This Content Is Only For Subscribers

Not every company private equity firms invest in is thriving. Some are struggling—maybe they’re drowning in debt, facing declining sales, or even headed toward bankruptcy. This is where a unique strategy within private equity comes into play: distressed investing.

Distressed private equity focuses on companies in financial trouble, buying their debt or equity at steep discounts with the goal of turning them around. It’s a high-risk, high-reward strategy that requires sharp analysis, steady nerves, and a willingness to tackle complex problems.

What Is Distressed Investing?

At its core, distressed investing means putting capital into troubled companies. These businesses may be unable to pay their debts, losing market share, or suffering from poor management. Private equity firms step in by:

- Buying Distressed Debt – Investors purchase bonds or loans of struggling companies at a discount. If the company recovers, those securities can soar in value. If the firm takes control through debt restructuring, it can convert debt into equity.

- Injecting Fresh Capital – In other cases, PE firms provide new funding directly to keep a company afloat, often in exchange for significant ownership stakes.

- Taking Control in Bankruptcy – Sometimes, distressed investors acquire companies through bankruptcy proceedings, helping restructure operations and debt obligations.

Why Distressed Investing Exists

Businesses don’t always fail because their products are bad. Sometimes external shocks—like a recession, rising interest rates, or supply chain disruptions—strain otherwise solid companies. Distressed investors step in when traditional financing dries up, keeping these companies alive and giving them a chance to recover.

In a way, distressed private equity plays an important economic role: it recycles struggling assets and gives companies a second chance. Of course, investors are also in it for the potential rewards.

Potential Rewards

The main appeal of distressed investing is buying low. If a company’s debt trades at 40 cents on the dollar, and the business stabilizes, the upside can be enormous. By acquiring equity stakes cheaply, PE firms can see big returns if a turnaround succeeds.

Some of the world’s most successful private equity deals have come from distressed situations. During the 2008 financial crisis, for example, firms that bought assets in beaten-down sectors like real estate and financial services reaped huge profits as the economy recovered.

Risks of Distressed Investing

With high potential reward comes high risk. Distressed companies are distressed for a reason, and not all can be saved. Common risks include:

- Structural Problems: A company may be in a declining industry with no realistic growth prospects.

- Excessive Debt: If the debt burden is too great, even strong operations may not keep the company afloat.

- Management Challenges: Poor leadership or entrenched corporate cultures can make change difficult.

- Economic Uncertainty: Recessions or market shocks can sink already fragile businesses.

Sometimes, even the best turnaround efforts fail, leaving investors with significant losses.

