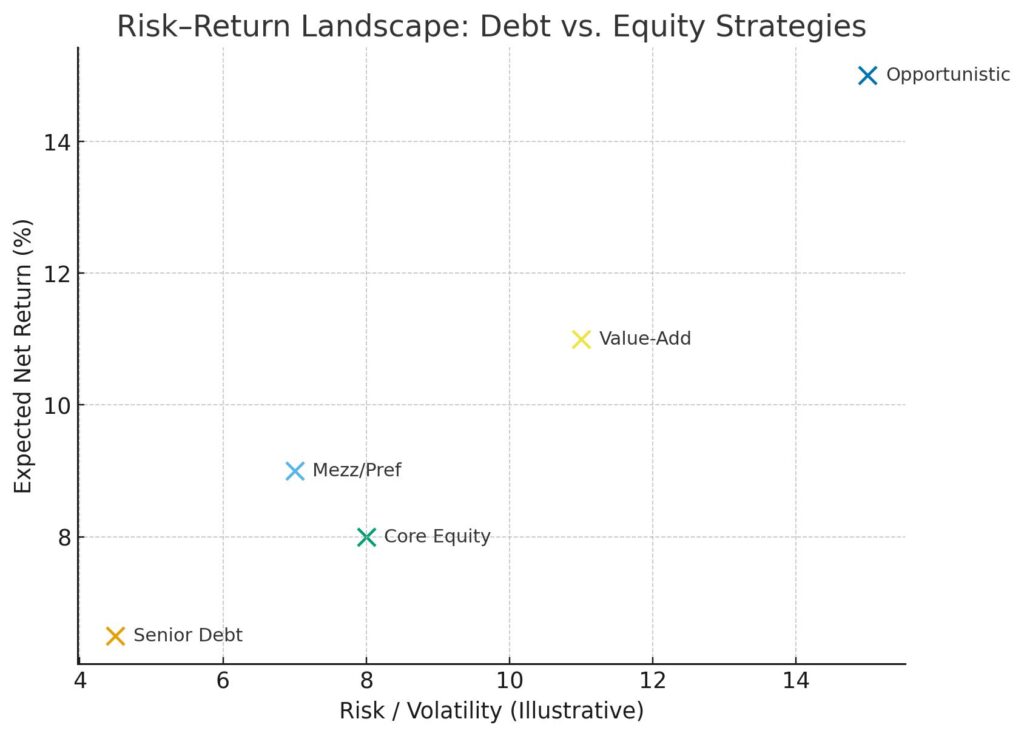

- Lower Risk: Investors have a higher claim on assets in case of default, making debt funds generally safer than equity funds.

- Predictable Income: Returns come from regular interest payments, providing a steady cash flow.

- Limited Upside: Since returns are capped at interest rates, investors typically do not benefit from property appreciation.

- Shorter Duration: Debt funds often have defined loan terms, which may range from 1 to 5 years.

Example: A debt fund might provide a $20 million loan to a developer to renovate an office building. The fund receives interest payments monthly or quarterly, and the principal is returned at the end of the loan term.

What Are Equity Real Estate Funds?

Equity real estate funds acquire ownership stakes in properties, sharing in both rental income and potential appreciation. Equity investors assume more risk than debt investors but have greater potential for higher returns.

Key Characteristics of Equity Funds

- Higher Risk: Investors are last in line if the property underperforms or defaults.

- Variable Returns: Income depends on rental performance and capital gains from property appreciation.

- Longer Investment Horizon: Equity investments often require multi-year commitments to realize full value.

- Active Management: Fund managers actively oversee property operations, tenant relationships, and capital improvements.

Example: An equity fund purchases a multifamily apartment complex. Investors earn income through rent distributions and benefit from any increase in the property’s market value when it is eventually sold.

Comparing Debt and Equity Real Estate Funds

| Feature | Debt Funds | Equity Funds |

| Risk | Lower | Higher |

| Returns | Fixed interest | Variable (rental + appreciation) |

| Upside Potential | Limited | High |

| Claim on Assets | Senior (paid first in default) | Subordinate (paid after debt holders) |

| Investment Horizon | Short to medium | Medium to long |

| Management Involvement | Passive | Active |

Advantages and Drawbacks

Debt Funds

Advantages:

- Stability: Predictable interest payments provide steady income.

- Lower Volatility: Less exposed to market swings than equity.

- Priority Claim: Debt holders are first to be repaid if the property defaults.

Drawbacks:

- Capped Returns: Investors cannot benefit from significant property appreciation.

- Inflation Risk: Fixed-rate interest may lose value in rising inflation environments.

Equity Funds

Advantages:

- High Return Potential: Benefit from rental income and property appreciation.

- Portfolio Diversification: Adds growth-oriented assets to a balanced portfolio.

- Active Influence: Investors can leverage manager expertise to enhance property performance.

Drawbacks:

- Higher Risk: Losses are possible if the property underperforms.

- Longer Lock-Up Periods: Equity investments often require multi-year commitments.

- Market Sensitivity: Returns are affected by economic conditions, interest rates, and local demand.

When to Choose Debt vs. Equity

The choice depends on investment goals, risk tolerance, and time horizon:

- Income-Focused Investors: Debt funds are ideal for those seeking predictable, steady income with lower risk.

- Growth-Oriented Investors: Equity funds suit those willing to accept higher risk for the potential of capital appreciation and higher overall returns.

- Balanced Portfolios: Many investors allocate capital to both debt and equity funds to achieve income stability and growth potential.

Real-World Considerations

Leverage: Both debt and equity funds may use leverage, but debt funds are often more conservative, while equity funds may employ higher leverage to amplify returns.

Fund Structure: Debt funds often take the form of private lending vehicles, while equity funds may be structured as private partnerships, REITs, or mutual funds.

Market Conditions: Interest rate environments affect debt fund yields and property valuations, influencing equity fund returns.

Liquidity: Debt funds generally have shorter investment horizons, while equity funds may require 5–10 year commitments.

Combining Debt and Equity in a Portfolio

Integrating both debt and equity funds allows investors to balance risk and return. For example:

- 50% Debt: Provides predictable income and stability

- 50% Equity: Offers potential for capital appreciation and portfolio growth

This combination ensures steady cash flow while participating in long-term property appreciation, providing a balanced approach to real estate investing.

Conclusion

Debt and equity real estate funds represent two fundamentally different ways to invest in real estate:

- Debt funds offer stability, predictable income, and lower risk, making them suitable for conservative investors.

- Equity funds provide potential for higher returns through rental income and property appreciation but require a higher risk tolerance and longer investment horizon.

Understanding the differences between these strategies is critical for novice investors seeking to diversify their portfolios and align real estate investments with their financial goals. By strategically combining debt and equity funds, investors can achieve a well-rounded real estate allocation that balances stability, income, and growth potential.

{kind=link}