This Content Is Only For Subscribers

Private equity (PE) often makes headlines for splashy acquisitions, billion-dollar funds, or the massive fortunes earned by its top players. But behind the buzz, private equity is really a set of investment strategies with a common thread: taking stakes in private businesses to create value and earn strong returns.

For novice investors, the world of private equity can feel both glamorous and intimidating. The jargon is dense, the deals are complex, and the investor base is usually reserved for institutions or ultra-wealthy families. Yet the core ideas are not as mysterious as they might seem. Once you understand the main strategies private equity firms use, the entire landscape starts to come into focus.

This article unpacks the most common private equity strategies—buyouts, growth equity, distressed investing, and more—so you can see how they differ, where they overlap, and why investors pursue them.

What Is Private Equity, Exactly?

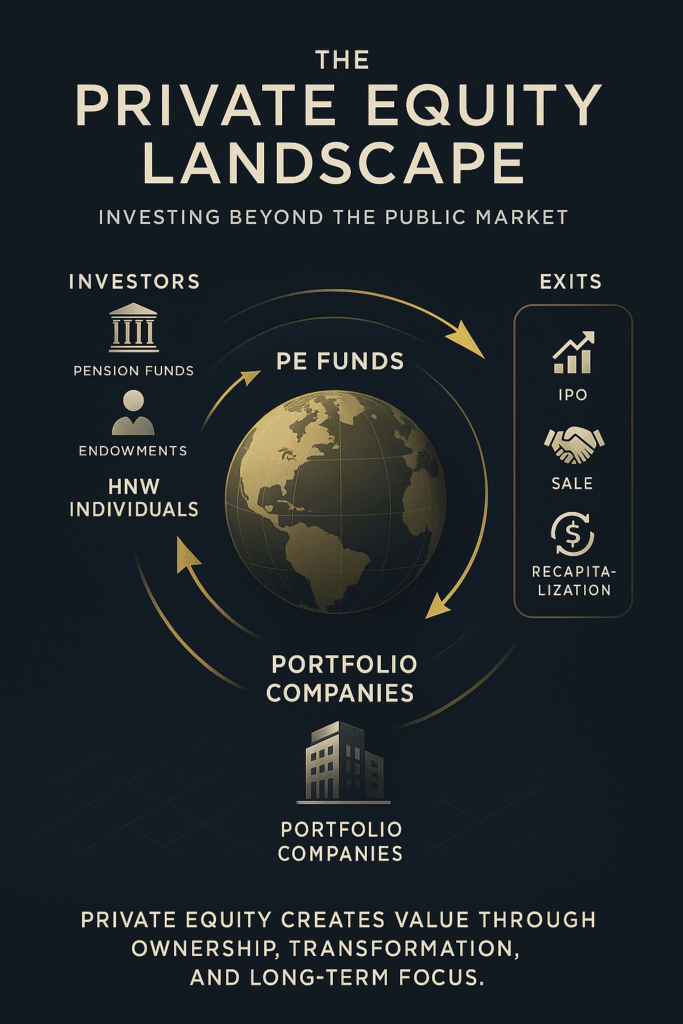

At its core, private equity is about investing in companies that aren’t listed on public stock exchanges. Firms raise capital from investors—often pension funds, endowments, insurance companies, and wealthy individuals—and pool that money into funds. Those funds are then used to acquire stakes in businesses with the goal of improving their value and eventually selling at a profit.

Unlike mutual funds or ETFs, private equity investments are illiquid. That means investors commit their capital for years at a time—usually 7 to 10 years—while the firm works to generate returns. The illiquidity comes with a potential payoff: private equity has historically outperformed many traditional asset classes, although the risks are higher too.

Within private equity, there isn’t just one playbook. Firms employ a variety of strategies depending on the type of company they’re targeting, the maturity of the business, and the risks and rewards they’re seeking.

Buyouts: The Classic Private Equity Strategy

When most people think of private equity, they think of buyouts—sometimes called leveraged buyouts (LBOs). This is the strategy that made names like KKR and Blackstone famous in the 1980s and 1990s.

