This Content Is Only For Subscribers

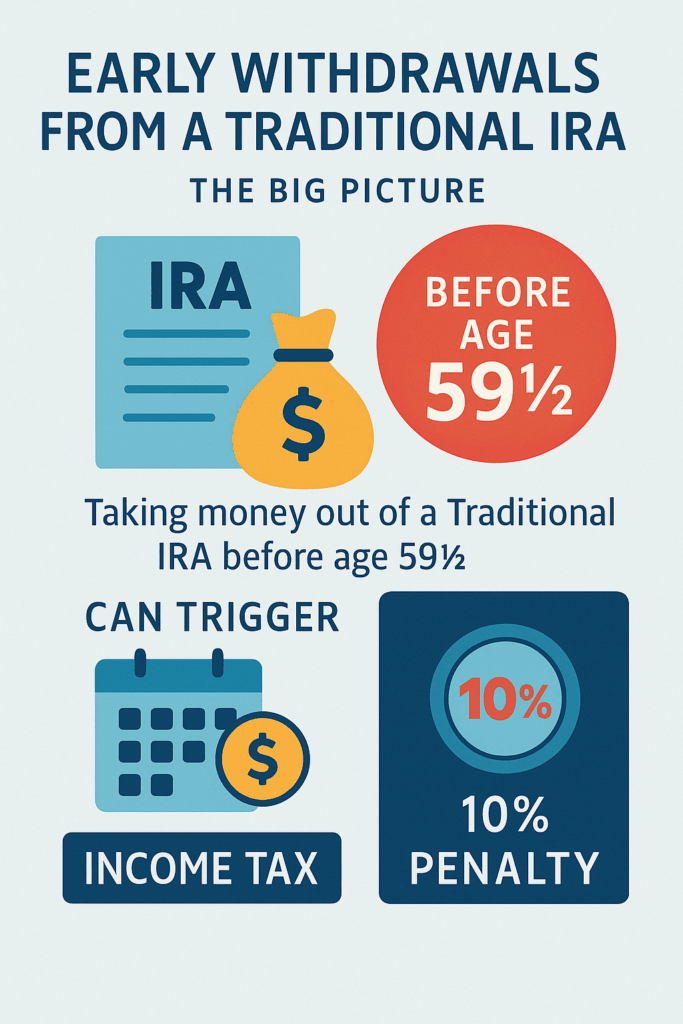

A Traditional IRA is a powerful tool for retirement savings, offering tax advantages and long-term growth potential. But one of the key rules to remember is that early withdrawals—taking money out before age 59½—can come with taxes and penalties. Understanding these rules can help you avoid unnecessary costs and make informed decisions if you need access to your funds before retirement.

What Counts as an Early Withdrawal?

An early withdrawal from a Traditional IRA occurs when you take money out before age 59½. While the IRS allows you to access your money at any time, doing so before this age usually comes with consequences:

- Income tax: Withdrawals are taxed as ordinary income.

- Early withdrawal penalty: A 10% penalty is applied to the amount withdrawn, on top of income taxes.

For example, if you withdraw $10,000 early and you are in the 22% federal tax bracket, your taxes and penalties could look like this:

- Federal income tax: $10,000 × 22% = $2,200

- 10% penalty: $10,000 × 10% = $1,000

- Total cost: $3,200

Exceptions to the 10% Penalty

The IRS recognizes that there are situations where early access to retirement funds may be necessary. In these cases, you can avoid the 10% penalty, though ordinary income tax still applies. Key exceptions include:

1. First-Time Home Purchase

- Up to $10,000 can be withdrawn to buy, build, or rebuild a first home.

- This is a lifetime limit, not an annual limit.

- The funds can be used for the taxpayer, a spouse, or a dependent.

2. Qualified Education Expenses

- Funds can be used for tuition, fees, books, and supplies for yourself, your spouse, or children or grandchildren.

- Room and board may also qualify if the student is at least half-time.

3. Medical Expenses

- If unreimbursed medical expenses exceed 7.5% of your adjusted gross income (AGI), you may withdraw funds penalty-free to cover these costs.

4. Health Insurance Premiums

- If you are unemployed and paying for health insurance premiums, you may withdraw funds penalty-free.

5. Disability

- If you become totally and permanently disabled, early withdrawals are exempt from the 10% penalty.

6. Substantially Equal Periodic Payments (SEPP)

- The IRS allows penalty-free withdrawals through a structured program of equal payments over your life expectancy.

- This is often called the 72(t) rule and requires careful planning to avoid penalties.

Tax Considerations on Early Withdrawals

Even if you qualify for a penalty exception, early withdrawals are generally subject to ordinary income tax. This means the withdrawn amount increases your taxable income for the year.

- For example, withdrawing $10,000 for qualified education expenses still adds $10,000 to your taxable income.

- Planning early withdrawals carefully can help minimize your tax liability.

Strategies to Avoid Early Withdrawal Penalties

Wait Until 59½ When Possible

- This is the simplest way to avoid penalties and taxes on withdrawals.

