This Content Is Only For Subscribers

When people think of private equity, one strategy often comes to mind: the leveraged buyout, or LBO. This is the iconic play that made headlines in the 1980s, produced blockbuster deals, and helped define the entire private equity industry. Yet while LBOs sound intimidating, the basic idea is surprisingly straightforward. At its core, a leveraged buyout is about buying a company using a mix of borrowed money and investor capital, then improving the business to sell it later for a profit.

For novice investors, understanding how leveraged buyouts work is a great way to grasp the mechanics of private equity as a whole. Let’s break it down step by step.

What Is a Leveraged Buyout?

In a leveraged buyout, a private equity (PE) firm acquires a company by combining equity (money from its fund) with debt (borrowed capital, often from banks or bond markets). The “leveraged” part refers to the fact that most of the purchase price is funded with debt rather than equity.

Think of it like buying a house: you might put down 20% in cash and borrow 80% with a mortgage. If the house increases in value, your return is magnified because you only invested a fraction of the price upfront. LBOs work the same way, just with businesses instead of real estate.

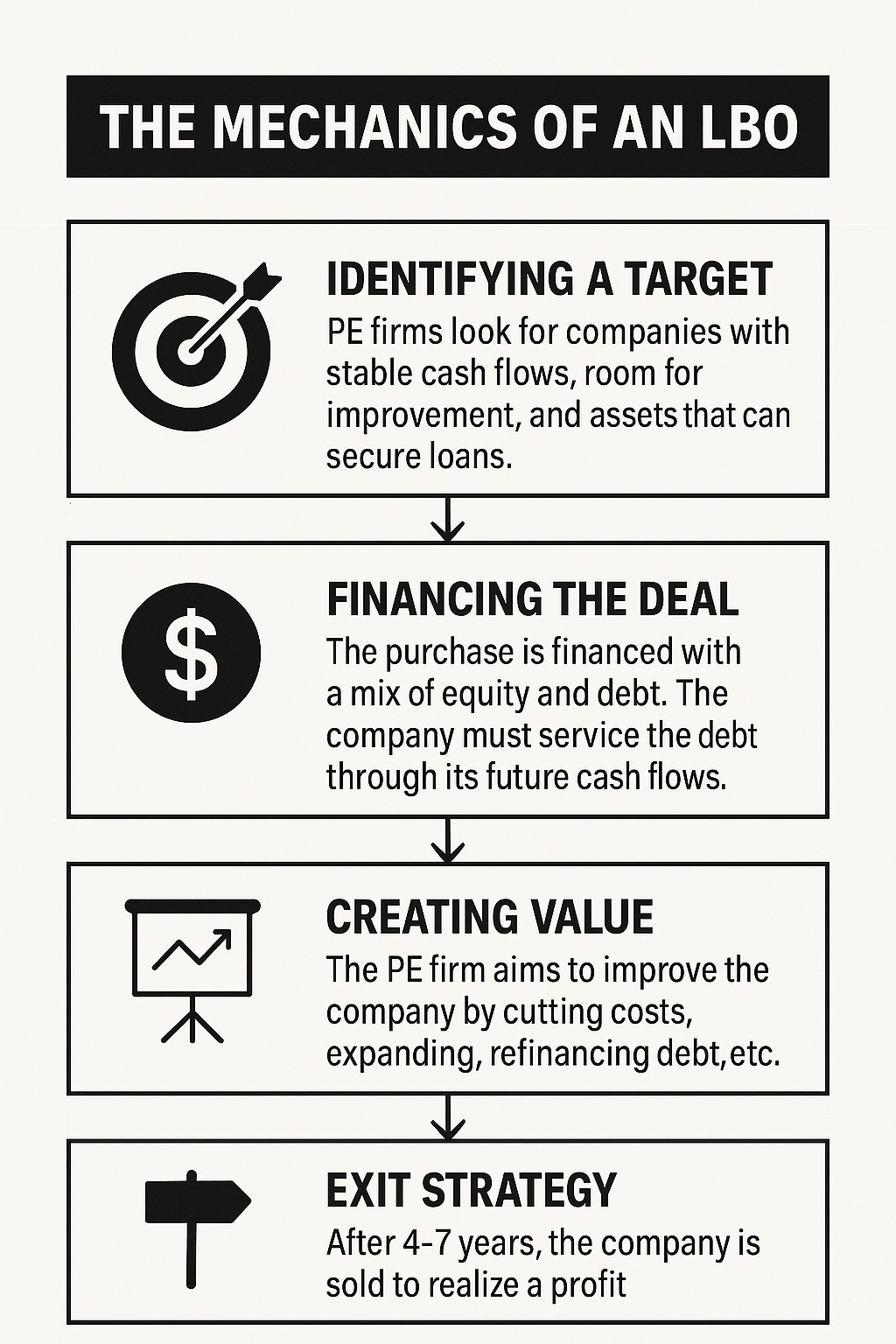

The Mechanics of an LBO

- Identifying a Target

PE firms look for companies with stable cash flows, room for improvement, and assets that can be used to secure loans. Strong, predictable earnings are essential because the company itself is expected to help pay off the debt. - Financing the Deal

The purchase is financed with a mix of equity and debt. In many cases, debt makes up 60–80% of the total price. The company being acquired is responsible for servicing that debt through its future cash flows. - Creating Value

Once the PE firm owns the company, it works to increase its value. This might include:- Cutting costs and streamlining operations.

- Expanding into new markets.

- Refinancing debt at better terms.

- Improving management or governance.

- Exit Strategy

After several years (usually 4–7), the PE firm looks to sell the company at a higher value. Common exits include selling to another company, selling to another PE firm, or taking the company public again through an IPO.

Why Use Leverage?

Leverage amplifies returns. If an investor buys a business entirely with cash, their profits are tied directly to the company’s performance. But by using borrowed money, they can generate higher returns on the equity they actually put in.

Here’s a simple example:

- A PE firm buys a company for $100 million, using $30 million in equity and $70 million in debt.

- Over time, the company improves and is sold for $150 million.

- After paying off the $70 million debt, $80 million is left for equity holders.

- The initial $30 million investment grew to $80 million—a return of nearly 167%.

Without leverage, the return would have been just 50%.

A Famous Example: Hilton Hotels