How Buyouts Work

In a buyout, a private equity firm acquires a controlling stake in a company, often taking it private if it was publicly traded. The acquisition is typically financed using a mix of the fund’s equity capital and borrowed money (leverage). This is why the term “leveraged buyout” is often used.

Once the deal closes, the PE firm works to increase the company’s value over several years. Common levers include:

- Operational improvements: streamlining processes, cutting costs, or improving supply chains.

- Strategic shifts: focusing on more profitable business lines or expanding into new markets.

- Financial engineering: optimizing debt structures, refinancing loans, or managing working capital more effectively.

Case Study: Hilton Hotels

One of the most famous buyouts was Blackstone’s 2007 acquisition of Hilton Hotels for about $26 billion. At the time, critics thought Blackstone overpaid, especially with the global financial crisis looming. Yet through operational improvements and strategic growth, Hilton’s value soared. By the time Hilton went public again in 2013, Blackstone’s investment was hailed as a massive success, generating billions in profit.

Why Buyouts Appeal to Investors

Buyouts are attractive because they allow firms to exert significant control. With a controlling stake, PE firms can make the tough decisions needed to unlock value. The use of leverage can also magnify returns if the investment goes well.

Risks of Buyouts

The flip side of leverage is that it magnifies losses too. If the acquired company struggles under its new debt load, the PE firm could face steep losses or even bankruptcy. Buyouts also tend to be cyclical, performing better in strong economies when debt is cheap and companies are growing.

Growth Equity: Fueling Expansion

Growth equity sits somewhere between venture capital and buyouts. It’s aimed at companies that are past the risky startup stage but not yet mature enough for a full buyout.

How Growth Equity Works

In a growth equity deal, the PE firm typically takes a minority stake in a company rather than buying it outright. The capital provided is used to accelerate growth—hiring more staff, expanding into new geographies, developing new products, or making acquisitions.

For example, a profitable software company with steady revenue might need $50 million to scale into international markets. A growth equity investor provides that funding in exchange for a stake in the business, with the expectation that the company’s value will multiply in the coming years.

Case Study: Facebook’s Early Backers

In 2009, when Facebook was already a dominant social network but not yet public, Digital Sky Technologies (DST) invested $200 million for a minority stake. That growth equity deal helped fuel expansion and gave DST a massive return when Facebook went public in 2012.

Why Growth Equity Matters

Growth equity is often seen as a “sweet spot” strategy. The companies targeted are less risky than early-stage startups but still have significant upside. Because the PE firm isn’t taking control, the existing management team typically stays in place, which can be appealing to founders.

Risks of Growth Equity

The risk is that growth doesn’t materialize as expected. Maybe international expansion proves too costly, or competition eats into margins. Because the firm doesn’t control the company, it has less ability to course-correct if things go wrong.

Distressed Private Equity: Turning Around Trouble

Distressed investing is a very different flavor of private equity. Instead of targeting healthy companies, distressed investors seek out businesses that are struggling—sometimes even in bankruptcy.

How Distressed Investing Works

Distressed investors often buy debt rather than equity. For instance, if a company is having trouble repaying its loans, its debt might trade at a steep discount. A PE firm can buy that debt, potentially gaining control of the company through restructuring.

Other times, the firm injects new capital into a struggling company in exchange for ownership. The idea is to stabilize the business, restructure operations, and eventually sell at a profit.

Case Study: Chrysler’s Turnaround

In 2007, Cerberus Capital Management acquired an 80% stake in Chrysler, just before the auto industry was hit hard by the financial crisis. While Cerberus’s investment was rocky and controversial, it illustrates how distressed investors step into industries or companies in crisis, often betting on a turnaround where others see only collapse.

Why Distressed Investing Appeals

Distressed deals can deliver outsized returns if the turnaround succeeds. Buying assets on the cheap creates the potential for big gains. Distressed investing also plays a critical role in the economy by keeping companies alive that might otherwise fail.

Risks of Distressed Deals

The obvious risk is that the turnaround doesn’t work. Struggling companies often face deep structural problems—declining industries, outdated products, or toxic cultures. Even with new capital and management, not every business can be saved.

