This Content Is Free After You Enter Your Email

Why Fees Matter in Hedge Funds

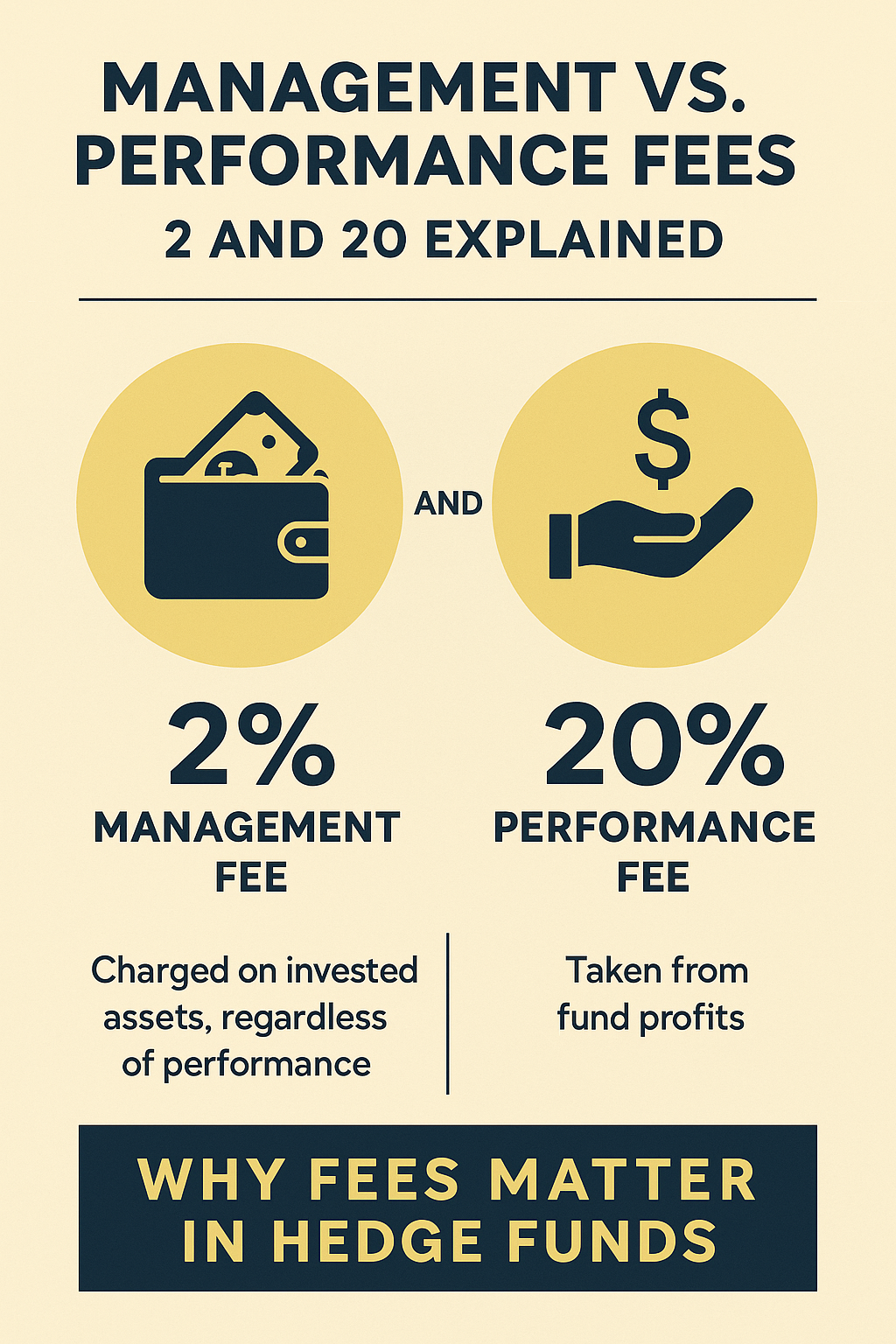

When you invest in a hedge fund, fees aren’t just fine print—they’re central to how the industry works. Unlike mutual funds or ETFs, which charge less than 1% annually, hedge funds are famous for their “two-part” fee model: management fees and performance fees.