One of the most successful LBOs was Blackstone’s 2007 acquisition of Hilton Hotels for $26 billion. At the time, the financial crisis soon hit, and many critics doubted the deal would work. But over the next few years, Hilton improved operations, expanded globally, and recovered strongly. When Hilton went public again in 2013, Blackstone made more than $14 billion in profit—one of the most lucrative private equity deals in history.

Risks of Leveraged Buyouts

While leverage magnifies gains, it also magnifies losses. If a company underperforms, the heavy debt burden can become overwhelming. In the worst cases, LBOs lead to bankruptcies.

Risks include:

- Debt pressure: Companies must use cash flow to pay interest, leaving less room for reinvestment.

- Economic downturns: Recessions can shrink cash flows, making debt harder to manage.

- Overpaying: If the PE firm pays too high a purchase price, even improvements may not deliver enough return.

The 1980s saw several high-profile failures, which gave LBOs a reputation for being ruthless. Critics argued that firms loaded companies with debt, cut jobs, and prioritized short-term profits. While the industry has matured, the balance between risk and reward is still delicate.

Modern LBOs

Today’s leveraged buyouts are often more sophisticated than their 1980s predecessors. PE firms focus on creating long-term value, not just financial engineering. Many bring in operational experts, industry specialists, and new leadership teams to strengthen portfolio companies.

Sectors like healthcare, software, and consumer goods are popular targets because of their steady cash flows and growth potential. At the same time, firms are more cautious about leverage levels, especially after the lessons of the global financial crisis.

What Novice Investors Can Learn

Even if you never invest directly in a private equity fund, leveraged buyouts offer lessons for personal investing:

- Prudent use of debt: Leverage can be powerful, but only when backed by reliable cash flow.

- Value creation matters: PE firms don’t just buy and hold—they actively improve companies.

- Timing is critical: Market cycles, interest rates, and industry trends all influence outcomes.

You may also be indirectly invested in LBOs without realizing it. Pension funds, endowments, and insurance companies—institutions that manage everyday people’s money—commit billions to PE funds that specialize in buyouts.

Final Thoughts

Leveraged buyouts are the cornerstone of private equity, combining strategic deal-making with financial leverage to unlock value. They can deliver extraordinary returns, but they also carry significant risks if debt becomes unmanageable or markets turn against the business.

For new investors, LBOs are worth understanding because they illustrate how private equity firms think: identify opportunities, use capital creatively, and focus relentlessly on value creation. Whether you admire or criticize the approach, leveraged buyouts remain one of the most powerful tools in the investment world.

{kind=link}