Secondary Investments: A Market for PE Stakes

Private equity is known for its long lock-up periods, but what if an investor wants out early? That’s where secondary investing comes in.

How Secondaries Work

Secondary funds buy existing stakes in private equity funds from investors who want liquidity before the fund’s life is over. For example, a pension fund that committed $100 million to a buyout fund might decide it needs cash five years in. A secondary buyer purchases that stake, usually at a discount, and assumes the rights to future returns.

Case Study: CalPERS and Secondary Sales

Large institutional investors like CalPERS, the California Public Employees’ Retirement System, have occasionally sold parts of their private equity portfolios on the secondary market. These sales allow them to rebalance exposure and free up capital, while buyers gain access to funds they otherwise couldn’t join.

Why Secondaries Are Attractive

Secondary deals allow investors to enter funds at a later stage, often when the portfolio companies are more mature and risks are clearer. Discounts on purchases can also enhance returns.

Risks of Secondaries

Valuation can be tricky. If the underlying portfolio underperforms, the discount may not be enough to protect returns. The market is also competitive, with many firms chasing the same deals.

Fund-of-Funds: Diversification Made Simple

Another strategy is investing through a fund-of-funds (FoF). Instead of directly buying companies, a FoF invests in a mix of private equity funds.

Why Investors Use Fund-of-Funds

For smaller institutions or wealthy families without large teams, FoFs provide instant diversification across managers, strategies, and geographies. Rather than betting on one buyout fund or one growth equity manager, you get exposure to many.

The Trade-Offs

The downside is cost. Fund-of-funds charge their own fees on top of the fees already charged by the underlying funds. This “double layer” can eat into returns. Still, for investors seeking diversification and professional manager selection, FoFs can be a valuable tool.

Other Niche Strategies

While buyouts, growth equity, distressed, secondaries, and fund-of-funds are the big categories, there are other specialized strategies worth noting:

- Venture Capital: Though technically distinct, some private equity firms also run venture capital arms focused on early-stage startups.

- Real Assets: Some PE funds invest in infrastructure, energy projects, or natural resources.

- Sector-Specific Funds: Certain firms specialize in areas like healthcare, technology, or consumer goods.

Trends in Private Equity Strategies

The private equity industry isn’t static. Strategies evolve with markets, regulations, and investor demand. A few key trends stand out today:

- ESG Integration: Many investors are pushing PE firms to consider environmental, social, and governance (ESG) factors in their investments. This can mean everything from energy efficiency to board diversity.

- Tech Focus: Technology and software companies are increasingly popular targets, given their scalability and recurring revenue models.

- Co-Investing with Family Offices: Wealthy families and their offices are increasingly bypassing traditional funds to invest directly alongside PE firms, giving them more control and lower fees.

The Common Thread: Value Creation

Despite the different flavors, all private equity strategies share one goal: to create value and deliver strong returns to investors. Whether through operational improvements, growth capital, turnaround strategies, or smart diversification, private equity firms aim to transform companies in ways that public market investors often can’t.

What Novice Investors Should Know

If you’re a new investor, you might not have direct access to private equity—most funds are open only to institutional or accredited investors. But understanding PE strategies is still valuable.

- Perspective on markets: Private equity shapes the business landscape. Companies you buy stock in may have once been owned by PE firms.

- Indirect exposure: You might already be invested in private equity through your pension, university endowment, or insurance company.

- Lessons to borrow: PE teaches the power of long-term focus, rigorous due diligence, and aligning incentives—principles that can apply to personal portfolios too.

Final Thoughts

Private equity is a vast and varied industry. From classic buyouts to growth equity, distressed turnarounds, secondary markets, and fund-of-funds, each strategy offers its own mix of risks and rewards.

For novice investors, the details can seem overwhelming, but the big picture is straightforward: private equity is about using capital, expertise, and time to transform businesses. By understanding the main strategies, you gain insight not only into how PE works but also into how value is created in the broader economy.

{kind=link}