This Content Is Only For Subscribers

Why Leverage Matters

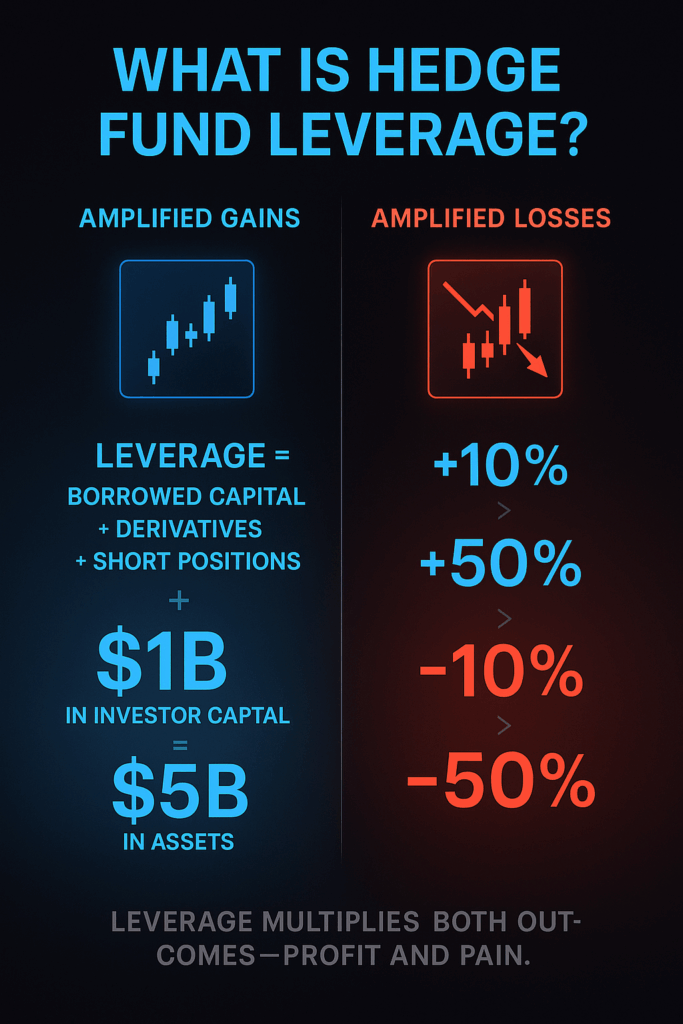

When people hear “hedge fund,” the word “hedge” suggests safety. But in reality, hedge funds are known for taking risks—and one of the biggest tools they use is leverage.

Leverage means borrowing money or using financial instruments to amplify potential returns. Used wisely, it can boost profits. Used recklessly, it can magnify losses and even sink a fund. For novice investors, understanding how leverage works—and how it’s managed—is key to understanding hedge fund risk.

What Is Leverage in Practice?

Leverage can take many forms:

- Borrowed Capital: Taking loans from banks or brokers to increase buying power.

- Derivatives: Using options, futures, and swaps to control large positions with limited upfront capital.

- Short Selling: Borrowing securities to sell them now, aiming to buy them back later at a lower price.

A hedge fund with $1 billion in investor money could use leverage to control $5 billion or more in assets. If investments rise 10%, the leveraged fund could return 50%. But if markets move the other way, losses are equally magnified.

Why Hedge Funds Use Leverage

Hedge funds pursue leverage for several reasons:

- Amplify Returns: A way to boost otherwise modest gains.

- Strategy Requirements: Some approaches, like fixed-income arbitrage, rely on large but low-margin positions that need leverage to be profitable.

- Diversification: Funds may borrow to spread across more opportunities without diluting their capital.