A Real-World Example

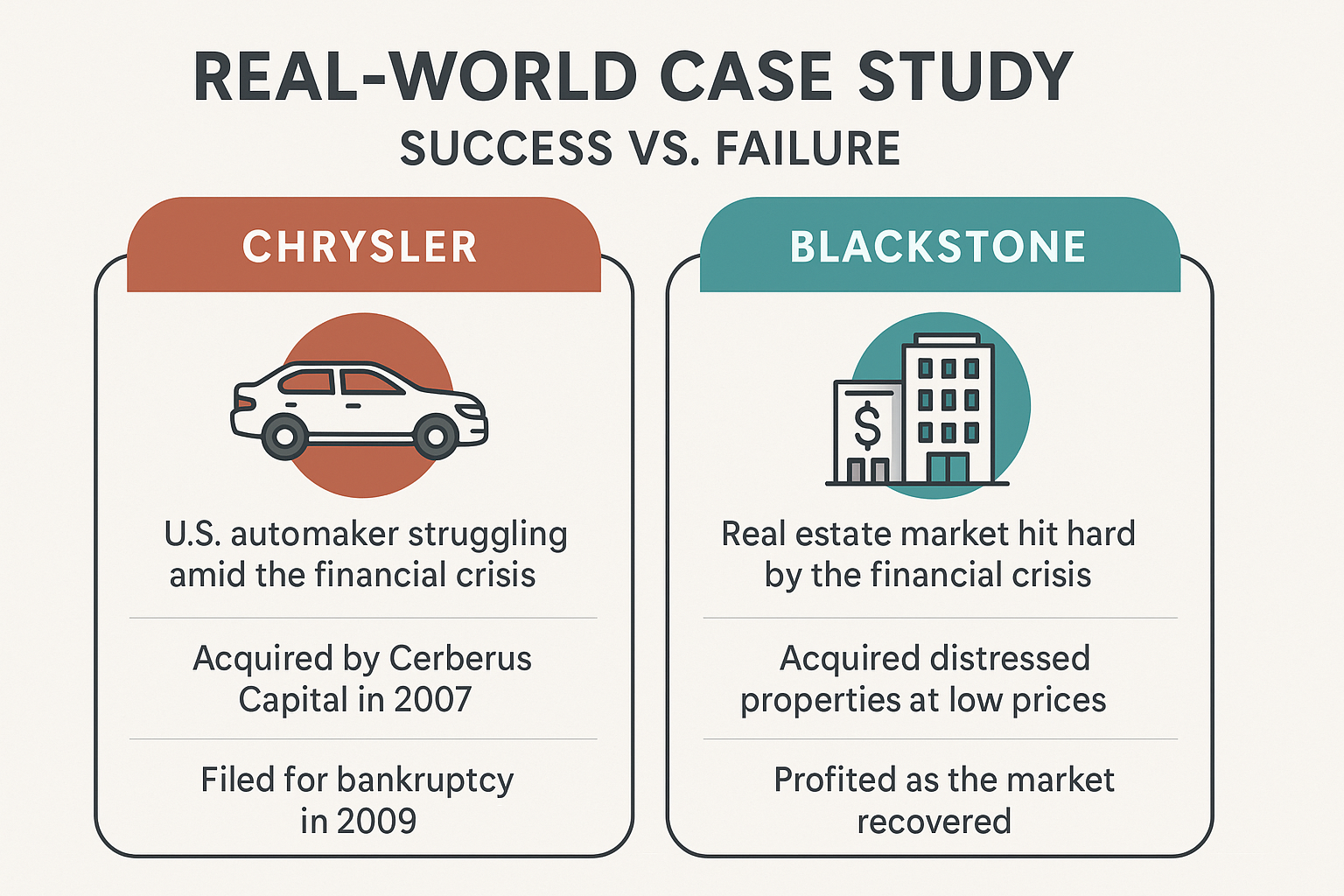

One of the most famous distressed deals was Cerberus Capital Management’s purchase of Chrysler in 2007. The U.S. automaker was already struggling, and when the financial crisis hit, things went from bad to worse. Cerberus injected capital but ultimately couldn’t turn the company around. Chrysler filed for bankruptcy in 2009 before eventually merging with Fiat.

Contrast that with distressed investments in real estate during the same period. Firms like Blackstone scooped up properties at rock-bottom prices, then profited handsomely when the real estate market rebounded. The difference highlights just how varied outcomes can be in distressed investing.

How PE Firms Create Value in Distressed Situations

Turning around a struggling company takes more than money. Distressed investors often bring in new leadership, cut unprofitable divisions, renegotiate with lenders, and streamline operations. The goal is to stabilize cash flow, rebuild credibility with stakeholders, and set the stage for long-term recovery.

They may also restructure the company’s capital stack—reducing interest payments, extending debt maturities, or converting debt into equity. By giving the company breathing room, they increase the chances of a successful turnaround.

Lessons for Novice Investors

Even if you never invest directly in private equity, distressed investing offers lessons:

- Look for Opportunity in Crisis: Just as PE firms see potential in beaten-down companies, individual investors may find value in sectors temporarily out of favor.

- Understand the Risks: Bargains aren’t always what they seem. A “cheap” stock or bond may be cheap for very good reasons.

- Patience Matters: Turnarounds take time, and not all succeed. Having realistic expectations is crucial.

It’s also worth noting that you may already have indirect exposure to distressed investing. Pension funds and institutional investors often allocate part of their portfolios to these strategies, meaning everyday savers benefit (or take on risk) without realizing it.

The Human Side

Distressed investing is not without controversy. Restructuring often means layoffs, cost-cutting, and tough decisions that affect employees and communities. Critics argue that some firms prioritize profits over people, while defenders counter that saving part of a company is better than letting it fail entirely.

This tension highlights the complex role distressed investors play—not just as financial engineers, but as stewards of struggling businesses with real-world consequences.

Final Thoughts

Distressed private equity investing is one of the boldest strategies in finance. By stepping into high-pressure situations, investors have the chance to reap huge rewards—but also to lose everything if turnarounds fail.

For new investors, understanding this strategy sheds light on the broader private equity world. It shows how capital, expertise, and timing can make the difference between failure and recovery. And while most of us won’t be buying bankrupt companies anytime soon, the lessons—about risk, resilience, and opportunity in crisis—are valuable for anyone building a portfolio.

{kind=link}