Use Roth IRA Contributions

- Unlike Traditional IRAs, Roth IRA contributions (not earnings) can be withdrawn at any time tax- and penalty-free.

- This can provide a flexible emergency fund.

Leverage SEPP Plans

- If you need early income from a Traditional IRA, SEPP plans allow structured withdrawals without penalties.

- Must follow IRS rules carefully; changing the plan can trigger penalties retroactively.

Consider Other Accounts First

- Taxable brokerage accounts or emergency savings can be used before dipping into retirement accounts.

- Preserves the tax-advantaged growth of your IRA.

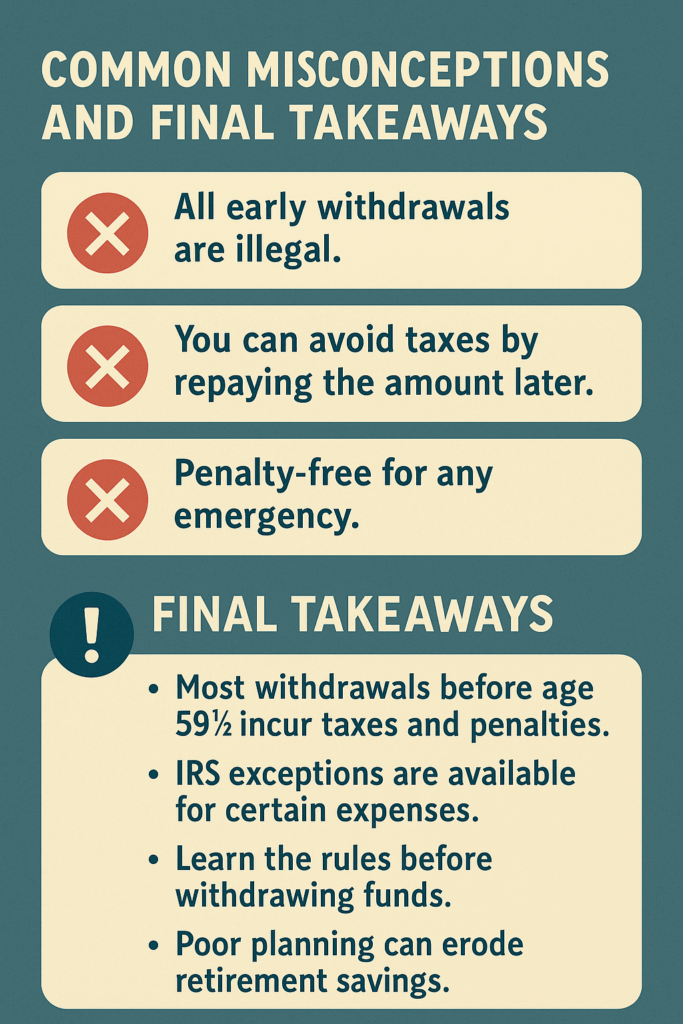

Common Misconceptions About Early Withdrawals

“All early withdrawals are illegal.”

- ❌ False. They are legal but usually subject to taxes and penalties unless exceptions apply.

“You can avoid taxes if you just deposit the money back later.”

- ❌ False. Traditional IRAs allow rollovers but only if done within 60 days and not exceeding one rollover per year.

- Failing to meet these rules triggers taxes and potential penalties.

“You can withdraw penalty-free for any emergency.”

- ❌ False. Only IRS-defined exceptions qualify for penalty-free withdrawals.

Planning for Early Withdrawals

- Know the rules before withdrawing: Confirm whether your situation qualifies for a penalty exception.

- Calculate the tax impact: Consider your federal and state tax rates.

- Document carefully: Keep receipts and records in case the IRS requests proof of a qualified exception.

- Consult a financial advisor: Complex situations, like SEPP plans, are easier to manage with professional guidance.

Real-Life Example

Sarah, age 45, needs $8,000 for tuition for her child. Her Traditional IRA balance is $50,000.

- Since qualified education expenses are an exception, she avoids the 10% penalty:

- 10% penalty on $8,000 = $0

- She still owes federal income tax:

- If her tax rate is 22%, she pays $1,760 in income taxes.

By understanding the rules and planning ahead, Sarah accesses the funds she needs without triggering extra penalties.

Why Understanding Early Withdrawals Matters

Early withdrawal rules are about protecting your retirement savings while allowing some flexibility for genuine needs.

- Penalties are steep: 10% plus ordinary income tax.

- IRS exceptions exist but are limited.

- Poor planning can erode retirement security.

For novice investors, being aware of these rules now can help prevent costly mistakes and ensure your IRA grows as intended for retirement.

Final Thoughts

Traditional IRAs provide a tax-advantaged path to retirement, but early withdrawals can undermine those benefits. Knowing what counts as an early withdrawal, which exceptions exist, and how taxes and penalties apply empowers you to make informed decisions.

By planning ahead, using exceptions wisely, and exploring alternatives like Roth IRAs or SEPP plans, you can access funds when necessary without jeopardizing your long-term retirement goals.

{kind=link}