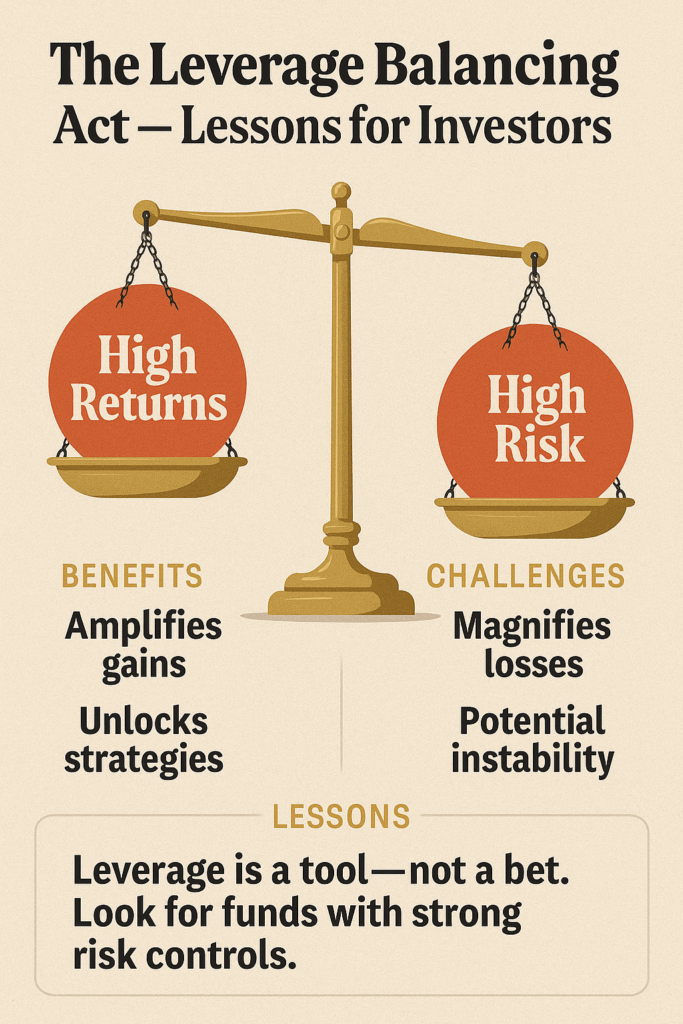

Leverage itself isn’t necessarily reckless—it depends on how it’s used.

Risks of Leverage

The danger is that leverage can make small miscalculations catastrophic. Consider:

- Liquidity Risk: If markets move suddenly, a fund may not be able to unwind leveraged positions fast enough.

- Margin Calls: Lenders can demand more collateral, forcing funds to sell assets at the worst possible time.

- Counterparty Risk: Banks or brokers providing leverage may cut credit in a crisis, leaving the fund stranded.

The infamous collapse of Long-Term Capital Management (LTCM) in 1998 illustrates this risk. Using extreme leverage, LTCM bet heavily on bond spreads converging. When Russia defaulted on its debt, those spreads widened instead. Losses spiraled, forcing a Federal Reserve-organized bailout to prevent broader financial contagion.

How Funds Manage Risk

Good hedge funds balance leverage with strong risk management systems. These can include:

- Position Limits: Caps on the size of individual bets relative to total capital.

- Value at Risk (VaR) Models: Statistical tools estimating potential losses in a given time frame.

- Stress Testing: Running simulations to see how the portfolio might react to extreme events, like a sudden interest rate spike.

- Liquidity Buffers: Holding cash or highly liquid assets to meet obligations quickly.

While no system is foolproof, these guardrails help funds avoid catastrophic losses.

The Role of Risk Officers

Many modern hedge funds employ Chief Risk Officers (CROs) who operate independently from portfolio managers. Their job is to challenge assumptions, enforce limits, and ensure the fund doesn’t overextend.

For investors, it’s worth asking: Does this fund have independent risk oversight, or is risk managed only by the same people making trades? Funds with strong risk culture often prove more resilient in downturns.

Leverage in Different Strategies

Not all hedge funds use leverage in the same way:

- Global Macro Funds: May use derivatives for large, directional bets on currencies, interest rates, or commodities.

- Equity Long/Short Funds: Often use moderate leverage to expand both long and short positions.

- Relative Value Arbitrage Funds: Typically rely heavily on leverage, since profit margins per trade are small.

As an investor, understanding the strategy helps you anticipate how much leverage is likely in play.

Regulatory Oversight

Unlike banks, hedge funds aren’t subject to strict leverage caps. However, regulators monitor them indirectly through disclosure rules and stress-testing of large financial institutions.

Post-2008, the Dodd-Frank Act increased reporting requirements. Hedge funds above a certain size must file detailed data (Form PF) about leverage and risk exposures. Still, transparency remains limited compared to mutual funds.

This means investors themselves need to do more homework—reading offering documents carefully and asking managers direct questions about leverage and risk policies.

Investor Considerations

If you’re evaluating a hedge fund, here are practical steps:

- Ask about leverage levels. Is it modest (1–2 times capital) or extreme (10+ times)?

- Understand the strategy. Some strategies require leverage; others don’t.

- Look at drawdown history. Past losses can reveal how the fund manages stress.

- Evaluate transparency. Does the manager provide clear reporting on risk?

Even sophisticated investors like pension funds sometimes underestimate leverage risks—so novice investors should approach with extra caution.

Leverage Isn’t Always the Villain

It’s easy to paint leverage as dangerous, but it’s also what makes many hedge fund strategies viable. Without leverage, arbitrage funds, for instance, might not exist at all. The key is balance. A disciplined manager uses leverage as a tool, not a gamble.

Final Takeaway

Leverage is the double-edged sword of hedge funds: it can deliver spectacular gains or devastating losses. What separates resilient funds from risky ones isn’t the presence of leverage—it’s how carefully it’s managed.

For novice investors, the lesson is clear: before investing, understand how much leverage a fund uses, how it controls risk, and whether it has a culture of discipline. Those factors often matter more than the investment strategy itself.

{kind=link}