The shorthand for this is “2 and 20,” and while it’s not universal, it has shaped the hedge fund industry for decades.

The Basics: What “2 and 20” Means

- 2% Management Fee: Charged on the assets you invest, whether the fund makes or loses money. Think of it as the subscription cost for being in the fund.

- 20% Performance Fee: Taken from profits. If you invest $1 million and the fund gains 10% ($100,000), the manager takes $20,000.

This setup ensures the manager has steady income while also being rewarded when investors earn returns.

A Bit of History

The performance-fee idea dates back to Alfred Winslow Jones, who launched what’s often called the first hedge fund in 1949. He charged investors based on profits, arguing it aligned his incentives with theirs.

By the 1980s and 1990s, as stars like George Soros and Julian Robertson delivered blockbuster results, “2 and 20” became an informal standard. Today, though, fees vary widely, often lower than the classic formula.

Why Management Fees Exist

Running a hedge fund is expensive. Managers must pay analysts, buy research, maintain technology, and meet regulatory obligations. The management fee provides predictable income to cover these costs—even during losing years.

Critics argue it feels unfair to pay when returns are poor. As a result, many funds now charge closer to 1.5% or less, especially when negotiating with big institutional investors like pension funds.

Why Performance Fees Exist

Performance fees are supposed to align manager and investor interests—when you win, they win.

But there are drawbacks:

- Risk-taking: Managers may chase short-term gains to boost fees.

- Asymmetry: Investors bear losses, while managers pocket fees from past gains.

To address this, many funds use:

- High-water marks: Performance fees are only earned on new profits, not on recovering old losses.

- Hurdle rates: A minimum return (say 5%) before fees kick in.

What This Means for Investors

If you’re considering hedge fund investing, here are key questions to ask:

- What exactly are the fees? Is it truly “2 and 20” or a different arrangement?

- Is there a high-water mark? This ensures you don’t pay fees twice on the same gains.

- Are there hurdle rates? These prevent fees on subpar returns.

- Can fees be negotiated? Large investors often negotiate lower fees.

Understanding these terms matters: a few percentage points in fees each year can make a massive difference over time.

The Changing Fee Landscape

After the 2008 financial crisis, many funds struggled to outperform the market, putting pressure on the fee model. Some trends:

- Average fees have dropped closer to 1.5 and 15 or even 1 and 10.

- Some funds charge performance-only fees, skipping management fees altogether.

- Large investors often get “founder shares” with discounted fees in exchange for early commitments.

Meanwhile, the rise of cheap index funds and ETFs has forced hedge funds to prove they’re worth the premium.

Comparisons to Other Investments

- Mutual Funds: Typically under 1%, with no performance fee.

- Private Equity: Similar “2 and 20” structure, but profits are tied to long-term deals.

- Index Funds/ETFs: Some charge as little as 0.03%.

Hedge funds justify higher fees with the promise of specialized strategies and the potential for uncorrelated, above-market returns.

Case Study: Investor Pushback

In 2014, CalPERS—the largest U.S. public pension—pulled out of hedge funds altogether, citing high fees and complexity. This spurred more scrutiny across the industry.

But niche funds with unique expertise (like distressed debt or quant trading) continue to attract investors willing to pay for access to specialized skills.

Psychology and Perception

Interestingly, fees aren’t just math—they influence perception. High fees sometimes signal exclusivity, making a fund appear more elite. Conversely, funds that cut fees too much risk looking less prestigious.

Key Takeaways

- Hedge fund fees matter far more than in traditional investments.

- “2 and 20” is the classic model, but many funds charge less today.

- Protections like high-water marks and hurdle rates are essential to understand.

- Investors should evaluate whether a fund’s potential strategy justifies the higher cost.

Final Word

For novice investors, hedge fund fees are a window into how the industry works. They shape incentives, affect risks, and ultimately determine how much of your return you keep.

While “2 and 20” may still symbolize the hedge fund world, real fees are often more nuanced. By asking the right questions and understanding how these structures work, you can better decide whether a fund’s costs are worth its potential rewards.

{kind=link}